- T1 is NOT an AI Play – It is a China Hustle

- IP Sale to “Independent Party” Evervolt was Supposed to Make T1 FEOC Compliant & Unlock Key US Tax Credits. It was an Illusion.

- Evervolt’s Owner Has a Web of Secret Connections to Chinese Trina Solar

- We Uncovered Direct Connections to Chinese State-Owned Enterprises & “Alleged” Chinese Criminals

- Thus T1 is Ineligible for US Tax Credits & No Profits

- Patent Databases Show IP Still Owned by Trina Not Evervolt & Trina is 99% of T1’s Revenue

- Former T1 Executives, US Commerce Dept Officials, and Tax Credit Lawyers all told us T1 Energy is FEOC’ed

- Drone Flights over G2 Show It is Behind Schedule; G2 is Not AI, but G2 is FEOC’ed, too

- Is it Accounting Fraud to Boost Income via Tax Credits You’ll Never Earn? We Believe Large Restatements Are Coming Soon

We are Short T1 Energy (TE), a failed battery SPAC who pivoted and bought a solar module manufacturing plant from a Chinese solar producer, Trina Solar. T1’s stock is not only fully pricing in continued US tax credits but investors have mistakenly begun confusing T1 as an AI infrastructure play. T1’s sales do NOT come from AI datacenter customers, instead, 99.9% of Q1 sales came from the Chinese solar company that originally spawned T1, Trina Solar. We will show you why T1 Energy is Not an AI solar play but is instead just another China Hustle.

Days before the end of FY2025, T1 scrambled to get in line with new US tax rules. T1’s access to Trina IP was the primary driver of it’s business but the IP being owned by Trina suddenly meant T1 was ineligible for essential tax credits. So T1 & Trina Solar announced that Trina’s extremely valuable IP (thousands of patents) had all been transferred to an unknown and ‘independent’ Singaporean company called Evervolt. T1 tried a classic Shanghai street hustle. The hustle where there are 3 plastic cups and 1 ball and the ball magically moves to the other cup. In this case the ball is the IP and T1 & Trina have claimed that the IP was all magically transferred to Evervolt. Evervolt is the key! Evervolt has allowed T1’s management to claim they continue to qualify for US solar tax credits and are FEOC compliant (FEOC = Foreign Entity of Concern – aka a Chinese company). T1’s business is 100% dependent on tax credits. With US tax credits T1’s a decent low margin business. BUT without tax credits, no AI datacenter demand will ever come, and T1’s business is wildly unprofitable. We found Evervolt is deeply connected to both Trina Solar and the Chinese government. The IP transfer was a mirage. T1 Energy is still a FEOC, and T1’s economics are completely FeoCK’ed.

We tried to save clean energy investors when we warned about Eos Energy (EOSE) at the end of October 2025. EOSE’s stock is Down –50% since. We believe the downside at T1 Energy is even higher.

T1 Energy & Evervolt’s Dirty Little Secrets – Now it’s time for the fun dirty secrets T1 & Evervolt never wanted you to know:

- Evervolt’s owner is Tan Chin Piaw (aka Simon Tan) – We uncovered a web of entities owned by Tan that have been connected to Trina Solar for >15 years

- In 2014, Australian regulators investigated a Tan owned entity for dumping Trina solar panels. We believe Tan set up the business to help Trina evade Aussie restrictions on Chinese ownership, aka it was another shanghai street hustle.Tan is connected to an alleged Chinese Criminal who reportedly had an Interpol Red Notice

- Singaporean docs reveal Evervolt was previously known as EliTE Solar Pte– EliTe Solar is on the US Antidumping List

- Chinese Corporate Docs seal the deal – they revealed Tan Chin Piaw has a direct connection to a Chinese State-Owned Enterprise (CETC)

Former T1 Energy employees and US Commerce Department Senior Officials also told us that they believed T1 Energy was set to be labeled a FEOC.

- “It’s ultimately Chinese IP…[the Administration] would look at it as a bullshit workaround”~Former US Commerce Dept Senior Official

- The Evervolt deal has obvious “tentacles back to China” ~Former T1 Energy Senior Executive.

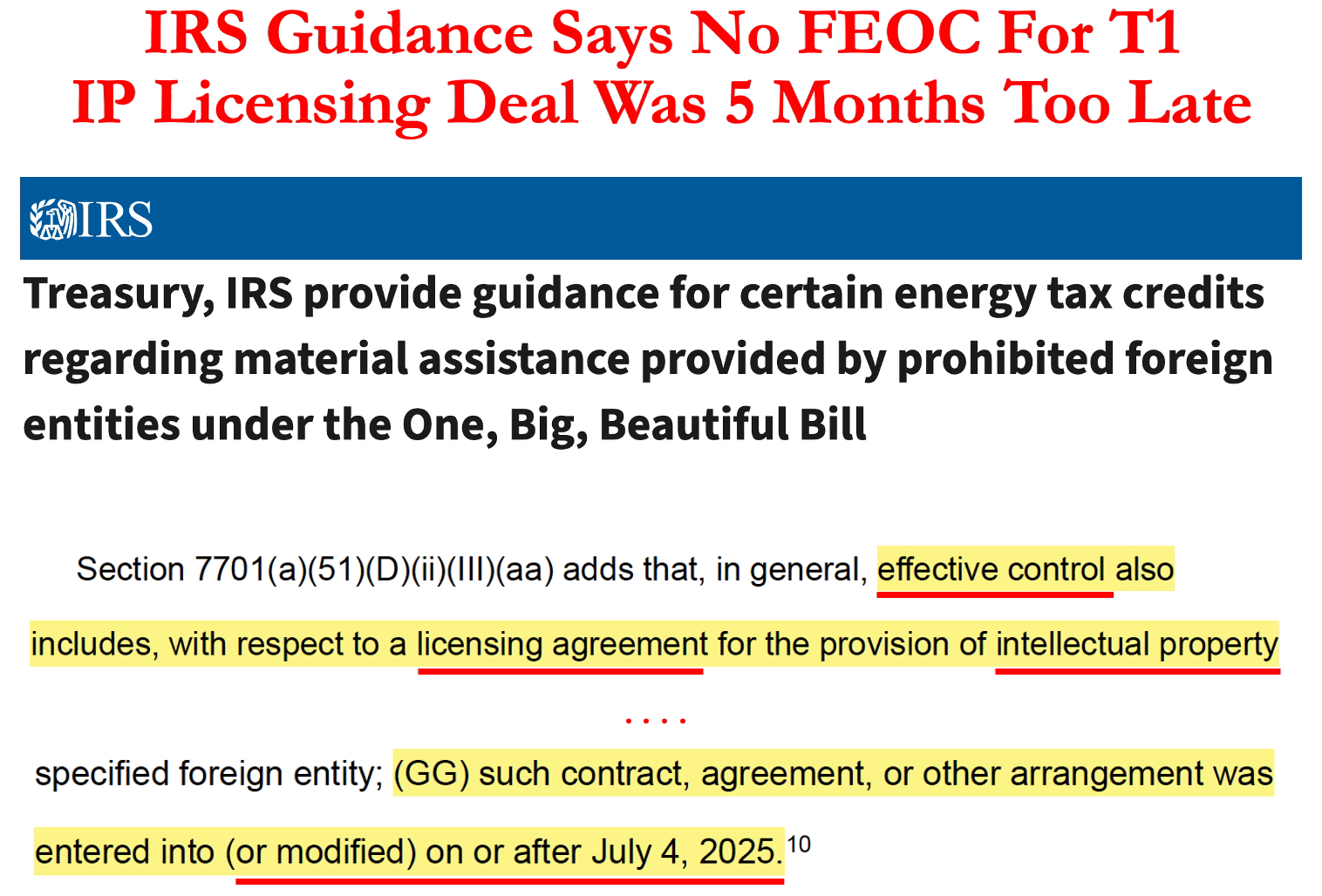

IRS Guidance killed T1’s 45-X Tax Credit Dreams – Feb 2026 IRS guidance put a July 4, 2025 deadline on IP licensing agreements occurring. T1 is further doomed to be non-FEOC compliant because the T1/Trina/Evervolt IP agreement transpired on Dec 29, 2025 – 5 months AFTER the deadline

- The one exception to IRS IP agreement deadline is a Bona Fide Sale. T1 is still FEOC’ed because we believe the Evervolt/Trina Solar IP shuffle is NOT a Bona Fide Sale for the following reasons:

- Tan & Trina Solar’s intertwined history shows Evervolt is not independent

- Trina Solar still owns/controls all the IP outside North America

- Singaporean records show Evervolt only had <$800,000 of capital. Evervolt lacked the $$$ to buy Trina’s IP at fair market values

- Evervolt still shows up as owning ZERO Patents. US Patent databases do NOT show any IP transferred from Trina -> Evervolt.

- Future IP developments & improvements still need to come from Trina Solar. Access to future IP + improvements from a Chinese Co’s automatically makes T1 Energy FEOC.

- T1 Energy spent $0 on R&D in FY 2025.

- Lawyers for tax credit investors told us the tax credit marketplace is closed.

- Insurance companies are carving FEOC exceptions and will no longer underwrite FEOC risk.

- Aka the tax credit gatekeepers, the lawyers and insurance co’s, are saying T1 and other Chinese connected solar co’s are FEOC’ed

Why a restatement to T1 Energy’s Financials should be coming soon?

- We believe Q1-2026 Profits overstated by $41.4 million. In Q1-2026 T1 Management made the aggressive judgement call to book tax credits they haven’t received despite the major tax law changes.

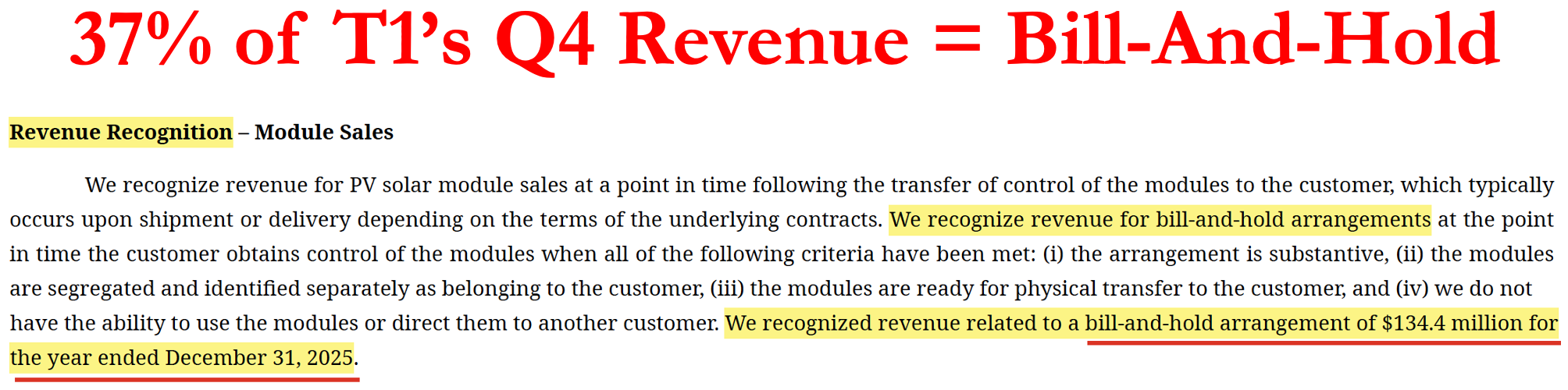

- 37% of revenue in Q4-2025 was Bill-and-Hold and from related party, Trina Solar. Bill-and-Hold is a major accounting red flag.

- We sent a letter to T1’s auditors regarding these issues.

T1’s economics are horrible w/out US Tax Credits. T1 is highly unprofitable

- T1’s future operating margins go from +6% to –31% without tax credits

G2 – T1’s US based solar cell factory is another key driver of future profitability.

- G2 is FEOC’ed too. G2 has the same Catch-22 IP problem. The G2 solar cell technology and machines are built on Trina created IP + rely on Trina’s future IP developments.

- Monthly drone flights over the G2 site have revealed very little progress since February 2026. As of early May 2026 G2 was still an empty dirt patch and there was a lot less going on.

- Experts estimate G2 is 12-18 months behind schedule yet management is still claiming it’s on schedule for a Q4-2026 opening.

Dilution coming soon – We believe T1 Energy had to maintain the illusion of tax credits in Q1 since TE needs to raise ~$220 million more to build G2.

The Freight Doesn’t Match the Weight! We uncovered Major discrepancies within T1s Import-Export Records. Our Import-Export records analysis revealed that many containers of suspicious T1<->Trina cargo actually had similar weights to container shipments of solar cells. T1 Energy has imported:

- Containers of “wood pallets” that weigh similar to solar cells

- Containers of “Packing Tape” that weigh similar to solar cells

- Containers of “Silicone Sealant” that weigh similar to solar cells

- Another obvious example is a large number of containers of “solar glass” (normally ~200% heavier than “solar cells”) but yet lots of the containers weigh similar to…solar cells.

T1 Energy has been subpoenaed by the DOJ, SEC, and even the Texas Lt. Governor has been calling for the Texas State Senate to investigate T1 Energy due to their Chinese ties.

We believe T1 Energy’s management has spun a fairytale about being FEOC compliant in 2026. Somehow they convinced all of Wall Street to believe them. T1’s entire economic future rests on a supposed IP Transfer to Evervolt that makes T1 FEOC compliant. But we think it’s nothing more than illusion. Evervolt and it’s sole owner’s past destroy the fallacy that Evervolt is independent. It clearly has long-term deep connections to both Trina Solar and the Chinese government. The emperor has no clothes.

We believe T1 is NOT FEOC compliant = No Future Tax Credits = T1’s Economics are F–k’ed…expect major accounting restatements coming soon.

Fuzzy Panda Research is Short T1 Energy

Fuzzy Panda Research and Fuzzy Panda “Affiliates” are short securities of T1 Energy (TE). Please see additional disclosures at the end of report and in our terms of service.

Whistleblowers, former T1 Energy employees, or people with more knowledge about T1 Energy’s suspicious import-export records can reach out to us by emailing at [email protected]. We will protect your anonymity.

Prologue – Short T1 Energy

FEOC 101 & Why it Matters: Not Compliant = No Tax Credits = Huge Losses

The key to T1 Energy and solar companies’ profitability lies in complying with new FEOC (Foreign Entity of Concern) rules. The new rules went into effect as of January 1, 2026. The US solar tax credit game completely shifted. There are five major categories of FEOC provisions (see Appendix F’ed – FEOC Rules for a primer on all the categories). Some items are easy to adjust to comply with FEOC rules (like % of Chinese ownership of the equity and debt), but there is one part that is very difficult, perhaps near impossible to get around. The IP. It’s not only about who owns the current intellectual property but more importantly where the future IP comes from.

Former T1 Energy executives confirmed that the IP is a Catch-22 that has doomed T1 to be labeled FEOC and why T1 is no longer eligible for US tax credits. To build competitive, comparably priced, and cutting-edge solar modules T1 needs access to new Chinese IP developments. But T1 getting access to Trina’s future IP and know-how forces T1 Energy to be forever labeled a FEOC company.

So what does it mean to be FEOC compliant – and why isn’t T1?

The FEOC rule is simple: If the IP has ties to China, then T1 is FEOC, and that means no tax credits, so T1’s economics are F—k’ed

T1’s technology originally came from its Chinese partner, Trina Solar, but in the days before the rules went into effect T1 tried what it probably thought was a clever work around to pass the FEOC IP test. It took place in the last days of December 2025

- Dec. 28, 2025: No question T1 Energy was a FEOC; all of T1’s IP was licensed from Trina.

- Dec. 29, 2025: T1 announced Trina “sold” the IP licensing rights to a Singaporean entity, Evervolt

It’s clever, but the strategy only works if no-one bothers to investigate Evervolt and the actual terms of the supposed deal. Unfortunately for T1 management, some Fuzzy Pandas did the due diligence.

We uncovered that Evervolt is not only connected to Trina Solar, but also that Evervolt’s owner is directly connected to CCP controlled Chinese entities. Oh and the IP that was sold, Trina Solar still has the rights to it outside the US and patent databases show that it was never transfered Trina Solar to Evervolt. T1 is FEOC’ed.

PART 1 – Evervolt Exposed – Short T1 Energy

T1’s New IP Partner Evervolt Exposed: Deep Connections to Trina Solar + Tied to Chinese Government = No Tax Credits = T1 is FeoCK’ed

- FEOC Compliance Won’t Happen – Trina Transferred IP to Singaporean Entity Named Evervolt

- Evervolt’s History of Connections to Trina Solar

- Tan Chin Piaw, Evervolt Owner, Helped Trina Solar Evade Aussie Rules on Foreign Ownership

- Chinese HK Corporate Records Reveal Evervolt is Directly Connected to the CCP

- Evervolt’s Owner Runs a Trina Distributor From the Same Office

- Evervolt was fka Elite Solar – Elite Solar Appears on US Anti-Dumping List

- Tan’s Former Business Partner – Alleged Chinese Criminal w/ INTERPOL Red Notice for Fraud

T1’s FEOC compliance hinges on a Trina Solar IP transfer to an unknown Singaporean company named Evervolt. We uncovered Chinese corporate documents that reveal Evervolt is tied to a sanctioned Chinese state-owned entity and Evervolt has a long history of connections to Trina Solar. We believe these documents prove that the IP transfer to Evervolt is not a “bona fide sale” and is more likely to be viewed by the US Government as a “Sham Transaction.” T1 will therefore not receive tax credits = NO profits.

Evervolt’s owner has long worked with Trina, and Evervolt appears to be little more than a shell through which the Chinese solar panel maker can pass its technology to T1. We have learned from conversations with former US Commerce dept officials and legal experts on tax credit sales that the burden of proof is on T1 to prove they are not Chinese. T1 will NOT be FEOC compliant.

In our investigation into Evervolt we uncovered:

- Evervolt’s owner, Tan Chin Piaw, has been a business partner of Trina Solar in multiple countries for >15 years.

- Social Media even highlights Tan & Trina’s business relationship in 2023

- Tan previously helped Trina get around Australian Foreign Investment rules. The Australian Government investigated Tan’s solar company for dumping Trina Solar modules in 2014

- Tan has at least 5 companies with Trina Solar Connections

- Chinese filings show Tan was named a director of a sanctioned Chinese state-owned entity, CETC, in October 2025.

- Singapore filings show Evervolt was controlled by 2 Chinese Directors

- Singapore filings show Evervolt used to be known as Elite Solar – Elite Solar currently appears on a U.S. Commerce Department Anti-Dumping investigation list.

- Tan’s past business partner reportedly had an Interpol Red Notice issued for his arrest for committing fraud.

Even former EliTe Solar Employees (Evervolt was fka EliTe Solar) directly told us that there were a few Chinese guys hidden behind the scenes at Evervolt.

It “all relates back to Evervolt … there’s a few Chinese guys … and these guys, over 20+ years behind the scenes, have been related to a lot of different Chinese companies that structure themselves in such a way to be, you know, non-Chinese companies with Chinese investors. So that’s what Evervolt is” ~ Former EliTE Solar Employee

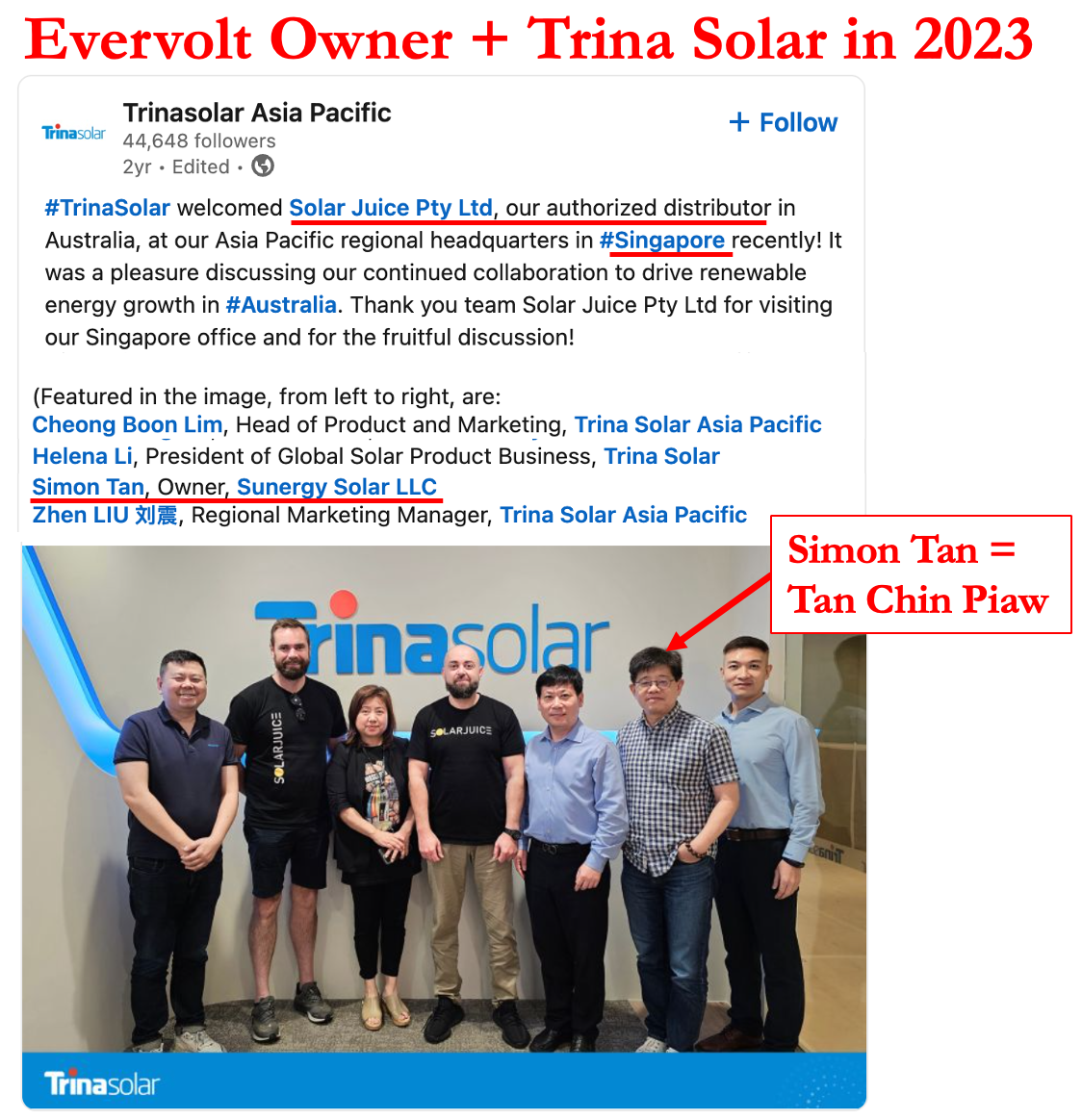

Evervolt’s Owner Featured in Trina Solar Social Media Post Back in 2023

T1 Energy’s FEOC compliance is dependent on Evervolt not being connected to the Chinese government and to Trina Solar.

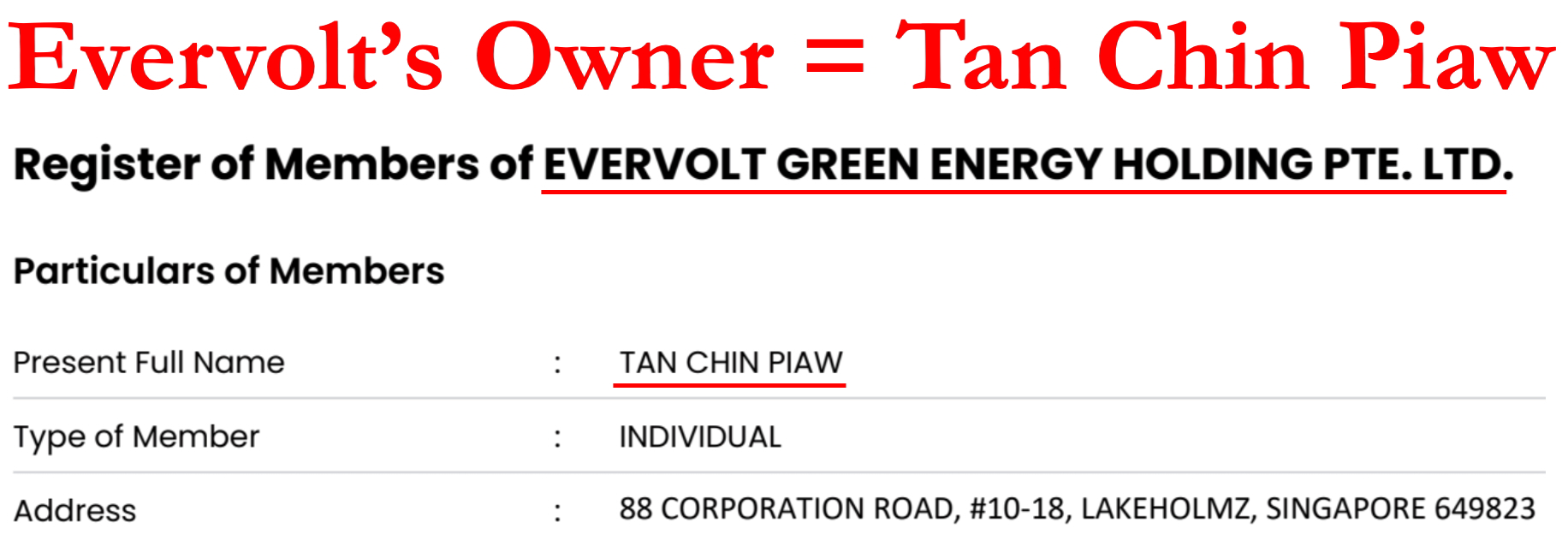

Singaporean business records show the only shareholder and owner of Evervolt is Tan Chin Piaw (aka Simon Tan) who is listed as a Singaporean citizen. Evervolt’s previous directors before Tan were both Chinese, but you can ignore that for now.

Below is an image of Tan Chin Piaw/Simon Tan when he was featured in Trina Solar’s LinkedIn post from September 2023. Tan visited Trina’s Singapore headquarters because his other business, Solar Juice, is an “authorized distributor” for Trina Solar in Australia. Hmm, that’s suspect, Tan Chin Piaw’s Evervolt is supposed to be a fully independent party to Trina Solar….the Trina connections begin.

Australian Antidumping Investigation Reveals Evervolt’s Owner Has >15 Year Relationship with Trina Solar

Uh oh, it turns out Tan Chin Piaw and Trina Solar go way back.

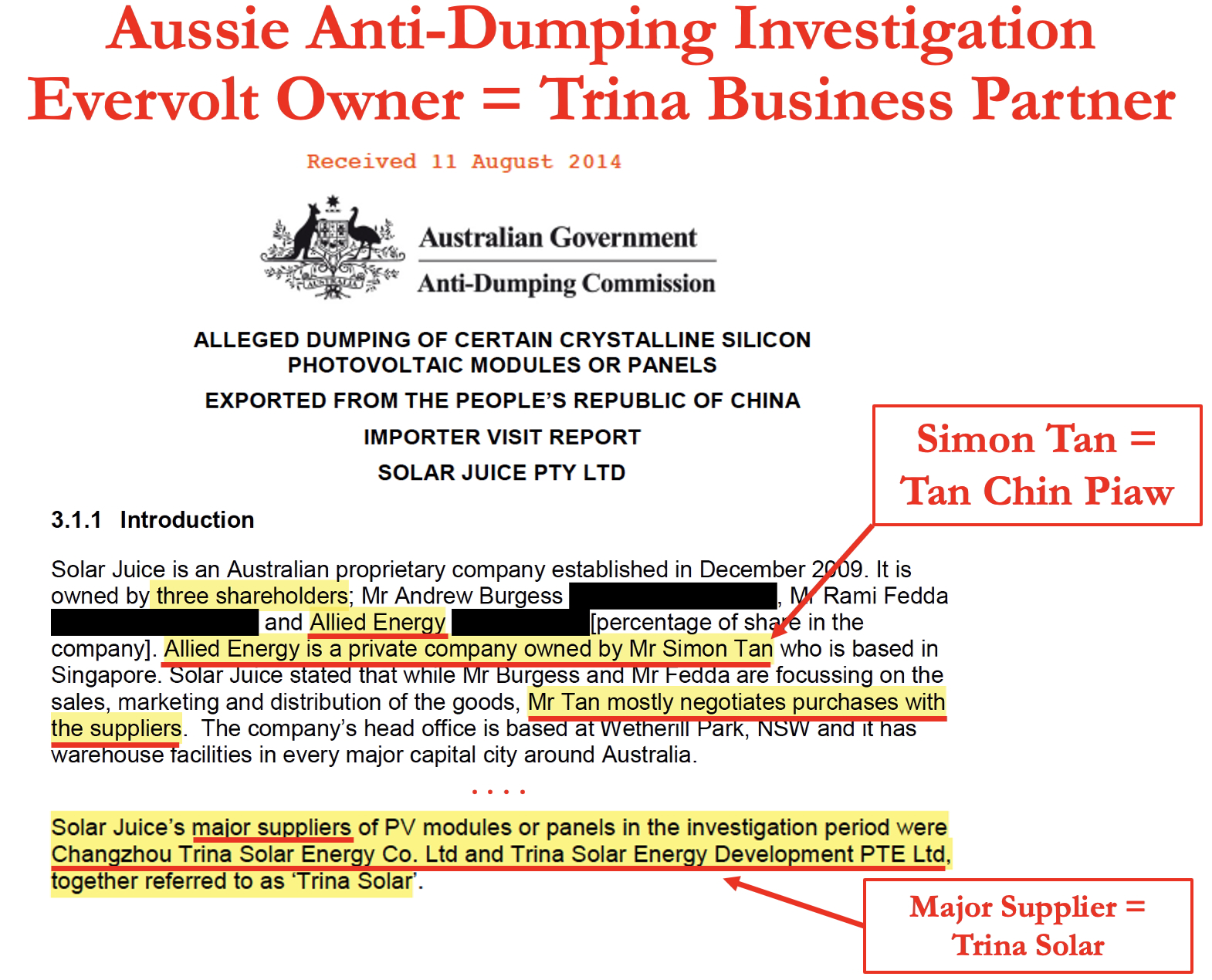

We uncovered an Australian Anti-dumping investigation that connects Tan & Trina 15+ years ago. It appears that Tan set up 2 “non-Chinese” companies to help facilitate Trina Solar navigating a crackdown on Chinese foreign investment in Australia.

Solar Juice, an Australian distributor of solar products was founded in 2009. Tan Chin Piaw was revealed as a major shareholder of Solar Juice during an investigation by the Australian Anti-Dumping Commission. The Anti-Dumping Commission stated that Tan’s primary role at Solar Juice was to “negotiate purchases with suppliers” … the main supplier was Trina Solar.

In 2008, the year before Tan founded Solar Juice to import Trina Solar modules into Australia, the Australian government had begun a large crack down on foreign investment, specifically Chinese ownership. We believe Tan Chin Piaw helped Trina create a work around to get past the Aussie regulations back then and he’s trying to do it for Trina again in the US with Evervolt now.

Chinese Corp Documents Show Evervolt’s Owner Tied to State-Owned Entity – Direct Connections to CCP

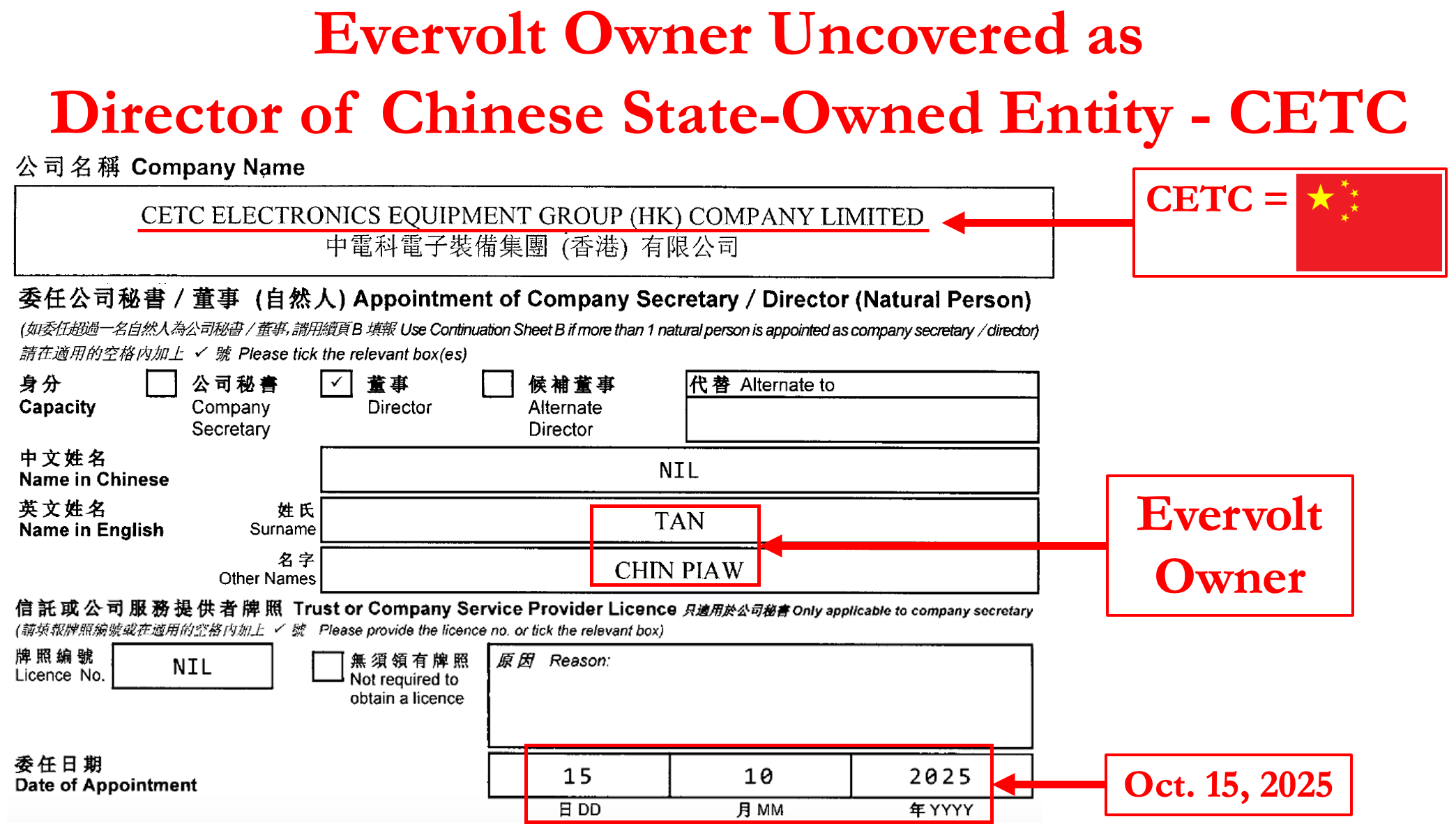

We pulled Chinese corporate records and uncovered that Evervolt’s owner, Tan Chin Piaw, has direct ties to a sprawling Chinese state-owned technology company CETC, China Electronics Technology Group Corporation. Tan Chin Piaw became the sole director of CETC’s Hong Kong subsidiary, CETC Electronics Equipment Group (HK) Company Limited. This appears to be a direct tie of Evervolt’s owner, Tan Chin Piaw to the CCP.

Not so Fun Fact – CETC is currently under U.S. Commerce Department sanctions that limit the business it can do with American firms.

The inclusion of “China” in the name of organizations like CETC (China Electronics Technology Group Corporation) signifies the company’s status as Central State-Owned Enterprises. CETC even describes themselves as a People’s Republic of China state-owned company on LinkedIn.

Evervolt’s Owner – Even More Connections to Trina Solar

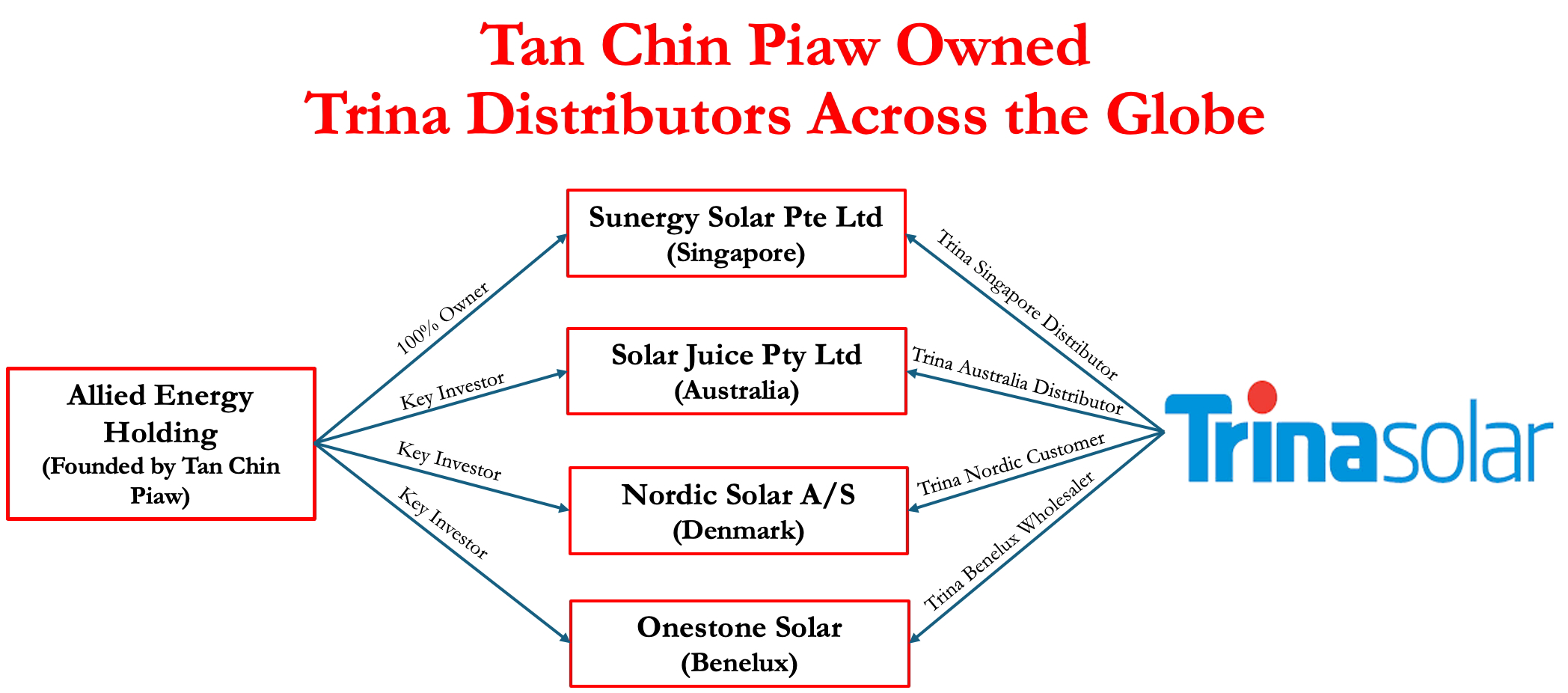

Evervolt is really FEOC’ed. We found that Tan Chin Piaw’s connections to Trina Solar don’t stop in Australia at Solar Juice. We uncovered that Tan Chin Piaw also has an investment firm named Allied Energy.

Via Tan’s investment company, Allied Energy Holding, we uncovered that Tan has been a distributor and wholesaler of Trina Solar products across the globe.

Tan Chin Piaw’s Other Connections to Trina Solar:

- Tan owns Sunergy Solar, a solar products distributor that sells Trina products. Sunergy Solar is even headquartered at the same address as Evervolt in Singapore.

- Tan is a major shareholder of Nordic Solar, a Danish solar park builder that relies heavily on Trina products.

- Tan owns Onestone Solar, a European Trina wholesaler in the Benelux countries.

- Reminder, Tan was a founding investor in Solar Juice, an Australian solar distributor whose main supplier was Trina Solar. Solar Juice even claims they’ve been “Trina’s longest-standing distribution partner” in Australia.

It Gets Worse – Evervolt Was Previously Called Elite Solar – Elite Solar Power is Listed on US Antidumping List

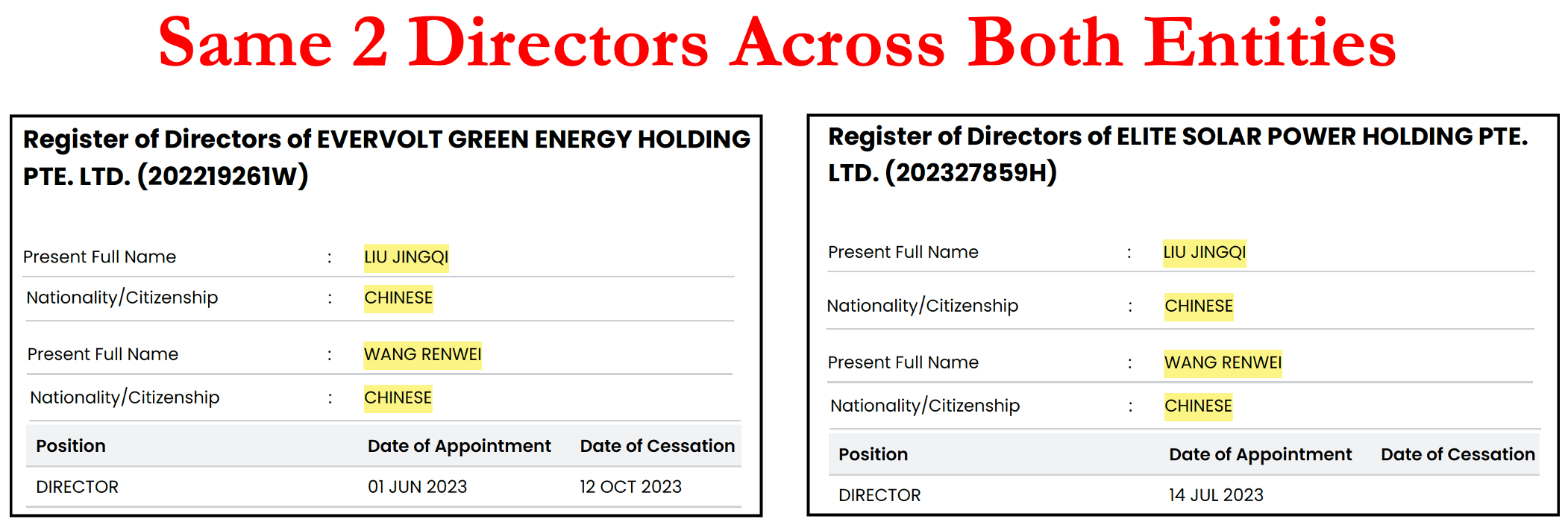

How could it get even worse? Singapore corporate records reveal Evervolt was originally known by a different name. Evervolt previously was called Elite Solar Holding PTE in 2022. There were also two Chinese nationals – Liu Jingqi and Wang Renwei – who served as directors the following year. Those same two Chinese gentlemen – are currently the only directors of Elite Solar Power Pte.

“EliTe Solar today is the successor of a truly government founded company, Chinese government founded company, called ET Solar” ~ Former EliTe Solar Employee

Elite Solar is better known for the fact that they have been added to the U.S. Commerce Department Antidumping List in January 2025. They are in good company with 12 of Trina’s entities in Asia being on the list. Elite Solar Power Pte was listed on the US anti-dumping list as a Chinese Entity.

Elite Solar Power is listed on the FY 2023 & FY 2024 US Antidumping and Countervailing Duty List.

INTERPOL Red Notice! Business Partners w/ Chinese Investor on “Most Wanted List” Accused of FRAUD

Turns out Tan Chin Piaw lives an exciting life, we uncovered that Tan Chin Piaw has Chinese friends in low places.

Tan Chin Piaw’s former business partner, Xiaofeng Peng, has a colorful history. Xiaofeng was accused of Fraud, and was placed on “China’s Most Wanted List,” and legal complaints and news reports state an Interpol Red Notice was issued for his arrest.

Background – Tan Chin Piaw had invested in Solar Power Inc (via his investment vehicle, Allied Energy Holdings) in 2014. Solar Power was the company Xiaofeng Peng was the CEO of. Xiaofeng Peng then seemingly returned the favor and invested in Tan Chin Piaw’s Australian solar distributor, Solar Juice in 2015. It reads like a you scratch my back, I scratch your back, type of situation.

PART 2 – IRS Guidance Shows T1 is FeoCK’ed – Short T1 Energy

IRS Guidance – No FEOC for You

- Trina IP ‘Transfer’ Occurred 5 Months AFTER The IRS Deadline

- License Agreement Includes Future IP Updates = NO Tax Credits

- Future IP Know-How Must Come from Trina Solar; Evervolt Lacks $ for R&D; T1 Spent $0 on R&D

The IRS guidance from Feb 2026 is crystal clear even if T1 Energy’s press releases about FEOC compliance are not. Any IP or patent license agreement that occurred or was modified AFTER July 4, 2025 with a specified foreign entity will NOT be FEOC compliant.

The Trina Solar -> Evervolt -> T1 Energy IP License Agreement was modified on December 29, 2025. It appears they scrambled to make the agreement appear FEOC compliant in the last three days of FY 2025, but the new IRS guidance suggests T1 Energy was already five months too late.

We spoke with a former senior member of the Department of Commerce who told us that the current US Administration are going to assume solar companies are Chinese until they prove it otherwise. We described the supposed Trina-Evervolt IP Sale and the official told us it’ll be viewed as a “Bullshit workaround.”

“That’s just a workaround. It’s ultimately Chinese IP…They [US Government] would look at it as a bullshit workaround” ~ Former US Department of Commerce Official

T1’s IP Deal Occurred 5 Months AFTER the IRS Deadline = No Tax Credits

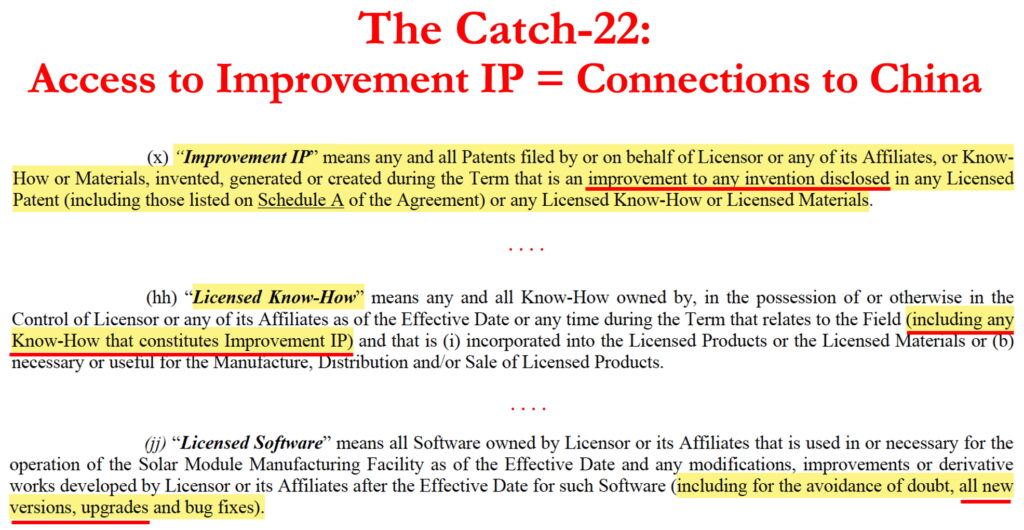

Future IP & Know-How Included in IP Deal – IRS Guidance Says Deals Requiring Future “Know-How” = Still Tied to Chinese

“If the deal was done where they didn’t have access to the improvements, I would be shocked. That wouldn’t be very competitive. If they did, that would be a red flag if they do have access to the improvements. Well, there again, you’re still tied to the Chinese then” ~ former T1/Freyr Senior Executive

Former T1 Energy/Freyr executives told us a huge concern of theirs was whether T1’s IP deal could include access to improvement IP and know-how.

It was a Catch-22—if the deal didn’t give T1 access to Trina Solar’s IP improvements than T1 Energy was screwed because it will be relying on old technology, and if T1 did get improvement IP then they would obviously still tied to the Trina Solar and reliant the Chinese. Access to IP Improvements = Not FEOC compliant.

The T1<–> Trina Solar Evervolt IP deal specifically highlights T1’s access to IP Improvements:

- Future Improvement Patents

- Improvement of Know-How

- New versions & upgrades of Licensed Software

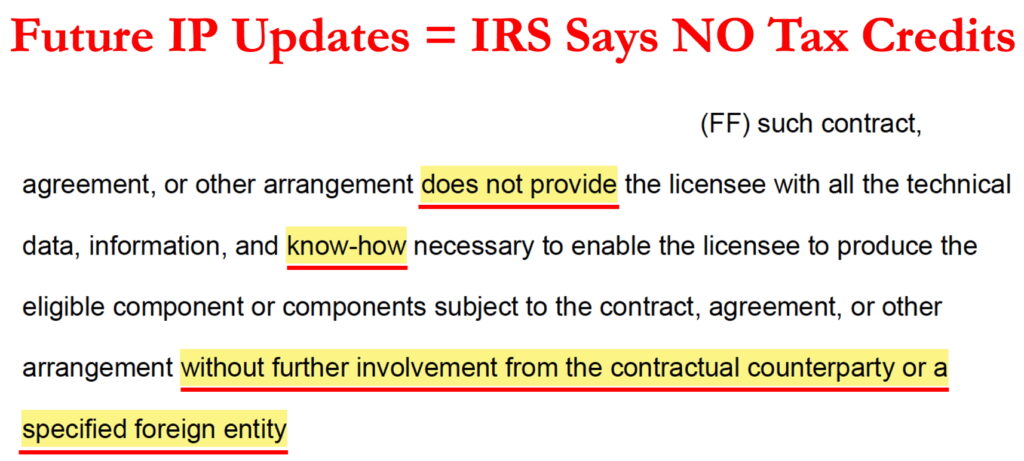

The Feb 2026 IRS Guidance further confirms that any IP agreements that require future know-how from a specified foreign entity would make a US company NOT FEOC compliant.

T1 Spent $0 on R&D in 2025 – Future IP must come from Trina

T1 Energy discloses spending $0 on R&D in FY 2025. Tan Chin Piaw and Evervolt have ZERO patents assigned to them. Evervolt appears to have never even applied for a patent and Evervolt’s Singapore disclosures show the company only has $800k million of contributed capital, so Evervolt lacks the capital to do R&D.

It’s obvious. Any future IP improvements must come from Trina Solar.

PART 3 – Gov’t Experts & Formers Call BS – Short T1 Energy

IP Transfer is NOT a Bona Fide Sale

- Experts Call It “A Bullshit Workaround” that “Doesn’t Pass the Smell Test”

- Formers See Obvious “Tentacles Back” to China

Former senior officials at the Department of Commerce told us that an IP deal structured similar to the T1-Evervolt-Trina Solar deal “will not pass the smell test” and would be viewed as a “bullshit workaround.” They also told us that the burden of proof falls on T1 Energy and Evervolt to prove it’s not a “Chinese Front” and that the current Trump administration hates solar to begin with.

“Creative structuring will not pass the smell test… I think that would be, you know, that’s just a workaround. It’s ultimately Chinese IP. [The US Commerce Department] would look at it as a bullshit workaround… if [the Trump Administration] see a solar company, they’re going to assume it’s a Chinese front organization until that company is able to prove otherwise.” ~ Former US Department of Commerce Senior Official

The lawyers for the 45X tax credit investors told us they don’t believe it either. So no one will take the risk to “buy it.”

“Some companies think having an intermediary [like Evervolt] should help. But we don’t buy that” ~ Legal Authority on Tax Structuring

What is a Bona Fide Sale? Trina’s IP Transfer Fails the Requirements

We will briefly entertain the idea of the Evervolt-Trina Solar IP transfer being a bona fide sale below and explain why we believe those claims won’t pass the US government’s “bullshit” detector.

Note to Bulls – Even if somehow the IP Transfer is magically was viewed as a bona fide sale then T1 will still be viewed as NOT FEOC compliant due to T1’s use of and reliance on future Trina Solar IP and Know-How…so don’t get your hopes up.

Based on Feb 2026 IRS guidance the only chance for Evervolt-Trina IP transfer to potentially have Evervolt viewed as non-FEOC is if the IP sale is considered a bona fide sale. In that situation Evervolt could potentially get an exemption to the IP transfer deadline of July 4, 2025.

If it were a bona fide sale then the IP transaction would need to occur at:

- Fair Market Value and be an

- Arm’s Length Transaction between Independent Companies

Fair Market Value – Highly Unlikely

T1 Energy told us at an investment conference that they bid for Trina’s IP but lost to Evervolt. Which is strange since Evervolt only had <$800k of “Paid in Capital” according to Singaporean records. How could T1 not have outbid Evervolt if there truly was a bidding process?. Especially when T1 spent >$50 million in legal fees in 2025. But Trina was willing to give it all away for <$1 million? We doubt it.

- Trina Solar & T1 Energy could easily clear this up by disclosing the actual amount paid as well as the list of all the patents that were supposedly sold.

Is Evervolt Independent from Trina? FeoCK No

Come on, did you read nothing above this? We have already demonstrated multiple ways that Evervolt and its owner are deeply intertwined with Trina Solar and the Chinese Government. If you still think Trina Solar and Evervolt are completely independent we suggest you go back to the beginning of this report and try again.

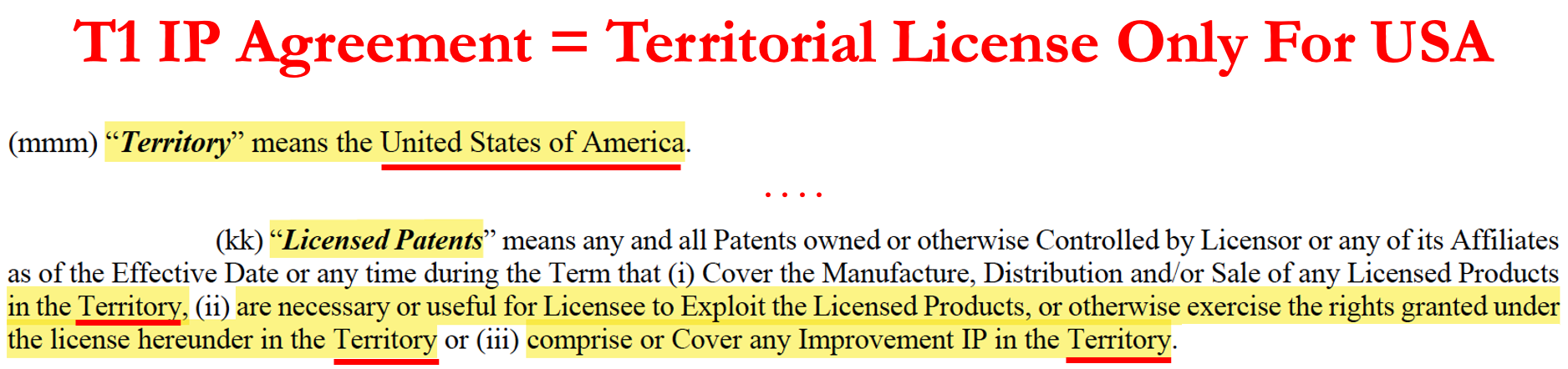

“Arm’s Length” Does NOT Equal Tentacles back to China – T1’s Territorial License is Only for USA

Former T1 employees say the IP Transfer agreement has obvious “Tentacles back” to Trina Solar, since T1’s license agreement is restricted to one geography.

“It’s not as if they sold their entire technology suite to [Evervolt]. [Trina Solar] sold what is probably just the licensing rights to the technology in a certain geography, which may be defined as North America … the point is it’s still got tentacles back” ~ former Freyr/T1 Senior Executive

The T1 Energy IP agreement only grants a Territorial License for IP in the United States. In the updated Dec 2025 agreement, we found no changes to this geographical restriction.

In other words, this indicates that Trina Solar can still utilize the IP everywhere else. Trina can still use the IP for production of solar products across the globe. Can it really be a bona fide IP Sale if Trina Solar still has the IP rights in 99% of the countries across the globe?

PART 4 – Horrible Unit Economics w/Out Tax Credits – Short T1 Energy

No Tax Credits = No Profits: T1’s Horrible Underlying Unit Economics

- T1’s Economics Depend on Tax Credits; No Tax Credits Due to FEOC = Massive Loses

- Rules Changed for FY 2026 – Say Goodbye to Hundred’s of Millions of Tax Credits

- Lawyers for Tax Credit Buyers Told Us Deals Won’t Happen – FEOC Risk is a Non-Starter

Becoming FEOC compliant is crucial for T1 Energy to go from a money losing business to a profitable one.

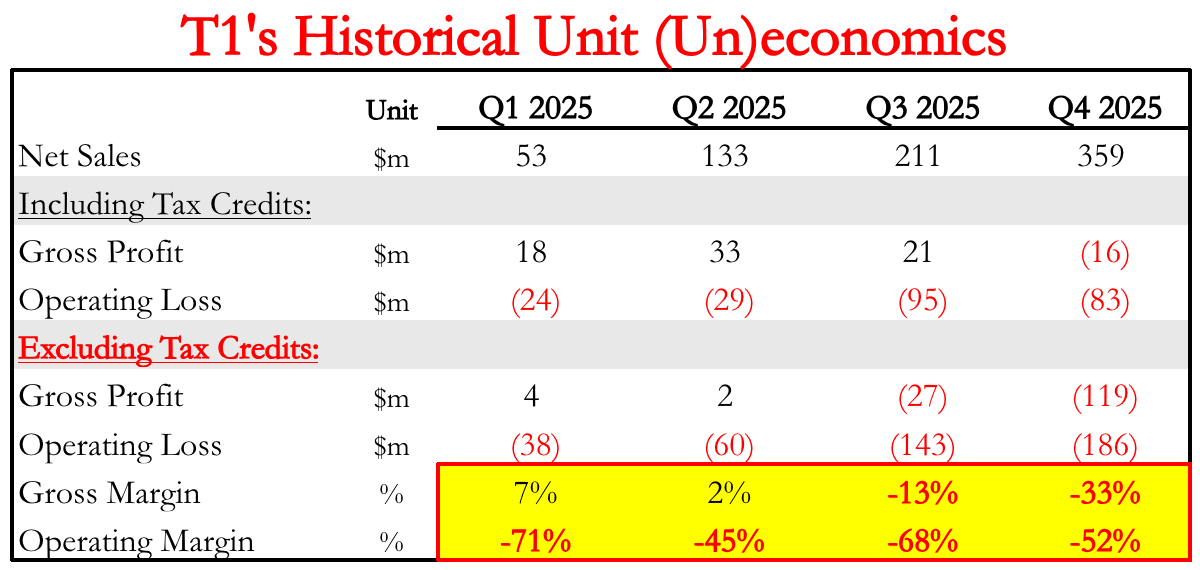

T1 claims they will have double digit margins but that’s only due to US Tax Credits which are offset against COGS. In FY2025, T1 reported gross margins of 7%. But what they didn’t report was that gross margins would’ve been –19% without tax credits.

Investors mistakenly believe that since T1 Energy sold tax credits at the end of FY 2025 that T1 will be able to sell them in 2026 too. But the rules have changed starting in 2026.

Trump Changed the Rules in 2026 – Chinese Companies Will Be FEOC’ed Out of Tax Credits

“If you can’t get FEOC compliant you can’t generate tax credits. You’re screwed economically” ~ former Freyr/T1 Senior Executive

T1 received tax credits in FY 2025 but investors are up for a big surprise if they think T1 will qualify from 2026 onwards. Prior to the OBBBA being passed into law in July 2025, 45X tax credits were NOT subject to FEOC restrictions. But since the passing of the bill, the heightened restrictions kick-in starting in taxable years after 2025 meaning any solar cells or modules sold from January 1, 2026 and onwards will have to be FEOC compliant. And T1’s modules are not.

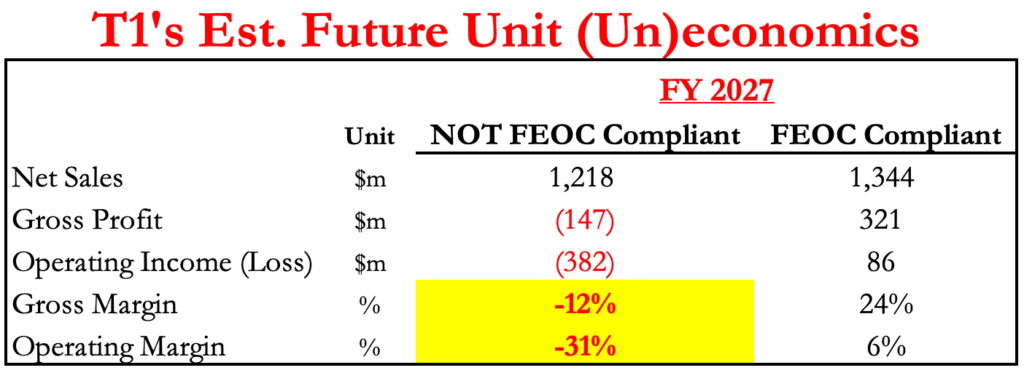

T1’s Future Economics are F–k’ed Without Tax Credits

Without tax credits, T1 will be a massively unprofitable business. Not only will they not get the 45X tax credits but customer demand will be very low. Customers receive 48E investment tax credits worth up to 30% of their project costs + 10% bonus for using domestic content on eligible projects when purchasing from American companies.

Without 45x tax credits T1 will lose out on $0.11 per watt in tax credits.

- $0.07/watt for solar modules – from G1

- $0.04/watt for solar cells – from G2

The 45X tax credits going away changes est Operating Margins from +6% to NEGATIVE 31%.

T1’s Historical Unit Economics Look Horrible w/Out Tax Credits

In FY2025, T1 sold modules for $0.28 per watt and their COGS (without tax credits) were $0.33 per watt. T1 Energy loses money with every additional solar module they sell.

After backing out the tax credits T1 accrued each quarter, you can see how gross margins flipped negative in Q3 and were razor thin in Q1 & Q2.

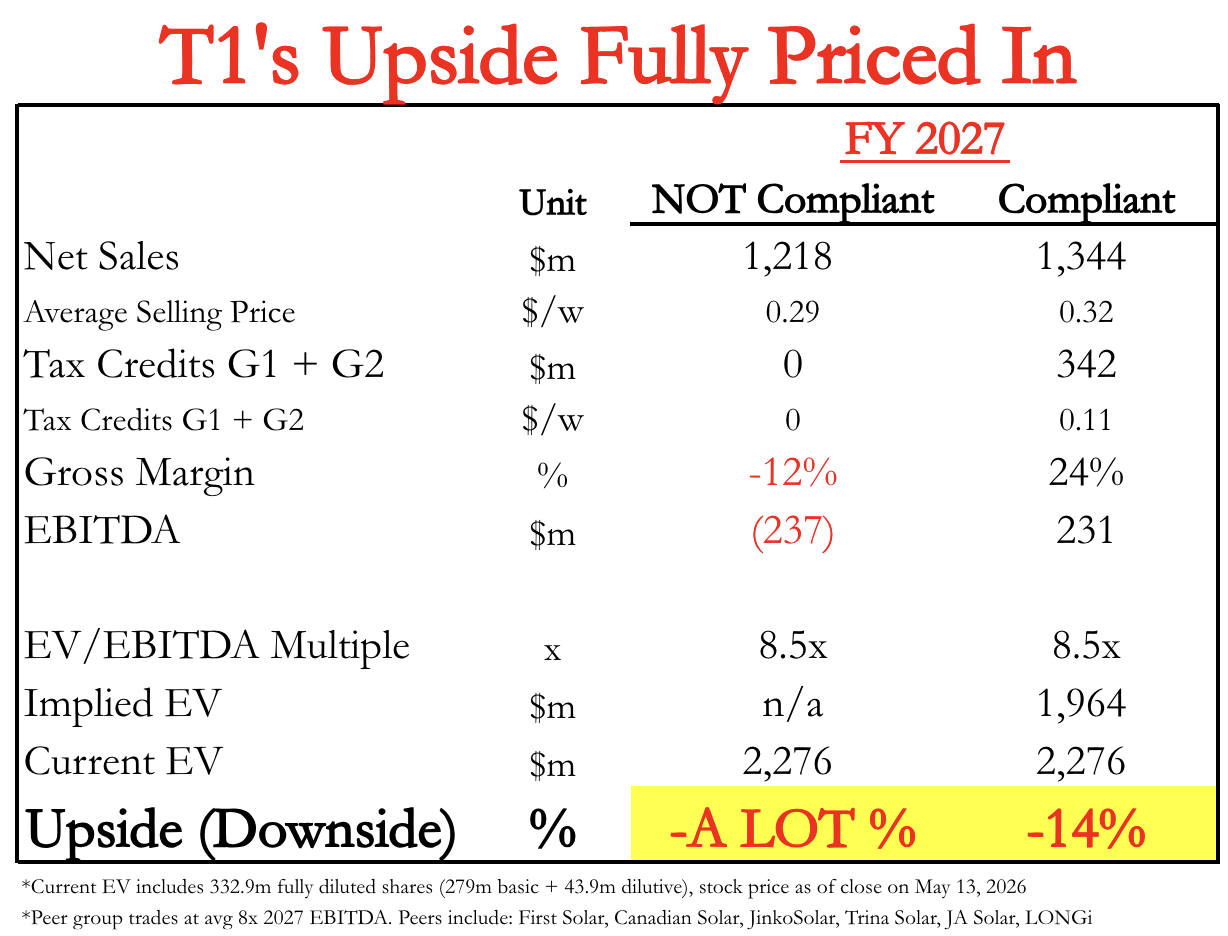

T1 Priced for Perfection. Plenty of Downside Risk!

T1 is currently priced for perfection as if the company was certainly going to be FEOC compliant and receive tax credits. Looking at FY 2027 we have generously assumed that G2 would open on time and applied an above comps 8.5x EBITDA multiple (peer group average trades at 8x) to our est we find that most of the upside for T1 shareholders is already priced in.

T1 to Lose Tax Credits in 2026 – Hundreds of Millions Going Away

Without FEOC compliance, T1 will lose out hundreds of millions of tax credits. For 2026 alone T1 will lose an estimated $224 million based on consensus estimates of ~$925 million of Sales which equates to ~3.2GW.

The math is simple: 3.2 billion watts x $0.07/watt = $224 million.

To have any hopes of getting those credits and that cash, T1 needs a non-FEOC source for solar cells pronto, and to sort out their IP license agreement. But import records show no evidence of T1 purchasing cells from FEOC compliant companies, and while it has a minority stake in Talon PV – an American cell maker – that company isn’t expected to be producing cells until 2027. Meantime, our drone footage of T1’s G2 facility makes it appear unlikely to be operating until well into 2026, at the earliest.

Lawyers for Tax Credit Buyers Say The Market is Dead & No FEOC Risk is Worth it; T1 Can NOT Sell Future Tax Credits

“The whole picture is that the factories remain in the vice grip of this Chinese company” ~ Legal Authority on Tax Structuring

Tax credit investors are the sophisticated investors in this market. They are the gate-keepers that decide the cost of taking on the risk that T1 Energy’s can actually earn tax credits starting in 2026 and will be FEOC compliant or not. We spoke to their lawyers who analyze the FEOC compliance risk behind the scenes. Their legal counsel told us in way too many words (they are paid hourly) that it is likely that NO Tax Credit investors will accept T1 Energy’s FEOC risk from FY 2026 onward.

Tax credit/FEOC risk lawyers also told us that tax credit buyers are no longer comfortable assuming the sellers point of view about whether or not they are FEOC compliant.

“The [tax credit] buyers are not comfortable assuming the seller [T1] has done proper scrubbing of effective control language” ~ Legal Authority on Tax Structuring

But as all things with T1, it gets even worse, it turns out the insurance companies are carving out FEOC risk from their policies. Insurance companies are excluding FEOC risk from the policies they underwrite for tax credit investors. Simply put insurers don’t want to get FeoCk’ed either. We learned that right now underwriting FEOC risk for T1 energy is essentially even worse for the insurance co’s than insuring an oil tanker going through the Straight of Hormuz. Because your balance sheet is going to get blown up.

“Tax insurers are carving our FEOC risk from their policies” ~ Legal Authority on Tax Structuring

Independent solar industry consultants told us the same.

“The tax equity insurance underwriters aren’t comfortable with these levels of FEOC risk and they’re not funding” ~ Solar Industry Consultant

PART 5 – Short T1 Energy

Why do Patent Databases Show IP Still Owned by Trina Solar NOT Evervolt?

- Trina Still Listed as Patent Owner in US, Asia & Europe

- Where is the List of Sold IP? SEC FOIA’s Show The IP Transfer List was Never Publicly Filed

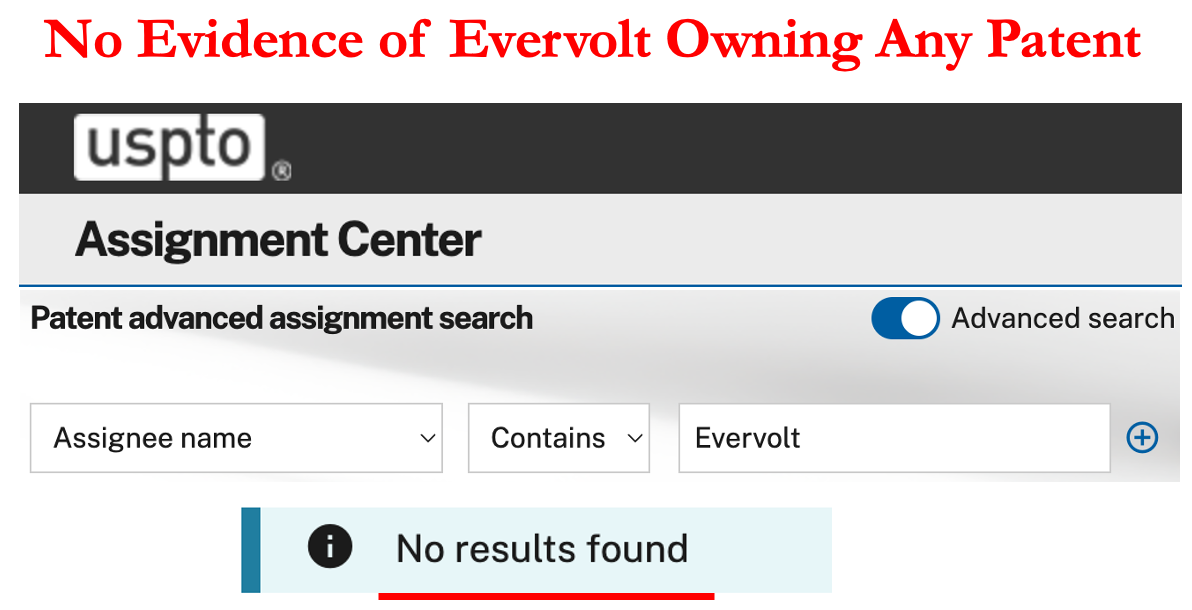

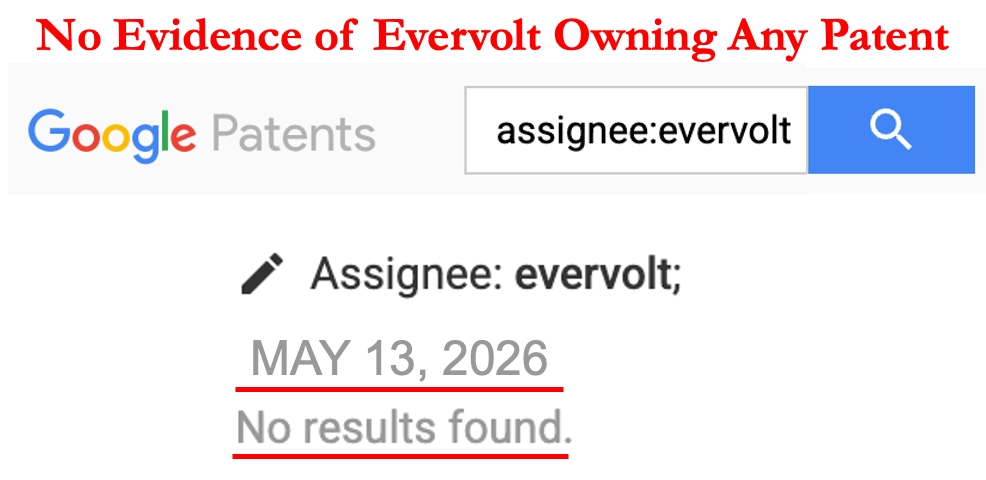

U.S patent databases still list Trina, not Evervolt Green Energy, as the owner of essential solar patents. Patent databases show ZERO patents assigned to Evervolt.

We engaged an IP lawyer to get their opinion, and they told us this situation was highly unusual if the IP was actually sold and transferred to Evervolt. The lag time for a new assignee to show up in public patent databases is usually a couple days not 3 months.

Trina, Not Evervolt, Still Listed in Global Patent Databases

Trina, not Evervolt, is the named owner of every single patent we could find in every database we could access in the U.S. and around the world. Evervolt does not currently appear to own any patents anywhere.

Why do Google & the USPTO patent databases not show patent transfers from Trina Solar to Evervolt?

Even if old patents are eventually transferred, the lack of any IP currently belonging to Evervolt shows they aren’t capable of developing any improvement IP on their own, proving that future IP improvements will have to come from Trina Solar in the future.

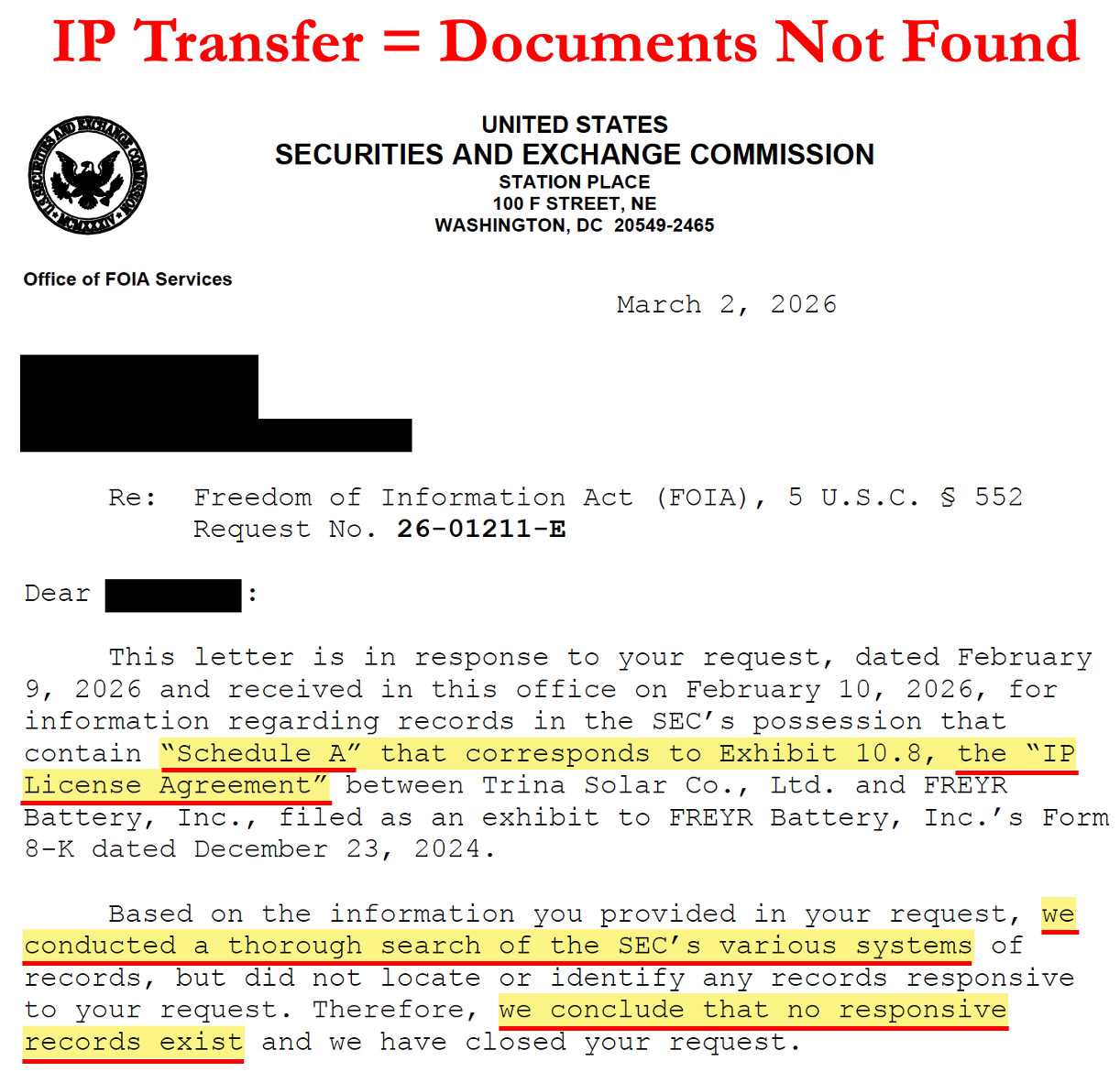

SEC FOIA Shows No Record of List of Transferred Patents – Are they Hiding Something?

T1’s filings say details of the exact patents it licensed from Trina/Evervolt are listed in an attachment called “Schedule A.” But the list isn’t available in SEC filings so we FOIA’d the SEC to get a look at Schedule A. The SEC’s response? The records do NOT exist.

That means that the SEC has no record of what patents T1 licensed from Trina/Evervolt.

If the IP has actually been sold then that raises questions for T1 Management:

- Why aren’t T1 Energy and Trina Solar disclosing the list of patents with the patent numbers that have actually been transferred? Are you hiding something?

- What price did Evervolt actually pay? What did Evervolt actually buy?

PART 6 – T1’s Suspicious Import-Export Records – Short T1 Energy

Suspicious T1 Imports – Freight Doesn’t Match the Weight – Is Trina Hiding their 2026 Shipments of Solar Cells to T1?

- Major Red Flag – Analysis of Customs Records Show Container Weights Don’t Match Declared Freight…but It Matches the Weight of Solar Cells

- Wood Pallets, Packing Tape, and Sealant that Weighs the Same as Solar Cells?

- T1’s Component Analysis = ~80% Material Costs From Non-FEOC Compliant Suppliers = No 2026 Tax Credits

We analyzed all of T1’s import records and found some suspicious discrepancies. Many of the container weights don’t match the description of the cargo. These “anomalies” have continued in FY 2026.

Companies, especially solar ones, have been known to lie/write misleading manifests for shipments. But there are two things that are impossible to fake, the number of containers and the weight of them.

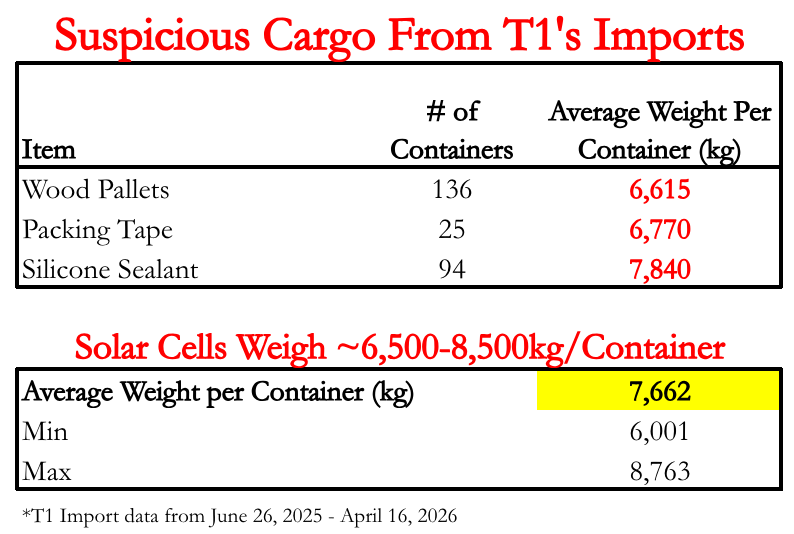

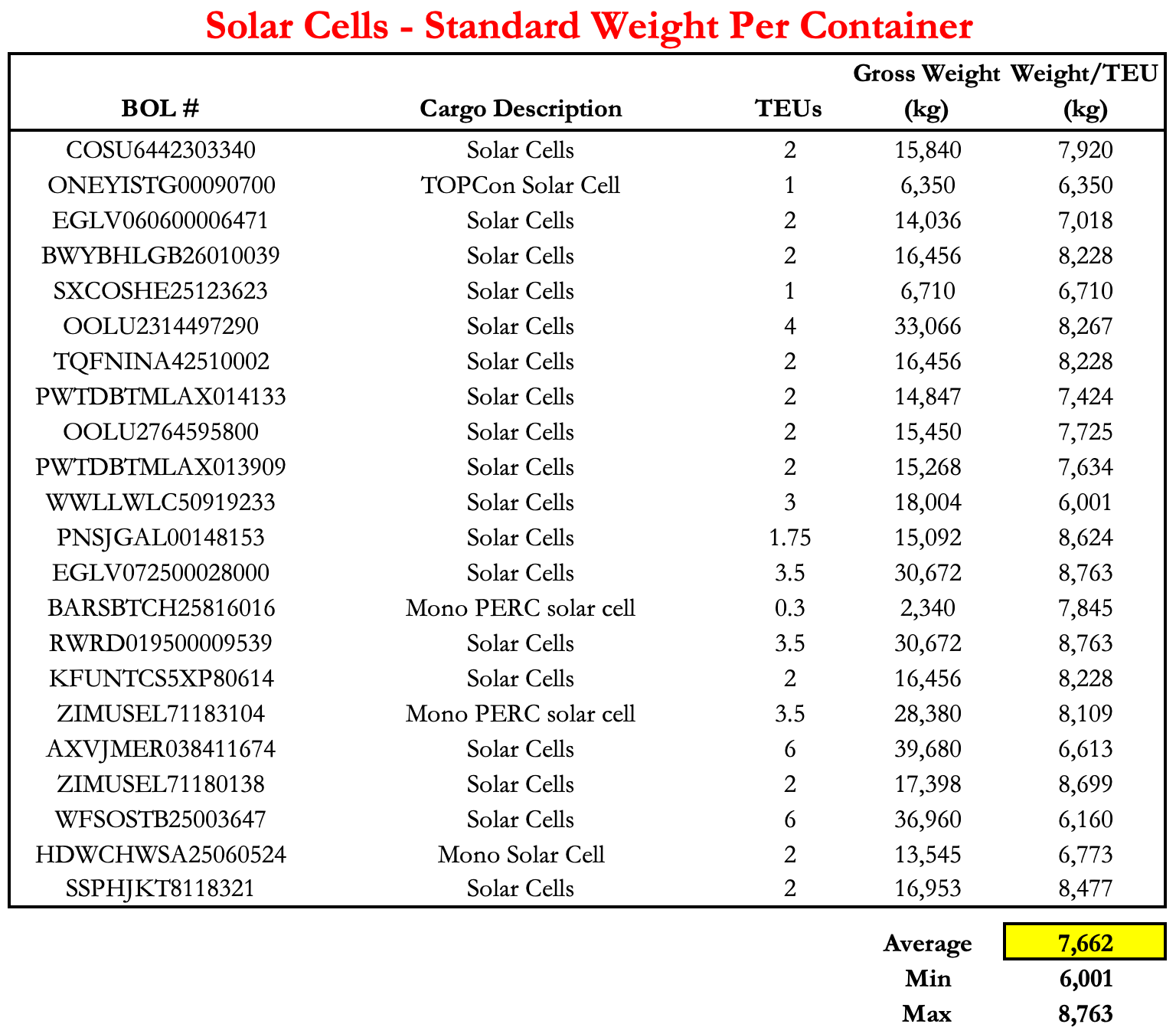

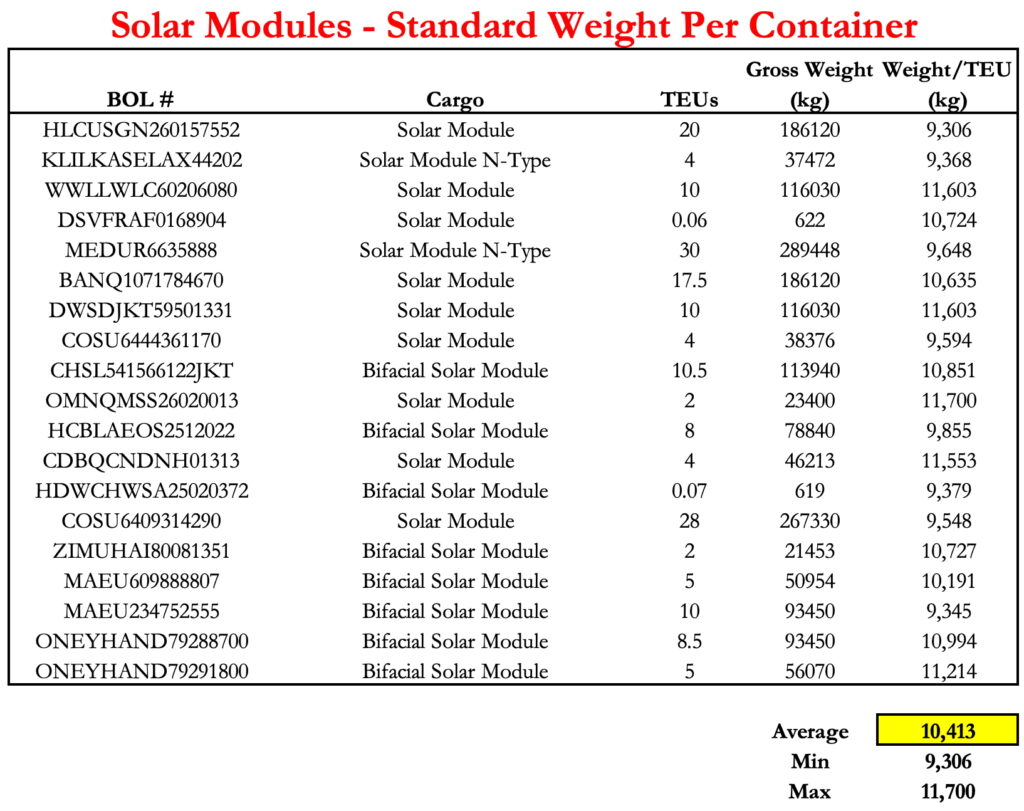

We reviewed >50 solar cell shipments and on average they weigh ~7,700kg per container. We found no records of T1 declaring that they are importing solar cells. However, we found a whole lot of container shipments from Trina Solar to T1 Energy that coincidentally match the approximate weight of containers of solar cells but also weigh way more or less than the stated cargo.

Suspicious Items in T1’s Import Data – Weight Doesn’t Match the Freight

- Wood Pallets – similar weight to Solar Cells

- Packing Tape – similar weight to Solar Cells

- Silicone Sealant – similar weight to Solar Cells

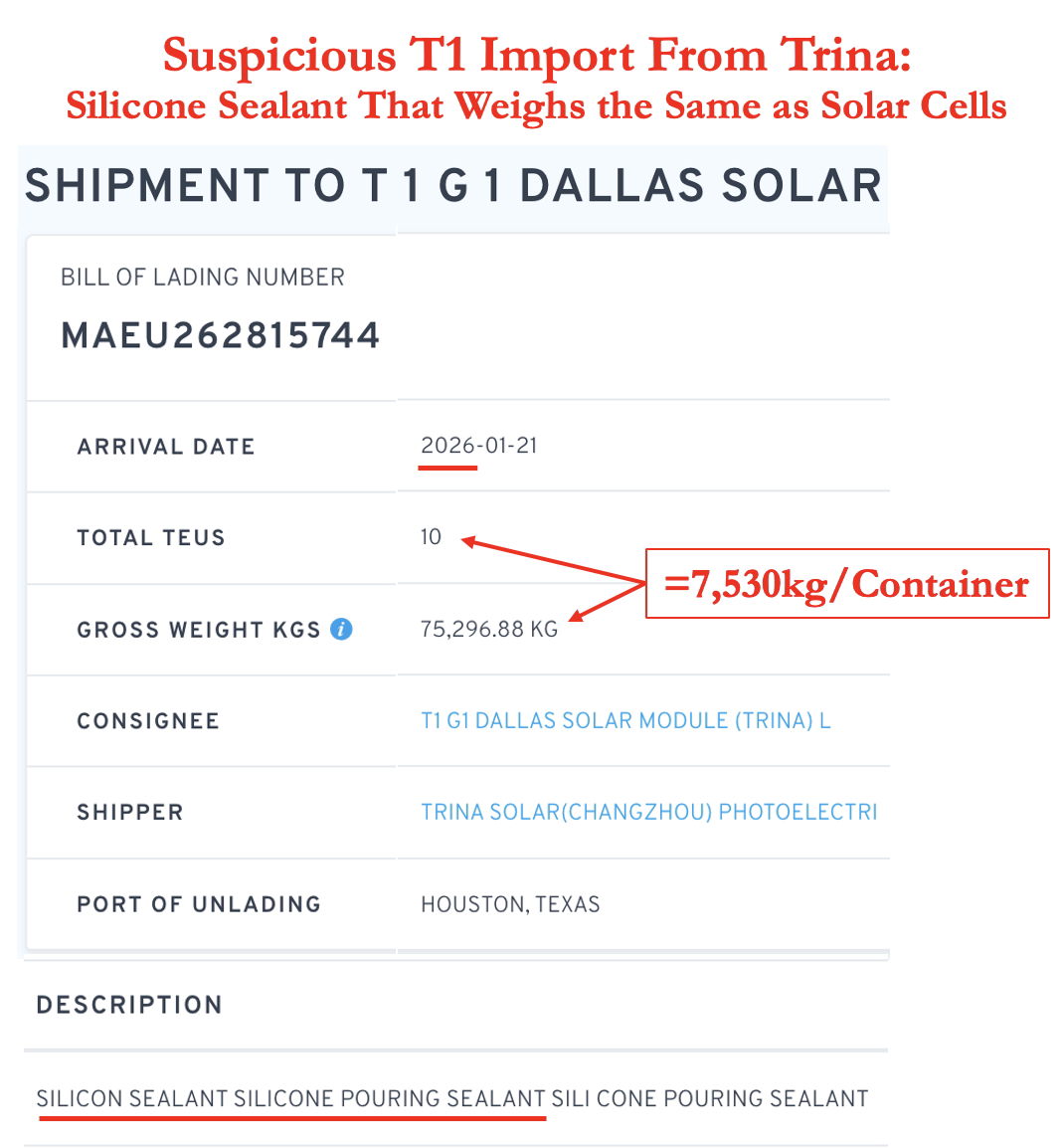

An example includes a shipment of silicone sealant that arrived at T1’s G1 factory on Jan. 21, 2026. This shipment (MAEU262815744) weighed 7,530kg/TEU, about the same as solar cells.

More Suspicious Items in T1’s Import Data – The Lightest Solar Glass Ever? Or are these Solar Cells/Modules?

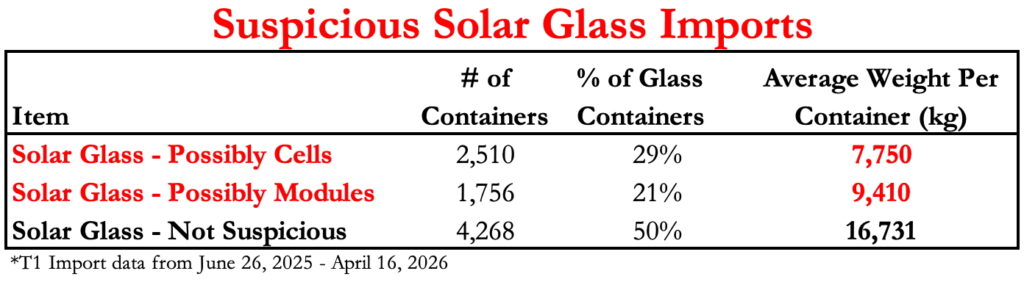

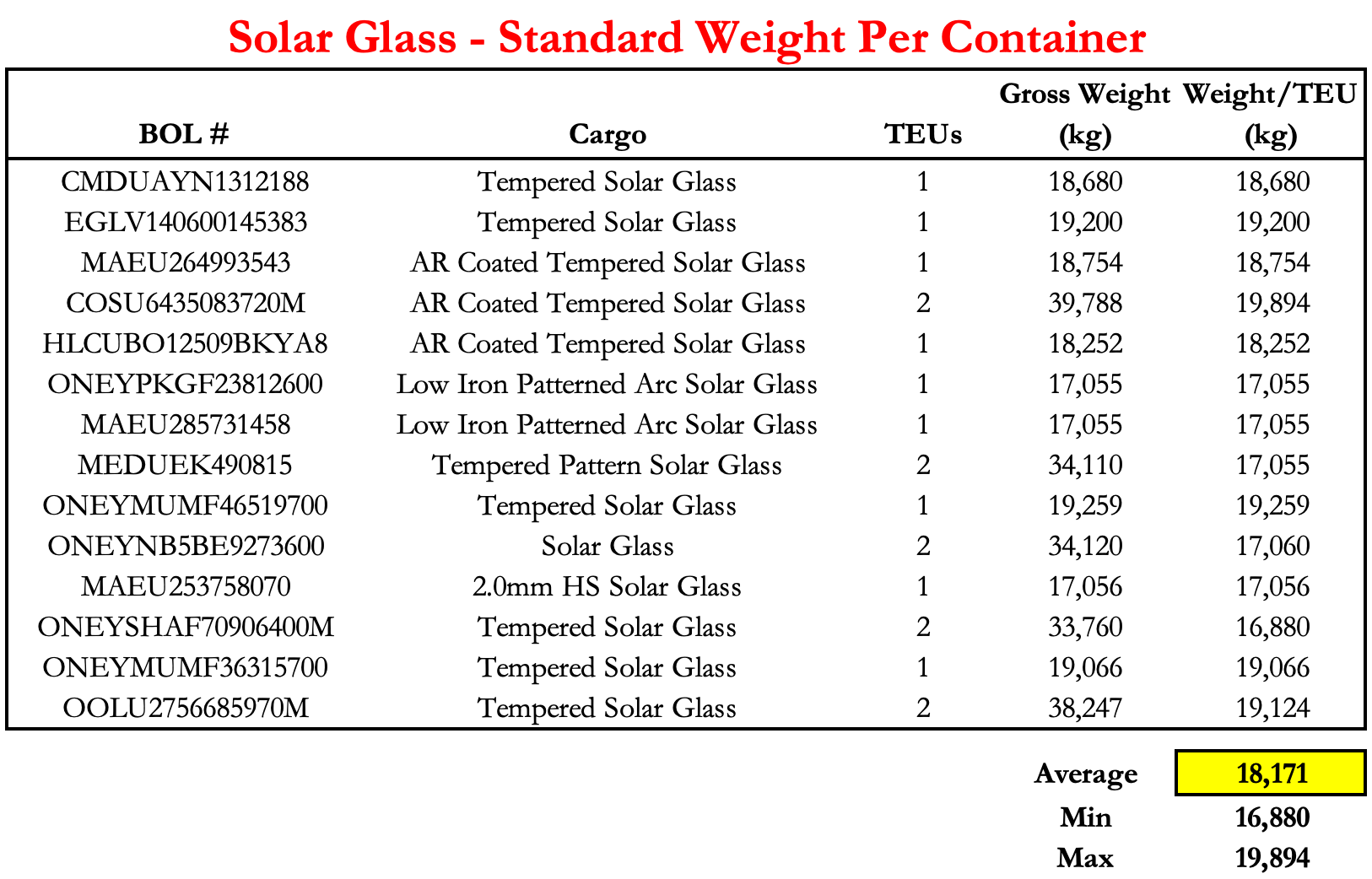

We believe Culper Research was onto something when they questioned all the Solar Glass Shipments. They made a valiant effort at flagging the anomaly but investors failed to listen. We analyzed the solar glass shipments and found that 53% of the Solar Glass shipments had container weights that are large anomalies vs. what solar glass should weigh.

Either Trina & T1 are very inefficient at packing solar glass, or investors should be very suspicious of something else going on, perhaps even tariff evasion?

53% of T1s Solar Glass Containers Weigh the Same as Solar Cells & Solar Modules NOT Solar Glass

We studied other companies import records and found that on average Solar Glass weighed 16,800-19,900kg per container (container defined as 1 TEU – a 20ft container & a 40 ft container = 2 TEUs). On average, solar glass containers weigh ~130% > solar cells and solar glass weigh ~85% > solar modules. (See Appendix X-Import-Export for more details.)

- 29% of Solar Glass Shipments – similar weight to Solar Cells (7,662kg per container)

- 21% of Solar Glass Shipments – similar weight to Solar Modules (10,413kg per container)

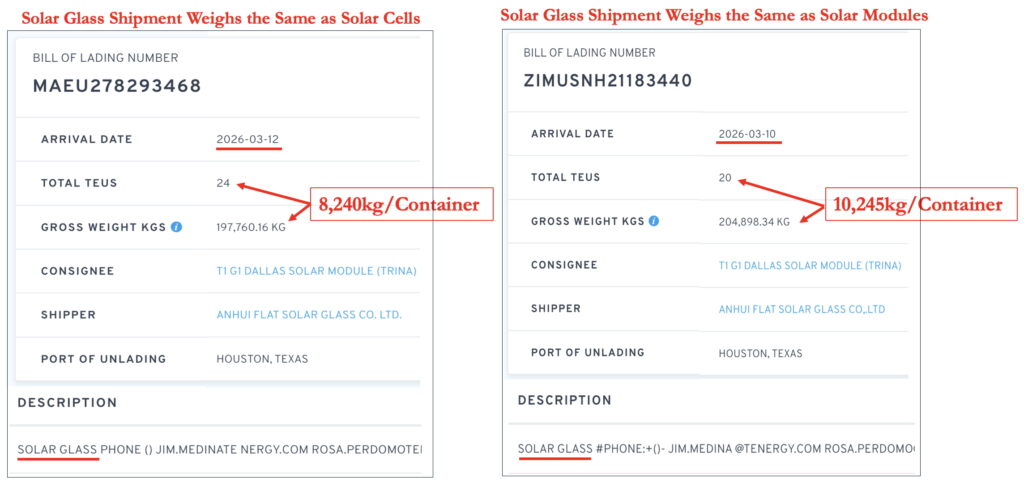

Examples of some suspicious shipments of solar glass that weigh the same as solar cells and solar modules. Notably these shipments have continued in FY 2026.

Are the containers ½ full, ½ empty, or filled with something else entirely?

If T1 Energy’s solar cells are still coming from China in FY 2026 then based on our supply chain components analysis it means No Tax Credits on those solar panels.

Solar Cells are the single most important component in the material assistance formula, and T1 has to import all of its cells. Yet none of T1’s publicly available import-export data show any imports labeled as solar cells. So where is the company getting cells?

First Solar Lawsuit v. Trina & T1 Energy – T1 Continues to Use Trina’s Infringing Cells

First Solar seems to agree with our analysis. In the First Solar 2026 lawsuit against Trina and T1 Energy, First Solar says “T1 Energy continues to manufacture solar modules using infringing solar cells manufactured abroad.”

US International Trade Commission Recently Opened an Investigation into Patent Infringement by Trina, T1 Energy, and Other Chinese Solar Co’s

Following this lawsuit, the US International Trade Commission (ITC) opened an investigation into solar cell patent infringement that names T1 Energy and Trina Solar on March 26, 2026. A negative ruling by the US ITC could lead to the blockage of Trina’s TOPCon cells from entering the US. T1 Energy would be left without the ability to sell their main solar module. Not good for revenue and profitability.

T1’s Current Supply Chain Fails “Material Assistance Cost Ratio” Stipulated by IRS

Like the IP test, we believe T1 also fails the “Material Assistance” requirement for FEOC compliance.

The Material Assistance Test is simple: T1 can only source a limited percent of its material costs from prohibited foreign companies. The percent of material costs coming from foreign entities decreases each year, going from 50% in 2026 to 15% in 2030.

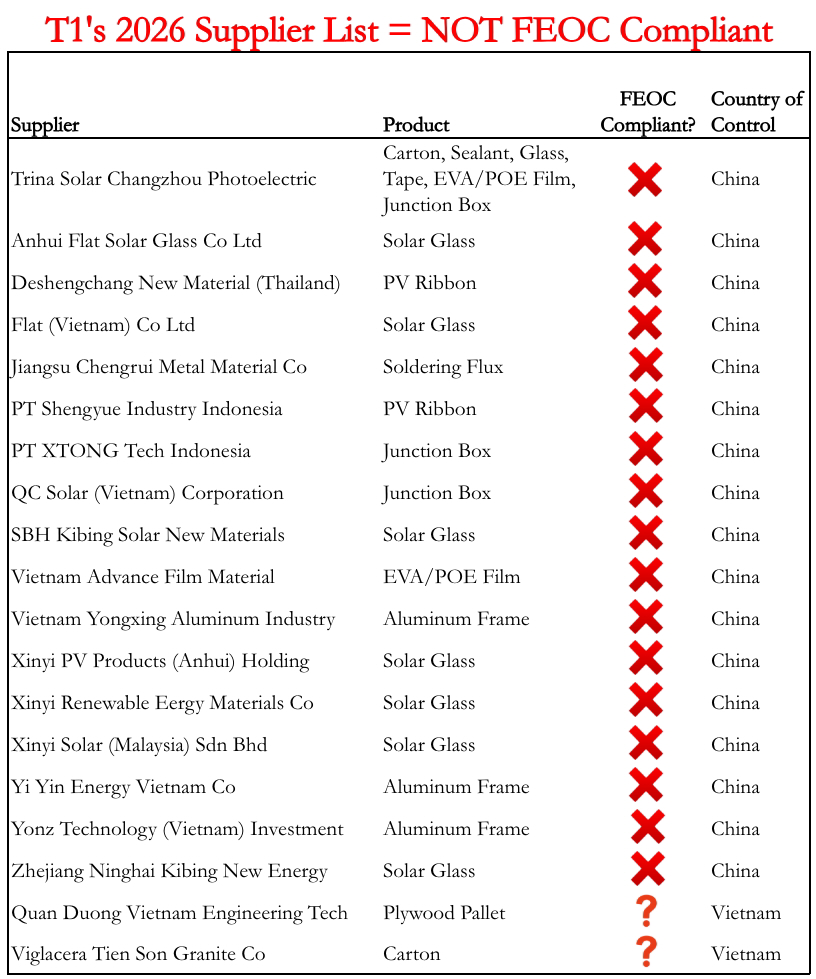

Right now, we think T1 isn’t even close to passing. Almost all its supplies — glass, frames, sealant, ribbons, junction boxes, etc. — come from Chinese-owned factories in Vietnam, Malaysia, and Thailand that the U.S. government does not consider FEOC compliant.

The IRS allows manufacturers to calculate their cost ratio two ways. We analyzed thousands of rows of T1’s own data, and we found the company fails either way you calculate the ratio.

Actual Direct Costs: We mapped T1’s suppliers and the component prices to estimate that 81% of T1’s direct material costs currently come from prohibited foreign companies.

Cost Allocation Percentages: Using the IRS cost allocations table and what we know about which of T1’s suppliers are prohibited foreign companies, we estimate 76% of direct materials costs come from prohibited foreign companies. This assumes 50% of T1’s frames are sourced from Nextpower and 20% of cells are from a FEOC-compliant supplier. T1 said they sourced solar cells from a compliant supplier for a “portion” of their modules – so we think 20% is a generous assumption for a “portion.”

PART 7 – G2 is FEOC’ed Too – Short T1 Energy

G2 Factory is Just as FeoCK’ed

- IP for Solar Cells will be Viewed as Chinese = FEOC

- G2 Plans Originated at Trina Solar < July 2024

- Drone Footage Shows It’s Still a Dirt Patch & is Way Behind Schedule

- Formers Say It’s Years Away From Commercial Ops

- What About Talon PV? Talon’s Connected to Trina Too + Mgmt History Bankrupting O&G Co’s

Former T1 Energy executives told us the G1 factory was built so that it can only take solar cells that match the specs and size of cells that are made by Trina Solar. Thus, G2 Factory will be forced to manufacture cells using Trina Solar’s technology and IP.

“The technology is different enough across the various different solar companies that you can’t just go buy anybody’s cell and turn it into what is the Trina technology module that they want to manufacture” ~Former T1 Energy/Freyr Senior Executive

We believe G2 will never qualify for the extra $0.04 per watt 45X Tax Credits because G2 has the same catch-22 regarding the IP. Either G2 can use old tech (supposedly has been sold to Evervolt) and be uncompetitive or they get access to Trina’s future solar cell intellectual property & know-how updates but not receive tax credits. T1 Energy says G2 will have access to future solar cell updates, so G2 is FeoCK’ed too.

US tax credit guidance is clear, all of the manufacturers of solar cells in the USA that rely on Chinese technology will still be considered FEOC. No tax credits for G2.

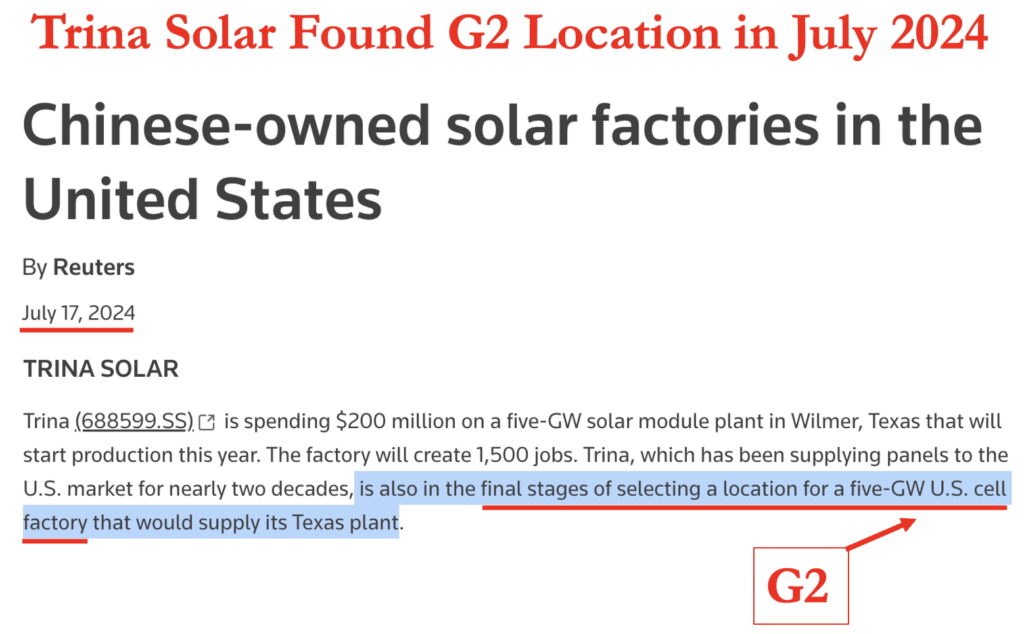

G2 Solar Cell Factory Was Planned by Trina

T1’s boasts that it found its factory site so quickly that it accomplished “in approximately 100 days” what usually “takes about a year.” News reports show this is fiction–Trina Solar was in the final stages of selecting the location to build the G2 factory back in July 2024. The “G2” cell factory was originally a Trina Solar plan.

T1 Solar Cell Factory is Even Designed Off Trina’s Cell Factories

T1’s Q3’25 investor presentation even says their G2 facility design is based on Trina Solar’s Huai’an and Indonesia solar cell factories.

Drone Footage Shows G2 Is Still an Empty Patch of Dirt

T1 has never fully disclosed the location of its G2 solar cell factory site, saying only that it would be in Sandow Lakes in Rockdale, Texas. We found the exact address in an EPA database.

We flew a drone over the planned factory’s site near Austin in Feb, March, and May of 2026. In February all we saw was dirt being moved around, and in the later visits we didn’t find much more. There are some industrial water/chemical storage tanks and temporary buildings for the construction team but the foundation for the 1.3 million square ft factory has not yet even been poured.

From the images it appears that G2 is incredibly far behind the optimistic end of 2026 timeline. We estimate that G2 construction is 12-18 months delayed.

In February 2026 the G2 site was actually quite active with tractors and other heavy equipment flattening out the land. However, in our late march and early May visits we noticed very little new development happening outside of a road to the site being built. Oddly we even saw that some of the porta potty’s seem to have disappeared. That’s a terrible sign for a project, especially since management is still claiming the project will be online by Q4-2026.

Former T1/Freyr Executives also thought the G2 construction was going to be delayed. They thought it would take forever.

“it’s not easy to run a solar module facility, by the way. And by the way, it’s a hell of a lot harder to run a solar cell facility. So don’t just assume they’re going to start Austin up and it’s going to run like clockwork. That startup timing is going to be really interesting to watch because it’s going to take forever.” ~ Former Senior Freyr/T1 Executive

Talon PV’s Trina Solar Agreement Months Before T1 Investment – Operations Don’t Begin Until Q1-2027

Talon PV is meant to be a potential “US based” solar cell supplier. T1 announced an investment in October 2025 multiple months after Talon PV had already entered into an agreement to supply Trina Solar with cells to be used in Trina’s modules.

T1 has claimed that they will be able to get solar cells from Talon in 2026 BUT there is one problem—Talon PV’s own website says commercial operations won’t begin until Q1-2027.

Below is a photo from the Talon PV-Trina Solar agreement announcement in February 2025:

Talon PV’s Mgmt Ran an Oil & Gas Co into Bankruptcy then Founded a Tequila Co & Mexican Stem-Cell Clinic

Most of Talon PV’s management’s expertise in clean energy comes from bankrupting an oil & gas supplier. The Talon team ran “Eagle Pipe LLC” into the ground, literally. Eagle was a distributor of tubular products to the oil and gas industry that declared bankruptcy in late 2020.

The Talon crew’s resume since is even less impressive. It includes co-founding a tequila company you’ve never heard of, a crypto company, and in 2024 they even started a Mexican Stem Cell clinic.

Are investors really supposed to trust that some guys that bankrupted a O&G pipe company and co-founded an unknown tequila company + Mexican stem cell clinic can figure out how to manufacture TOPCon solar cells? You gotta be drinking way more than 1 tequila to believe that.

PART 8 – Is Trina Solar Moving on from T1 Energy? – Short T1 Energy

Trina’s New Side-Piece – Experts Say Trina Hooked Up w/ Other “American” Suppliers; Could this Explain the Large Amount of Trina Bill-And-Hold Trina Rev?

- Did Sketchy, Related-Party Bill-and-Hold Deal with Trina Help T1 Energy Pull Forward $134m of Sales?

- Trina Flirting w/ Other US suppliers, like Imperial Star Solar

- T1 Promises New Customers – Experts Say “Market is Dead”

Is Bill-and-Hold Accounting Being Used to Inflate Revenue? T1 Energy Began Disclosing a Large % of Revenue as Bill-and-Hold in Q4-2025

T1 disclosed that 37% of their Q4 total revenue ($134.4 million) was recognized through bill-and-hold arrangements with Trina Solar. T1 recognized the revenue before shipping products or being paid by Trina.

Bill-and-hold arrangements are an aggressive and controversial accounting ploy that forensic accountants point out have often been used to manipulate earnings.

When Bill-and-hold arrangements are done between related parties (like T1 and Trina) then it is an even larger red flag. T1 has not disclosed to investors the details of the bill-and-hold arrangement nor why their key related party hasn’t been taking full delivery of the module. Oddly, the Q1 10-Q had no mention of the bill-and-hold relationship, despite it accounting for >$130m of revenue in the 10-k.

Infamous bill-and-hold fraud scandals include Sunbeam which was a textbook case of how to use bill-and-hold arrangements to manipulate financials. Diebold was another major improper bill-and-hold fraudulent accounting scheme. Diebold paid a large $25 million FCPA fine and was forced to do a $127 million earnings re-statement.

Solar Industry Experts Said Trina’s Working w/ other US Based Solar Module Manufacturers to Supply Trina Products

We all know T1 needs Trina. But Trina needs T1 way less. T1 management has described 2025 as the year of the marriage to Trina in 1x1s with investors. But we found out that Trina already appears to have secured a side-piece. Experts told us that Trina has begun using Imperial Star to build Trina branded solar modules.

“Most of what Imperial Star is building today is Trina modules … Imperial Star has the capacity and the pricing is better; there’s zero loyalty from any of the brands to a specific factory … Trina already moved on.” ~ Solar Industry Consultant

In Q1-2026 Trina Solar accounted for 99.9% of T1 Energy’s revenue. Losing Trina’s purchases would be disaster for T1. It’d leave T1 Energy with no customers to offtake the hundreds and hundreds of millions of potentially non-FEOC compliant modules that they plan sell.

T1’s 2026 plans call for it to build 3.1GW to 4.2GW of modules, and it says it has contracts to sell 3GW of those. While T1 hasn’t disclosed the buyer, industry experts told us it was obviously Trina. But they added that Trina is not sure bet for T1 anymore – word is out that Trina wants other suppliers, like Imperial Star.

“Trina is already running with bulk orders of modules … through Imperial Star” ~ Solar Industry Consultant

T1 Needs More Customers but Experts say the “Market is Dead”

Solar experts told us all the changes to American rules that are about to FEOC T1 prompted contractors to buy most of what they need through 2027. The experts expect the market to be weak or flatlined until late 2027 or early 2028, at the soonest. That’s bad news for a company like T1 that needs revenue and new customers now, not in 2 years.

“The [solar] market is dead. Like flat out dead” ~ Solar Sales Consultant

PART 9 – Financial Restatement Coming Soon? – Short T1 Energy

Major Financial Restatement Coming? Did T1 Commit Accounting Fraud by Booking Unearned Tax Credits?

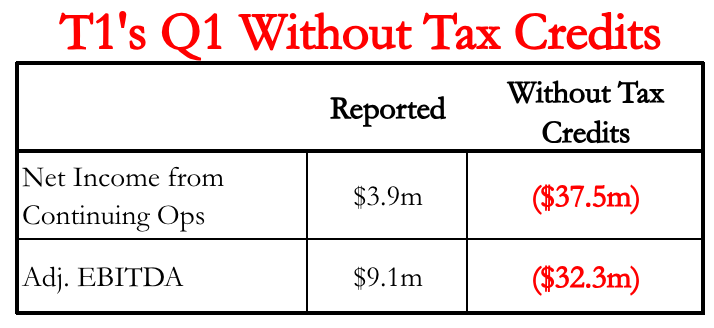

In Q1 2026, T1 Energy booked a significant amount of US tax credits, $41.4 million, on their income statement even though the tax credit rules changed dramatically on January 1, 2026. We believe that booking those tax credits at the very least could lead to a major negative financial restatement later this year, and worst case we believe it could be considered to be accounting fraud.

Per all our work T1 Energy is clearly not FEOC compliant and should not be recognizing 45x tax credits. Booking the tax credits are a non-cash adjustment to the income statement in Q1. The only way that T1 was able to recognize the credits in Q1-2026 is because it was a non-audited quarter and adding the tax credits to the income statement was up to management’s discretion.

T1 Energy’s financial picture looks dramatically worse without the claimed tax credits. Adj EBITDA and Net Income from continuing operations would have been massively NEGATIVE without tax credits.

Naturally, all of these tax credits are non-cash and have not been paid out by the government, so management judgement is required. T1 Energy claiming the tax credits on the income statement that we believe they will not ever actually receive doesn’t actually affect their declining financial position. The cash flow statement tells the true financial picture, T1 Energy burnt $147m in cash in Q1 alone.

Why We Believe T1 Will Be Forced to Restate Earnings Lower?

FY 2026 tax credits are nothing like the ones T1 Energy was able to capture in FY 2025. Trump’s One Big Beautiful Bill Act (OBBBA) changed everything in the solar tax credit landscape, starting Jan 1, 2026. The OBBBA introduced FEOC restrictions on Section 45X tax credits (the essential tax credits for solar module producers).

We have spoken to former US Senior Commerce dept staff, legal counsel for solar tax credit buyers, and multiple former T1 employees and they have told us that they believe that T1 Energy does NOT qualify for US tax credits as of Jan 1, 2026. Thus, T1’s lawyers and accountants should no longer be allowing T1 to incorrectly book non-cash tax credits as offsets to COGS and improve how T1’s income statement looks.

An essential cog in the tax credit sale machine has stopped—the insurance company’s. Our own interview and media articles have reported that the tax credit insurance company’s are either writing policies that carve out FEOC risk separately or are refusing to underwrite policies with any FEOC risk at all.

We believe that T1 Energy’s choice to continue booking tax credits in Q1-2026 was an improper and high-risk choice. One that we believe could even rise to the level of accounting fraud, but that’s up for the SEC to decide. Perhaps this was the reason that T1’s Chief Accounting Officer left abruptly in Feb 2026 (notably there is no standard “no disagreements” language in the 8-k).

The same day of issuing this report we sent a letter to T1 Energy’s Auditor questioning the tax credits.

PART 10 – Gov’t Investigation – Short T1 Energy

T1 Under Investigation by US Gov’t Regulators; Texas State is Calling for an Investigation + Subpoenaed by DOJ & SEC

DOJ, SEC, and State investigations into company’s will occasionally occur after short reports. T1 Energy is the rare exception where the regulators have clearly gotten there first. From our perspective this massively de-risks the short case. We don’t have to convince the government, since it appears they already know the truth.

The Trina-T1 Energy links are so blatant that Texas Lt. Governor Dan Patrick even directly called for the Texas state senate to investigate T1’s financial ties to China.

In the Texas Senate’s committee on business and commerce held its hearing on April 1, Senator Lois Kolkhorst brought up T1 Energy directly with one of the government experts. She asked if T1 was “there was undue influence by Chinese, leadership” and that “[T1’s] subject to the foreign entities of concern” – The expert answered in the affirmative, “Correct.”

DOJ & SEC Subpoenas Sent to T1 Energy

If the subpoenas were actually nothing then why did T1 Energy first drop the news at the bottom of an innocuous 8-K that was primarily about a change to the articles of incorporation and votes registered for a special shareholder meeting. T1 buried the disclosure that they received subpoenas from both the DOJ and SEC and has since tried to play it off as if it’s only related to the CEOs personal trading of the stock.

When was the last time you saw the DOJ care enough to investigate an insider pledging their shares? We’ve can’t recall ever seeing it. Thus we think this indicates a larger deep investigation into if there are other Chinese entities involved in T1’s ownership behind the scenes.

Conclusion – Short T1 Energy

Conclusion – T1’s Stuck in a Catch-22: It Can’t Earn Profits with Trina … or Without It … Either Way T1 is F—’ed

T1 Energy’s will never be able to actually separate themselves from Trina because T1’s is stuck in a catch-22 where its business is completely reliant on Trina. In Q1, Trina was 99.95% of T1 Energy’s sales and the past and future IP T1 relies on is developed by Trina. It’s impossible for T1 to keep telling false stories to investors that they will be FEOC compliant due Evervolt being independent of Trina. Everyone knows that is BS now. T1 Energy’s management can no longer hide from the truth so it’s time for them to answer some questions.

Questions for T1 Energy’s Management:

- Did you know about Tan Chin Piaw and Evervolt’s long-term connections to Trina Solar?

- Did you know about Tan Chin Piaw’s connection to CETC’s HK subsidiary (China Electronics Equipment Group)?

- Now that you know Evervolt and it’s owner are deeply connected to Trina Solar and the Chinese government how can you keep claiming “ T1 Energy is FEOC compliant”?

- Sorry that one was a rhetorical question—we doubt anyone could feel comfortable claiming that.

- If T1 Energy spent $0 on R&D in FY 2025 and Evervolt also lacks the money to spend on R&D, where will future IP improvements and enhances come from?

- Why are the G1 factory’s computers displayed in Chinese in your own youtube videos if you are actually an American company?

- Why do import-export records show container shipments of wood pallets, packing tape, and solar glass all arriving with similar weights to shipments of solar cells?

- Why haven’t you told investors T1 Energy’s solar cells currently come from Trina Solar in Q1-2026?

- Do you plan to use any Trina-built technology in the G2 factory? Who is funding the future IP development for G2’s solar cell factory?

- G2 – Why do our drones show very little progress at the G2 site over the last 3 months?

- How long do you plan to wait until disclosing the project is behind schedule?

- Bill-and-hold in Q1-2026 – Did Trina take delivery of all the bill-and-hold modules from Q4 in Q1-2026? Or did your terms with Trina change? Why is there ZERO disclosure about the bill-and-hold revenue in the 10-Q?

- Will your accountants and lawyers ask you to restate Q1’s income statement and remove the tax credits immediately or do you plan to wait until Q4-2026 to come clean?

- Are T1 Energy’s investors completely FeoCK’ed?

We are short T1 Energy and made up a new spin on an old (Chinese) proverb:

If it looks like a duck, and it quacks like a duck, and the duck speaks Chinese … then it’s a Peking duck. This Peking duck is cooked.

Fuzzy Panda Research is Short T1 Energy (TE)

Appendix D – More Details that FEOC T1 Energy’s Chances at Tax Credits

- T1 Computers & Signs in their own Factory Promo Videos are in Chinese Not English

- IP Agreement Says Trina Pays for T1’s IP Legal Related Fees?

- Trina Solar CEO’s Wife’s Secret Equity Stake in T1

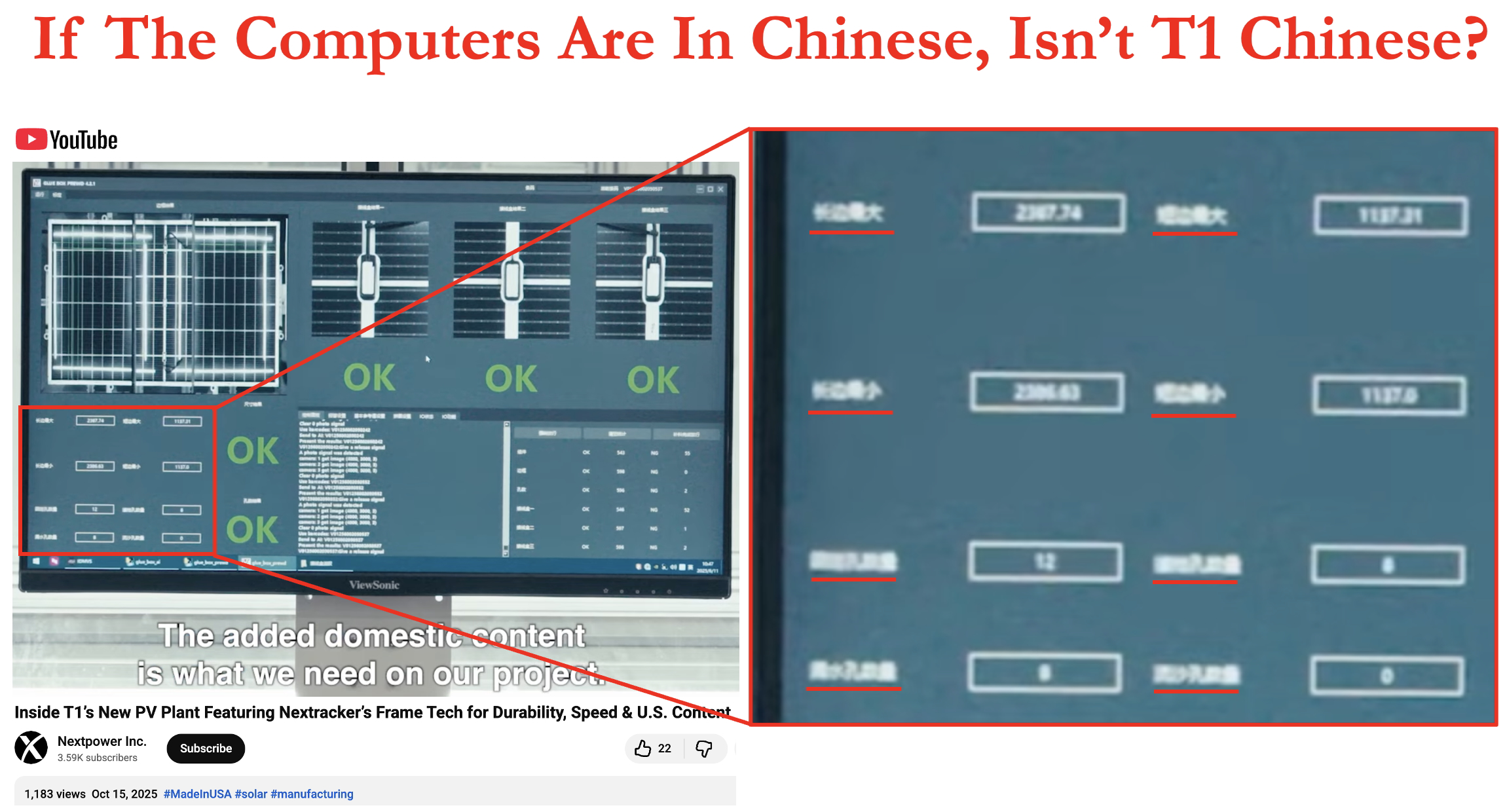

T1’s Marketing Videos Show the Computers Are in Chinese!

All signs point to T1 Energy being labeled Chinese…in fact at the G1 factory those signs are actually written in Chinese. Reporters note that every key notice within the G1 factory is listed in 3 languages Chinese, Spanish, and English. The only other place you can find in Texas with signs in all 3 of those languages is at a PF Chang’s in Laredo.

Just when you thought T1 Energy’s management attention to detail couldn’t get worse.

We found that in T1 Energy’s own YouTube video highlighting the factory that management made a large screw up. They hung a giant American flag on the factory wall but forgot to hide basic details connecting T1 Energy back to China. Notably that T1’s computers are NOT displayed in English … T1’s computers are in Chinese!

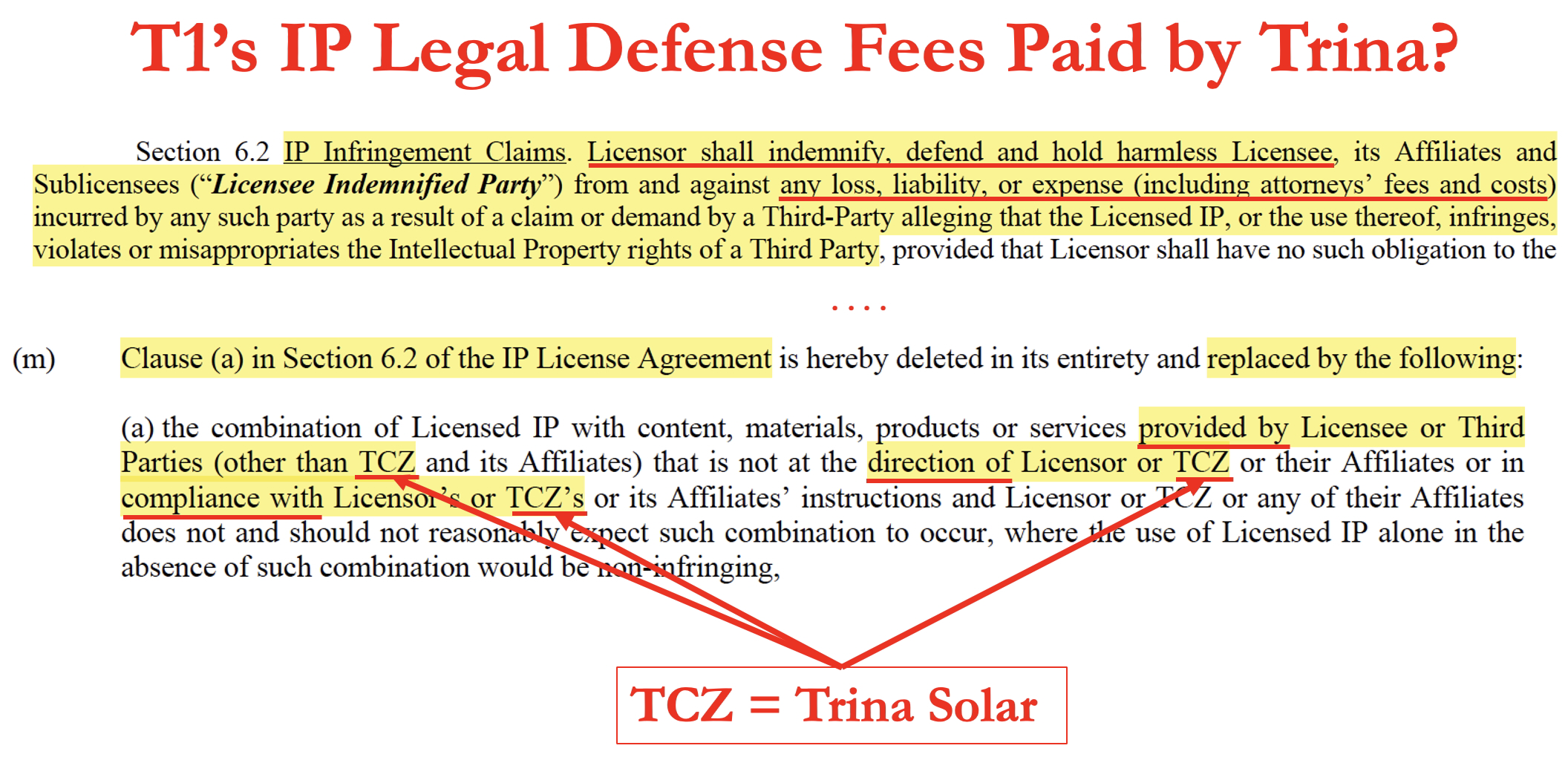

IP License Agreements Reveal a Key Detail – T1’s IP Legal Defense Fees Paid by Trina Solar?

Both the old and the new IP license agreements include a clause where legal fees from IP infringement claims are paid for by Evervolt/Trina solar.

The new IP agreement is modified to specifically add back in “Trina Solar’s” name to the agreement. T1’s expenses will be paid as long as T1 use materials “provided by Trina” “at the direction of Trina” and “in compliance with Trina’s instructions.”

T1 Employs Dozens of (ex)Trina Workers at Dallas Factory

T1 needs the Chinese staff because they know how to run the plant, former executives told us. Most of the Chinese staff directly came from Trina and were hired on at T1 Energy via contracting deals.

“They’re not T1 employees. They’re basically under a consulting arrangement [from Trina]” ~ Former T1 Senior Legal Executive

Caribbean Entities Hid Trina’s CEO’s Wife Owning Shares – Trina Owns At Least 21% of T1’s Equity

We uncovered the wife of Trina Solar’s CEO (Chunyan Wu) owning shares of T1 previously owned 7% of T1’s equity. Her ownership was originally masked under a BVI Entity called Trinaway Investment Second Ltd. In Sept 2025 she exchanged her 7% ownership stake into 7 million $0.01 penny warrants and was compensated with $5 million in cash. She renamed her entity Stellar Hann.

Including Trina (19.7%) and the CEO’s wife (2.6%) Trina controls >22% of equity.

We wonder if the government is going to find other hidden ownership stakes during their investigation? 😉

Appendix E – Elite Solar Connected to Chinese Government Too

Evevolt was fka as Elite Solar who recently constructed a manufacturing facility in Egypt which is a Chinese government backed overseas industrial zone. Elite Solar was previously known as ET Solar which had backing by Yuanfar which is part of the Chinese state-owned aerospace group.

Meantime, Liu Jingqi, (aka Derek Liu) is also connected to the Chinese government through its China-Africa TEDA Investment Co., a joint venture involving TEDA Investment Holdings which is owned by the Chinese government.

Appendix F’ed – How to Follow the FeoCK’ing FEOC Rules

Foreign-entity restrictions relevant to clean-energy tax credits were significantly expanded when OBBBA became law on July 4, 2025, adding the concepts of Prohibited Foreign Entity (PFE) and material assistance from a PFE to credits including 45X, 45Y, and 48E.

The broader FEOC/PFE policy is designed to keep entities tied to covered nations out of sensitive U.S. supply chains and tax credit programs. The legal policy mainly aims at limiting reliance on entities tied to China, Russia, Iran, and North Korea.

An entity can be treated as a FEOC if it is owned by, controlled by, or subject to the jurisdiction or direction of a covered nation, or if it falls within certain specified restricted-entity categories.

Section 45X Advanced Manufacturing Tax Credits are important for T1 Energy as the economics for a solar manufacturer can flip from negative to positive based solely on receiving these credits. In order for T1 Energy to qualify for 45X credits after OBBBA, it must satisfy the applicable Treasury/IRS PFE and material-assistance rules.

The 45X tax credits for solar module manufacturers run until 2032 but get reduced each year beginning in 2030. For solar modules, the 45X credit phases down based on the year the eligible component is sold: 75% in 2030, 50% in 2031, 25% in 2032, and zero thereafter. So for T1’s business, it’s very important to be eligible for these tax credits NOW.

For a U.S. solar manufacturer claiming 45X, the key tax issues are whether the company is treated as a foreign-influenced entity or other PFE, whether any specified foreign entity has disqualifying equity, debt, or covered officer-appointment rights, whether contracts or licenses create effective control, and whether the eligible components include material assistance from a PFE.

T1 Energy made changes in 2025 to address these restrictions, but the February 2026 IRS notice introduced a more detailed interim framework for PFE status, effective control, and material-assistance analysis, so those changes still need to be tested against that framework.

T1’s Efforts of Becoming FEOC Compliant:

Covered Officer: T1 Energy demoted Trina Solar employee, Mingxing Lin, from Director and Chief Strategy Officer to consultant to try and become compliant with the “covered person” provision. But he continues to appear as a Director on T1’s website.

Equity & Debt Ownership: T1 raised capital (1,2) to buy down debt owed to Trina Solar to meet the “equity and debt” ownership rules.

Effective Control: T1 said they don’t believe any of its agreements give a FEOC effective control of the company. The interim definition of effective control for a FEOC/PFE is when the FEOC/PFE has “the unrestricted contractual right of a contractual counterparty to do certain things that let it control a taxpayer’s facility, equipment, output, or production decisions.” This includes:

- Determine the quantity or timing of production of an eligible component

- Determine the amount or timing of electricity-generation or storage activities

- Determine who may purchase or use the output of an eligible-component production unit

- Determine who may purchase or use the output of a qualified facility

- Restrict access to critical production data or to the facility

- Have the exclusive right to maintain, repair, or operate plant or equipment necessary to produce eligible components or electricity

We do not believe the Module Operational Support Agreement and the Sales Agency Agreement clearly trigger the effective control provision as they have been amended to avoid tripping the IRS’s guidance. However, the latest IRS guidance released in February 2026 says that for IP licensing agreements, effective control also includes any one of the additional rights, including when a counterparty can:

- Direct the source of components, subcomponents, or critical minerals

- Direct the operation of the facility or production unit

- Limit the taxpayers use of IP

- Receive royalties beyond year 10

- Require the taxpayer to enter a services agreement longer than 2 years

- Withhold the full technical data needed for the licensee to operate independently

- Or where the IP contract was entered into or modified on or after July 4, 2025

It’s important to note that if any one of the listed items are met, the specified foreign entity is treated as exercising effective control over T1 Energy. So we believe T1 Energy fails to meet the effective control provision because of Trina’s non-bona fide sale of IP to Evervolt and the date the amended IP agreement was entered into.

It’s important to note that if any one of the listed items are met, the specified foreign entity is treated as exercising effective control over T1 Energy. So we believe T1 Energy fails to meet the effective control provision because Trina’s sale of the IP to Evervolt was NOT a bona fide sale, the limited geographical use of the IP to only be in the United States and the date the amended IP agreement was entered into.

Intellectual Property: Conveniently, three days before the new year, T1 said that Trina sold its patents and IP to Evervolt Green Energy Holding Pte Ltd. Our research can’t confirm that any actual sale went through. This is related to the effective control provision stated above.

Material Assistance: Additionally, T1 said they purchased solar cells from a non-FEOC supplier to use in a portion of its solar modules for 2026 but didn’t disclose who the supplier was. However, purchasing non-FEOC cells are hard to obtain. The US only has 4-5 GW of cell production capacity but 50 GW of module capacity, so finding a US supplier with excess capacity will be difficult for T1 Energy. And after analyzing thousands of shipments from T1’s import records, we find no evidence of T1 receiving solar cells from any non-Trina supplier abroad. Since the solar cell is the largest driver of direct material costs for a solar cell, we believe T1 is not compliant with the material assistance provision.

Since the main cost driver for material assistance is the solar cell, we provided you a free analysis:

T1 has publicly stated they expect 90% of module production to be utility-scale modules. According to the company, it currently produces the following Trina modules:

- Trina TSM-NEG19RC.20

- Utility-scale projects

- TOPCon technology using 132 cells with 210mm wafer/cell platform

- Trina TSM-DEG21C.20

- Utility-scale projects

- PERC technology using 132 cells with 210mm wafer/cell platform

- Trina TSM-NE09RC.05

- C&I and residential projects

- TOPCon technology using 144 cells likely with 182mm wafer/cell platform

On T1’s Q2’25 earnings call, T1 said they had 2/7 lines producing PERC modules. So future production will be heavily TOPCon weighted.

In 2026, Mission Solar will have 2GW’s of solar cell capacity but this capacity will be used internally for their own products. Qcells, Talon PV, and T1 Energy’s cell facilities are all expected to come online near the end of the year or early 2027.

T1 says they’re purchasing solar cells from international suppliers that are non-FEOC yet their import records show no evidence of this. So the key question bulls should be asking T1 Energy regarding their “material assistance” FEOC requirement is: “Show us the proof!”

Appendix More F’ed – T1’s Supply Chain Shows a Sea Full of Chinese Connected Entities

We analyzed each of T1’s 2026 suppliers and found that while most are based in China, Vietnam and Thailand, but these suppliers actually all appear to be Chinese controlled/connected entities. These Vietnamese and Thai companies are considered “prohibited foreign entities” because their parent companies are Chinese.

This means that T1’s supplies from such companies would be counted as non-domestic for the IRS’s Material Assistance Cost Ratio. Therefore, making it harder for T1 to pass the material assistance FEOC provision and make T1 ineligible for 45X tax credits.

Appendix G – How Solar Tax Credits Are Paid Out

T1 says their COGS “are offset by our generation of 45X tax credits” meaning each quarter, including Q1’26, the gross margin reported includes tax credits. The government doesn’t physically pay T1 cash each quarter for the tax credits the company recognizes on its income statement and balance sheet. These quarterly adjustments are non-cash and are largely based on the management team’s estimates of what they have earned.

Tax credit lawyers and commerce department officials explained to us how the tax credits payout process actually works. Each year, after filing taxes, the IRS will physically mail a check to the company claiming the tax credits if the company is FEOC compliant and earned those tax credits appropriately. Until that check arrives in the mail there is no guaranteed certainty that the tax credits you claimed in the prior year will actually arrive.

Given the uncertainty of timing and guaranteed amount of payouts most solar company’s monetize these credits ahead of time by selling them at a discount to a tax credit buyer. The tax credit buyer will do their own due diligence on the company (i.e. on T1 Energy) and if they feel confident that the seller (i.e. T1 Energy) will earn tax credits and is FEOC compliant, they may purchase the tax credits for ~$0.90-$0.95 on the dollar. Then when taxes are filed, the IRS will mail a check to the new owner of the tax credits for the full amount.

There is another layer to this industry and that’s the insurance companies. Tax credit buyers and their LP’s want to be assured that they will earn their expected rate of return. Thus they purchase tax credit insurance which guarantees the buyer gets the actual payout even if the credits they purchased later turn out to be ineligible.

But there is 1 big problem for T1 Energy & their management team’s decision. Every lawyer and tax credit insurer we have spoken to have told us the market is completely closed. The insurers are no longer willing to underwrite the transactions and when they do they write special carve-outs to exclude FEOC risk. Given the large amount of FEOC risk at T1 Energy it appears to us that it is completely inappropriate for them to recognize earning these tax credit payouts on their quarterly income statement.

Appendix H – Import-Export Data Doesn’t Lie; How Analyzing Container Weights can Reveal their True Contents? Solar Cells?

We used multiple import-export databases and analyzed thousands of shipments and rows of data. In that data lies the truth. Companies rarely ship containers that are even partially empty. Even in an industry as shady as solar which has pulled every trick in the book (including mislabeling BOLs) to try dodge tariffs the import-export data offers key insights. There are 2 things a shipping company absolutely can NOT lie about. The weight of the container (a large part of price is based on weight + that’s essential info for port cranes & ships) + the size & number of the container. Even an extreme skeptic will readily admit that the reported number of containers and their weight is honest, even on shipments with potentially mislabeled cargo.

We recommend you analyze T1 Energy’s Import-Export data, too. You will find many strange anomalies, but primarily you will find a whole lot of container shipments that just so happen to be a similar weight to Solar cells…but then oddly carry BOLs that state that container contents are filled with “wood pallets,” “packing tape,” and “solar glass” but yet somehow all of these weigh approximately the same as what a container of “solar cells” also do.

Below are a collection of non-Trina associated import-export shipments which could help you in figuring out what a standard container weight of a shipment of solar cells is, or how much solar glass or solar modules should weigh per container (defined as TEU – Twenty Foot Equivalent Unit).

Note – The below shipments are example shipments chosen from other company’s import/export of solar cells, solar glass and solar modules. These are from competitors and are not from T1’s own import recordds since we wanted to figure out if T1’s freight matched the weight.

Fuzzy Panda Research Disclosures, Disclaimer and Terms of Service:

By downloading from or viewing material on this website and/or by reading this report, you agree to the following Terms of Service. You agree that any use of the research in this report or on this website is at your own risk. In no event will you hold Fuzzy Panda or any affiliated party, including officers, directors, employees, consultants, and agents of Fuzzy Panda or any companies affiliated with any of them, liable for any direct or indirect losses caused by your use of or reliance on information on this site or in this report. You further agree that you will not rely on any information in this report or on this website, to do your own research and due diligence before making any investment decision with respect to companies or securities mentioned herein, and that you will consult with your own investment professionals prior to any investment decisions. You represent that you have sufficient investment sophistication to critically assess the information, analysis and opinions in this report or on this site. You further agree that you will not communicate the contents this report or other materials on this site to any other person unless that person has agreed to be bound by these same Terms of Service. If you accessed, download, or receive this report or the contents of other materials on this site as an agent for any other person, you are binding your principal to these same Terms of Service.

As of the publication date of this report, Fuzzy Panda, and possibly any companies affiliated with it or its members, partners, employees, consultants, clients and/or investors (the “Fuzzy Panda Affiliates”), have a short position in the stock (and/or options, swaps, and other derivatives related to the stock) and bonds of the company covered in this report (the “Covered Company”). Fuzzy Panda and the Fuzzy Panda Affiliates therefore stand to realize significant gains in the event that the prices of either equity or debt securities of the Covered Company declines. There are many factors that can go into a decision to cover the short position(s) in the Covered Company’s securities and it is not possible to predict exactly when or for exactly what reasons Fuzzy Panda and the Fuzzy Panda Affiliates may cover their positions, in whole or part, or otherwise change their investment holdings. As a general matter, Fuzzy Panda and the Fuzzy Panda Affiliates intend to cover some or all of their positions at a time that the price of the Covered Company’s securities are lower than when they were sold short or otherwise invested in. Fuzzy Panda and the Fuzzy Panda Affiliates may cover some or all of their short positions immediately after the publication of this report or an indefinite period after its publication. Similarly, Fuzzy Panda and the Fuzzy Panda Affiliates may cover some or all of their short positions if the price of the Covered Company’s securities move a small amount or after moving a larger amount. Fuzzy Panda and the Fuzzy Panda Affiliates intend to continue transactions in the Covered Company’s securities for an indefinite period after the publication of this report, and they may be short, neutral, or long at any time after the publication of this report regardless of any opinions, possible stock prices or valuations, or other views stated in the report. Fuzzy Panda will not update any report or information on this website to reflect any changes in the investments of Fuzzy Panda or the Fuzzy Panda Affiliates that existed at the time of the publication of this report, or any new positions in any securities of the Covered Company.

This report and the Fuzzy Panda website is informational and describes the opinions of Fuzzy Panda. This report is not an offer to sell or a solicitation of an offer to buy any security, and Fuzzy Panda does not offer, sell or buy any security to or from any person through this report or the Fuzzy Panda website. This report is not a recommendation or advice to short or otherwise invest in or trade any security. Fuzzy Panda does not render investment advice to anyone unless it has an investment adviser-client relationship with that person evidenced by a formal written agreement. You understand and agree that Fuzzy Panda does not have any investment advisory relationship with you, or owe any fiduciary or other duties to you. Giving investment advice requires knowledge of your financial situation, investment objectives, and risk tolerance, and Fuzzy Panda has no such knowledge or information about you.