- Pivot to Fermi 2.0 is a Mirage

- C-Suite Filled with “Yes Men” who Schemed with Former CEO & allegedly Involved with “Fraudulent Transfers”

- CFO Promoted to Board Friday, Resigned as CFO this AM

- Company Added Bankruptcy Expert to Board

- Former CEO Toby’s Past – More accusations of “Fraudulent Transfers” & “Securities Fraud”

- Key Partners appear to be Undisclosed Related Party Transactions

- No Hyperscaler Deal & None is Coming Because:

- Fermi Couldn’t get $5 Billion+ in Financing

- Lacks Concrete Plan & Lacks Capital

- Drone Footage Show a Mostly Empty Dirt Patch

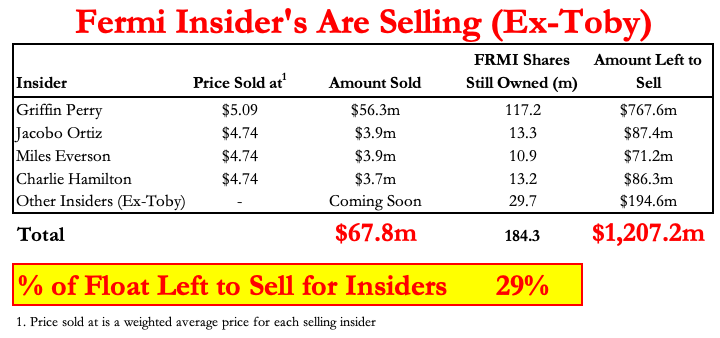

- Insider Selling Just Began

- 94% of Float Recently Unlocked & Borrow Finally Freed Up

- Insiders already Dumped $65m & have $2.5 billion More They can Finally Sell

“These guys [Fermi America] aren’t even close to Enron. I knew the Enron guys. At least they knew what a megawatt hour was”

~ AI Data Center Expert

You know Fermi is doomed when an industry expert compares them to Enron, but mainly to point out that the guys running Enron were way smarter – and they didn’t even know about the fraud allegations against senior management.

We are short Fermi America (FRMI). After the market closed Friday, Fermi CEO and co-founder Toby Neugebauer surprisingly “departed” the company. We believe he was fired, and that puts Fermi in an even worse position. Those left to run the shop are Toby’s loyalists (aka FoT’s – Friends of Toby). We uncovered serious allegations of fraudulent transfers and misappropriation of assets against both Toby and his leftovers in the C-suite at Fermi.

Our research will shed light for everyone onto all the reasons:

- Why the founder & CEO suddenly

was fireddeparted - Why the hyperscaler tenant bailed

- Why Project Matador’s capex and broken plans will slaughter Fermi bulls

Given that founding CEO Toby Neugebauer has just “departed,” we moved most of the information about Toby’s alleged fraud, insider enrichment schemes, and his reported character flaws like day-drinking and drug use at work to an Appendix…Appendix AA.

A bet on a company that plans to build a massive AI data center and enough power generation to light up 2.5x New York Cities is a wager on truly excellent management and executive. These guys are like the Bad News Bears of insider enrichment. We believe that Fermi is an even better risk adjusted short today at $5 than it was at $15 or even at $25 because of who is running the show.

Fermi C-Suite – Toby’s Friends with alleged Fraudulent Transfer Benefits + Other Loyalists:

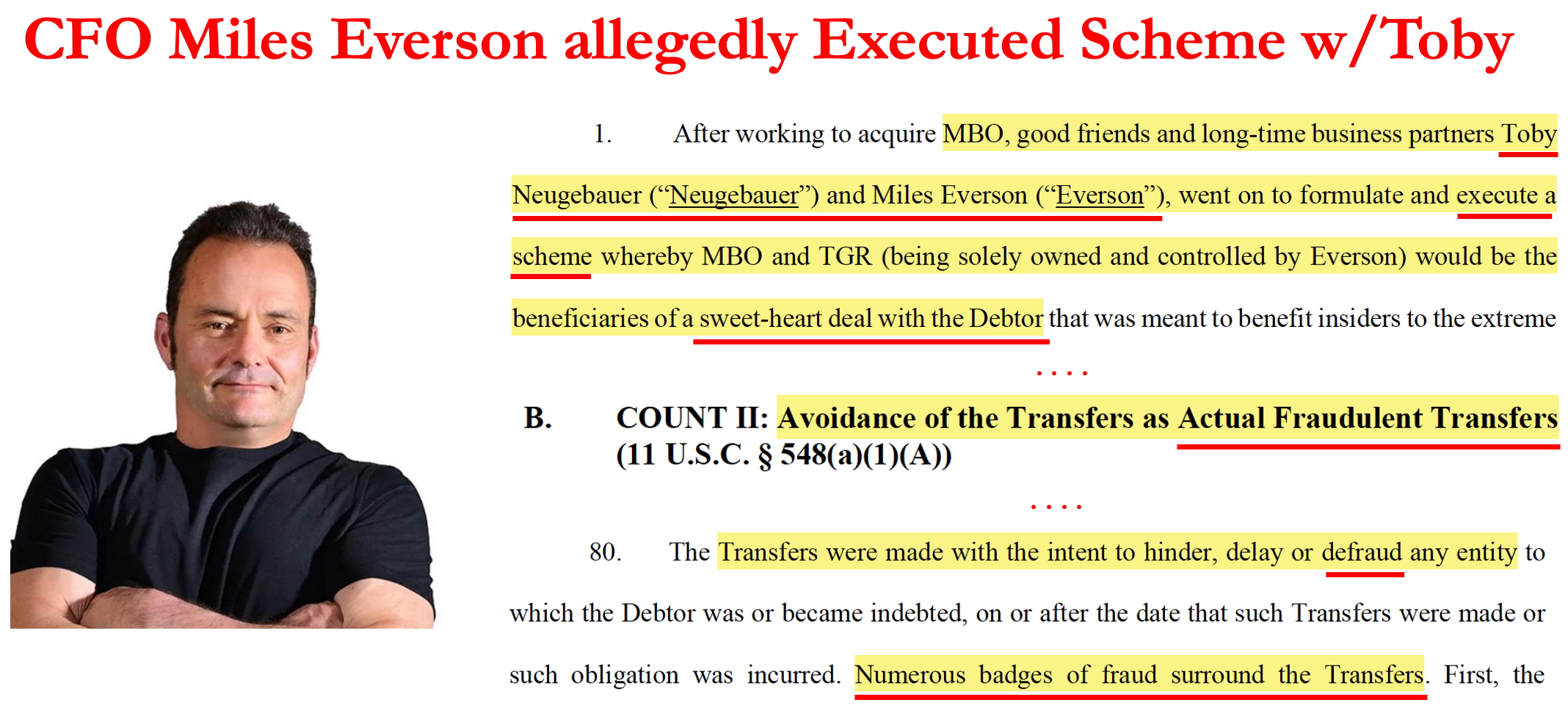

- CFO Miles Everson:

- Allegedly schemed with Toby to skim $8.7 million by billing for phantom services.

- Toby promoted Miles & named him to join the board of directors.

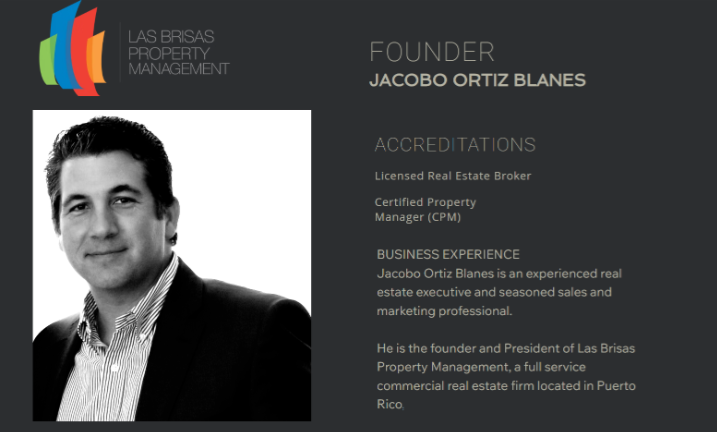

- New Interim CEO Jacobo Ortiz:

- Another FoT – Jacobo and Toby are neighbors in a Puerto Rican golf & beach resort.

- No data center or power plant experience — ran a Puerto Rico Real Estate Firm.

- Chief Site Officer Charlie Hamilton:

- allegedly Toby’s “Yes Man”

- Charlie approved and benefited from alleged “fraudulent backdating securities” with Toby.

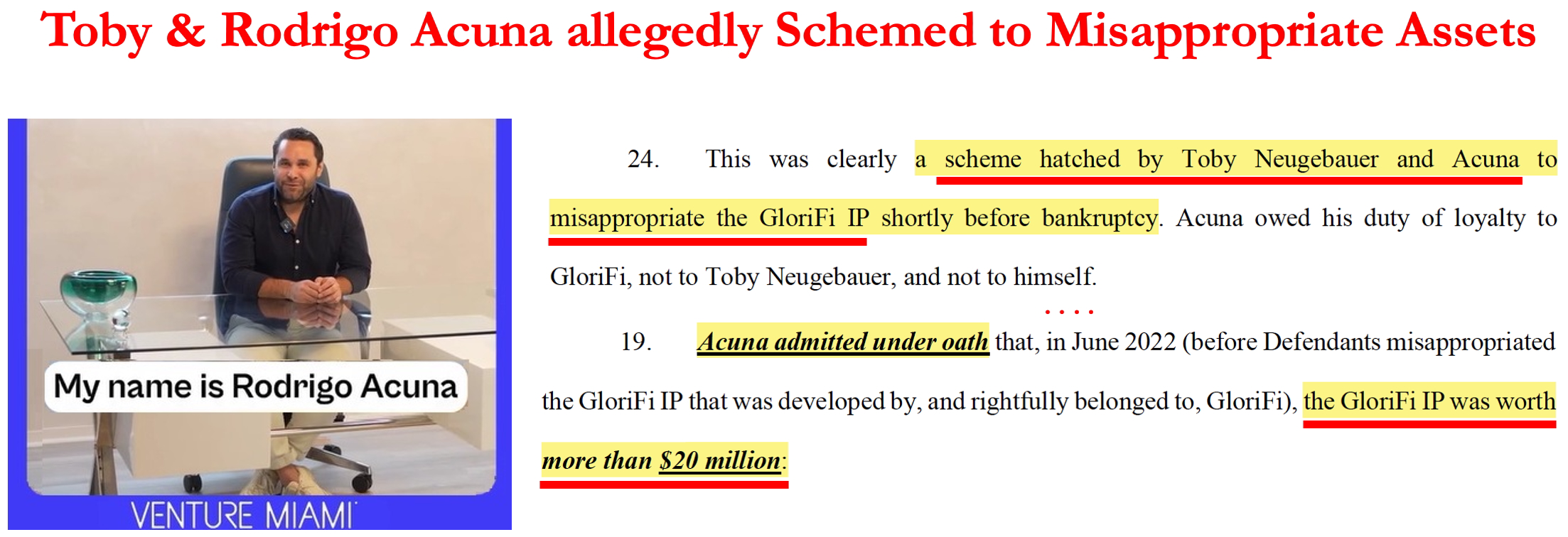

- Director of IR – Rodrigo Acuna:

- accused of executing a scheme with Toby to Misappropriate Assets worth >$20 million

- General Counsel – George Wentz:

- Not a Friend of Toby’s but ‘George the GC’ managed to get himself accused of a different fraudulent transfer scheme all by himself.

- Multiple of Toby’s family members are key employees

- Other C-Suite Members and senior management are friends from Toby’s Past.

Fermi’s inexperienced management team and their past fraud allegations are not even the worst things we uncovered in our 6 months of due diligence into Fermi.

- Key Contractors appear to be Undisclosed Related Parties

- Parkhill was hired as the key engineering firm designing Project Matador.

- One of Parkhill’s Owners is John Hamilton. John is 1st cousins with Fermi’s Chief Site Officer, Charlie Hamilton.

- John & Charlie also run a company together called “Four Hamiltons LLC”

- None of this is disclosed

- Natural Gas Supplier = Another Undisclosed Related Party?

- Energy Transfer, Fermi’s Nat Gas Supplier, discloses Fermi as a related party. Fermi is a tiny part of Energy Transfer’s business.

- Yet Fermi does NOT disclose Energy Transfer as a related party. Energy Transfer is Fermi’s key supplier for nat gas.

- Our Drone Flyovers show Fermi’s project is still empty dirt fields

- Experts say Fermi Lacks Complete Engineering Plans

- Fermi’s Plan is piecemeal and missing key parts and the plan has major electrical problems

- Large Red flag = No well-known EPC contractor like Bechtel or Flour took job

- Why did Hyperscaler Tenant 1 (Amazon) walk?

- We believe it is because Fermi promised they could secure $5-5.5 billion of financing

- Toby tipped everyone off – He told Amarillo City Council he needed to get the financing by December 9, 2025

- December 9, 2025 was also the last date of exclusivity with Tenant 1. Huge coincidence?

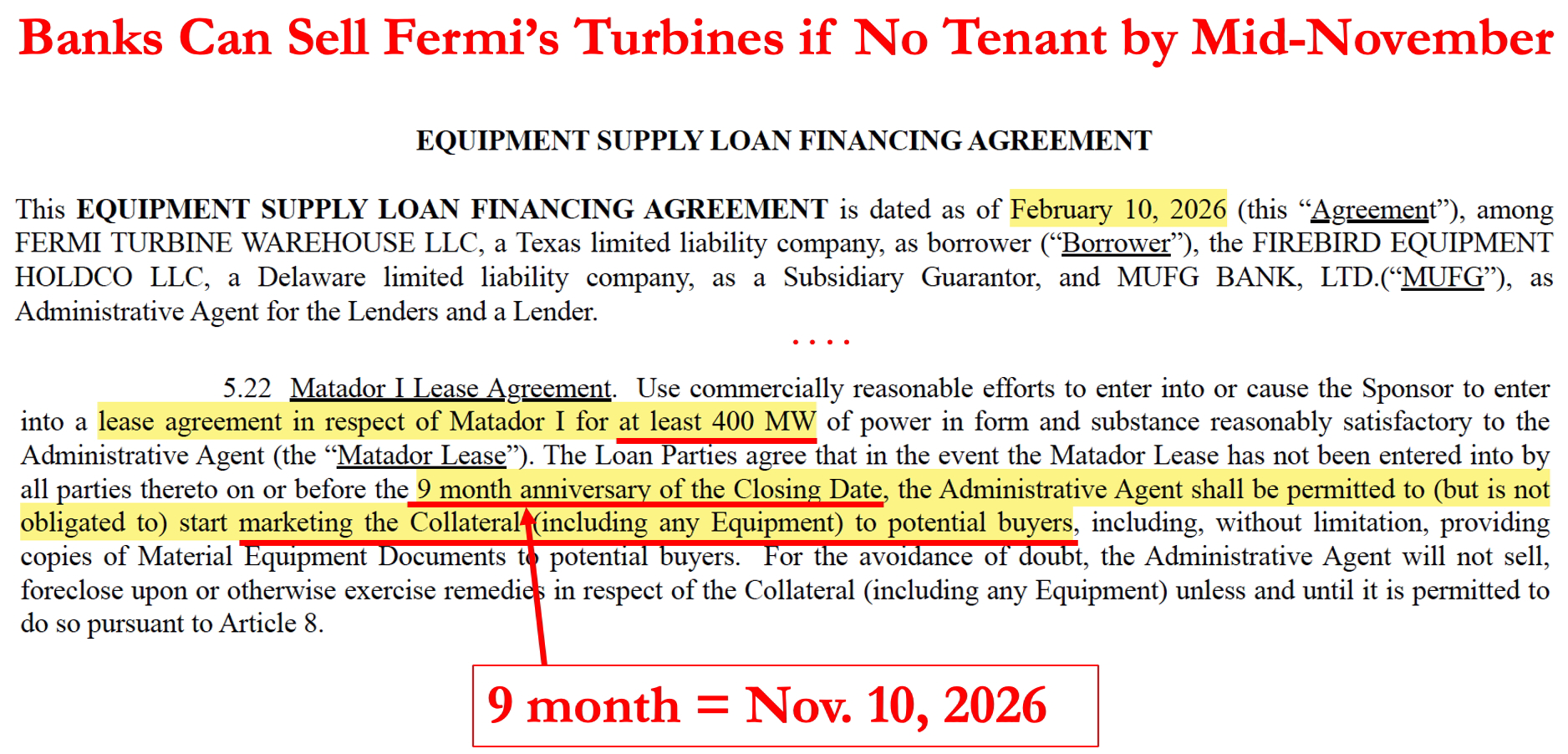

- Fermi’s Turbines are at Risk – Could be Sold in 7 Months

- Bull thesis depends on Fermi’s access to turbines.

- Debt Holders can sell the turbines if Fermi doesn’t have a 400MW AI hyperscaler tenant by Mid-Nov.

- New lawsuit also threatens to unwind the Siemens turbine sale – More accusations of fraud

- FOIAs show Land Lease Can be Terminated by End of 2026 if No Tenant

- Texas Tech can cancel the lease if a 200MW tenant isn’t signed by 12-31-2026

- Only Financing that has happened is Expensive Debt Financing

- Debt is secured by hard assets and at low LTVs (55% to 65%).

- Some has high interest rates >12%

- Death Spiral Toxic Financing:

- Fermi has been forced to raise via “death spiral” toxic financing from Yorkville

- Construction Halted in February 2026 because Fermi is running low on cash

- w/out the death spiral equity raise and if construction had continued on plan then at the end of Q1 Fermi’s Est Cash Balance would’ve been NEGATIVE

- At least $2 billion more of Capex needed to complete Phase 1

- Long term plans require $70-90 Bn of capex…that’s lots of death spiral financing

- Only 35 employees – Market Cap per Employee of ~$120 million each

- Insider selling of 94% of the float began March 30th

- Insiders already Sold >$65 million. They have >$2.4 billion they need to dump.

- Former CEO that just departed said he intends to sell too.

- Borrow is finally available: ~120 million of investor shares could also be sold post lock-up.

Fermi is a not a field of AI dreams … it’s a field of dirt. Sure, if they built it a tenant would come. But they lack the capital needed to build it, the expertise to build it – and now they’ve had to even stopped building it. Fermi has a Catch-22 that no AI hyperscaler wants to be stuck in.

It’s so obvious that even Jim Cramer can see the writing on the wall. Cramer has called Fermi “a loser” and as painful as it is, we admit that we agree with Jim. We are Short Fermi America (FRMI).

Fuzzy Panda Research is Short Fermi (FRMI)

Fuzzy Panda Research and Fuzzy Panda “Affiliates” are short securities of Fermi America (FRMI). Please see additional disclosures at the end of report and in our terms of service.

Prequel – Short Fermi – Toby’s Departure – Was it the Fraud, the Drinking, or the Yelling?

Toby’s Alleged Fraudulent Transfers; Securities Fraud; Drinking & Drug Use

- Toby + Key Fermi C-Suite accused of Fraudulent Schemes — Millions of Fraudulent Transfers, Securities Fraud, and Insider Enrichment

- Toby’s Other Alleged Bad Behavior:

- Drank “alcohol” throughout the day? YES

- Threatened to kill an investor? YES

- Used drugs “white powder” at work? YES

It is definitely time to short a company when the CEO with a history of fraud allegations and drinking and drug use on the job is let go in a Friday evening 8-k. But instead of cleaning house, the Fermi board left Toby’s loyalists to run the place.

We believe it’s fairly obvious that Toby was fired. The brief statement from Fermi says he “departed” – not resigned. The only way we think it should be described as “departed” is if the Fermi board was referencing the movie “The Departed”…spoiler alert, everyone dies. The 8-k was also missing the standard language about “no disagreements” when executives leave. On his way out, Toby put his long-time buddy Miles Everson, the CFO, on the board. Toby’s neighbor in Puerto Rico, Jacobo Ortiz, got promoted to the interim CEO.

It’s unclear which of the many reasons were the one that pushed the board to put Toby out to pasture, but here are some of the fraud filled allegations against Toby & the FoTs (Friends of Toby) that we have uncovered.

Toby’s + Key Fermi Mgmt’s alleged “Fraudulent Transfers”

At Toby’s past billion-dollar bankruptcy, GloriFi, we uncovered the bankruptcy trustee accused Toby and multiple key members of Fermi’s remaining management team of executing “fraudulent transfers” that enriched themselves. Toby’s dream team was accused of committing securities fraud including altering and backdating debt documents (with Fermi CSO, Charlie Hamilton), insider enrichment, misappropriating >$20 million of intellectual property (with Fermi Director, Ricardo Acuna) and even allegedly a “sweet-heart deal” with a friend to skim millions (with Fermi CFO, Miles Everson).

According to the bankruptcy trustee:

The Bankruptcy Court ruled that millions of Toby’s deals were fraudulent transfers.

But to read about all of Toby’s shenanigans please see Appendix AA.

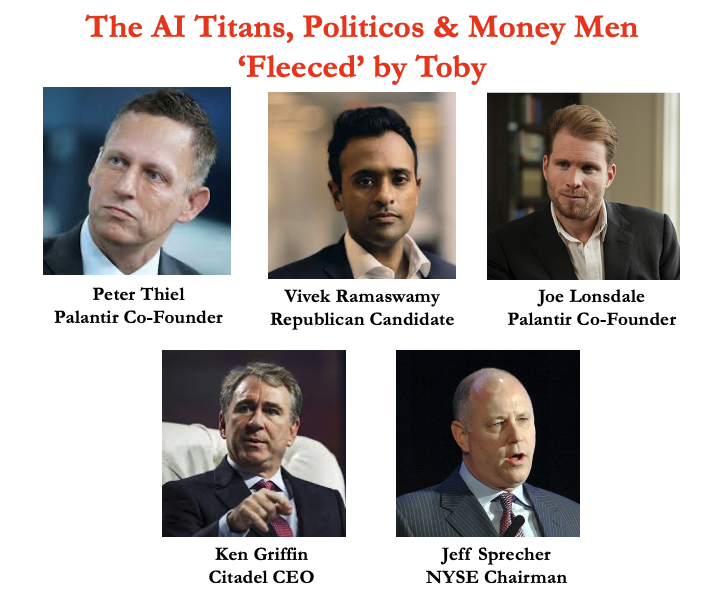

Toby Fleeced Silicon Valley AI Legends & Top NY Financiers

If you’re trying to sign up an AI hyperscaler, you probably shouldn’t make enemies of Silicon Valley’s AI elite, DC heavyweights and New York’s top financiers. That is exactly what Toby did at his past company. The trustee stated that Toby “fleeced” investors, including:

- Palantir co-founders Peter Thiel and Joe Lonsdale

- Former Presidential Candidate – Vivek Ramaswamy

- New York Financiers – Ken Griffin (Citadel) and NYSE Chairman Jeff Sprecher

Toby’s Other Talents? Drank on the Job, Used White Powder at Work & Threatened to Kill an Investor

Bankruptcy dockets show that Toby managed to accomplish an “employee of the year” trifecta that not many people have done. Multiple employees said Toby would:

- Day-drink during work – Toby called it “microdosing alcohol”

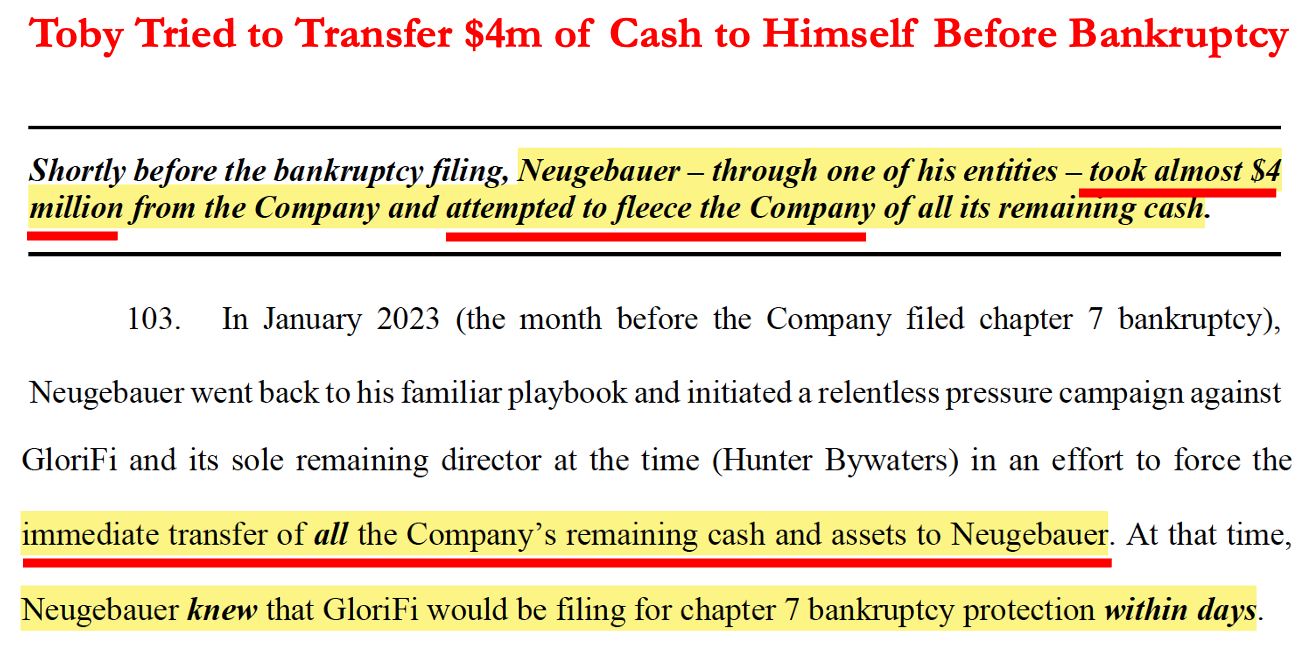

- Used “white powder” at work

- Threatened to Kill Vivek Ramaswamy

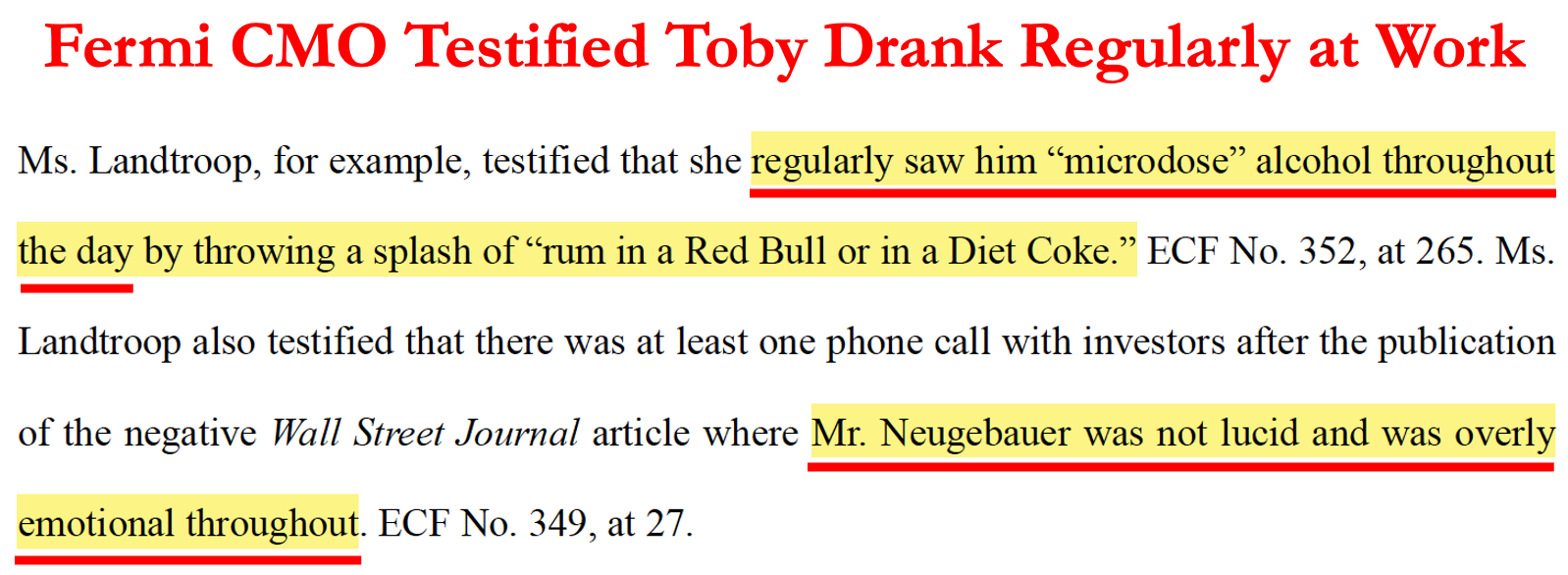

Former employees and board members testified that Toby would often drink throughout the workday. The current Fermi CMO, Cathy Landtroop, testified that she regularly saw Toby “throwing a splash of rum in a Red Bull or in a Diet Coke.” A former GloriFi board member testified that Toby’s drinking started at 10am.

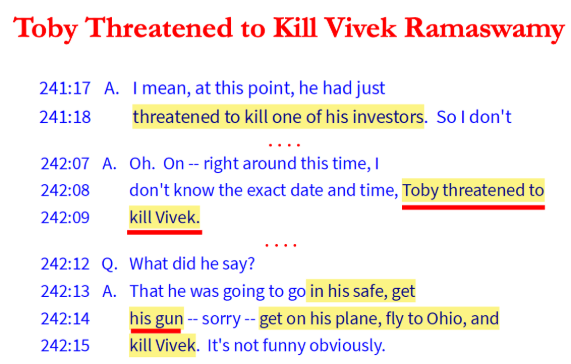

Investor Relations Lessons from Toby – “I’m Going to Go to My Safe, Get My Gun, Get on My Plane…and Kill Vivek”

Maybe Toby’s Last Straw was Yelling at the US Commerce Secretary

A CEO former CEO with a hyperscaler deal on the horizon doesn’t yell at the US Commerce Secretary in public.

At the Nvidia Conference in late March 2026 Toby shouted at US Commerce Secretary, Howard Lutnick. accusing him of blocking South Korean investment that Fermi needs for its nuclear power plant. We spoke with 2 members of the commerce department who told us more about the situation and that Lutnick responded, “there is no deal to be done.”

“He was basically shouting ‘Why are you holding up my deal?’ And Howard sort of responded by saying, ‘I’m not really sure, given that there’s no deal to be done.’”

~ senior Commerce Department Official A

Politico reported that Toby at one point had to be restrained by Lutnick’s security detail

PART I – Short Fermi America – The FoT’s – allegations of Fraud against FRMI Mgmt

Key FRMI Mgmt are Toby’s Friends sometimes w/ Fraudulent Transfer Benefits

- CFO – Miles Everson – allegedly Skimmed >$8 Million via Related Party

- Director – Rodrigo Acuna – allegedly Schemed with Toby to “Misappropriate” Assets Worth >$20m

- Chief Site Officer – Charlie Hamilton – Toby’s ‘Yes Man’ Approved “Fraudulent Backdated Securities”

- New CEO – Jacobo Ortiz – Toby’s Golf Club Neighbor that’s a Puerto Rican Property Developer

- Other Toby Friends & Family are Key Employees

All truly suspect companies like Nikola and Lordstown Motors share a key feature. They like to put their friends and family from previous suspect ventures in management roles. The newly departed CEO at Fermi, Toby Neugebeur was no different. Toby stacked the Fermi management team with key lieutenants from Toby’s last billion $ bankruptcy and loyal friends.

The two common characteristics for a majority of the management team are loyalty to Toby + a complete lack of experience in building AI data centers.

Of Fermi’s remaining 7-person C-Suite. We identified 6 out 7 that are Toby loyalists.

- 3 management team members have been accused of being involved in fraudulent schemes with Toby

- Another 3 are Toby’s good friends from his past

Unfortunately for Fermi’s investors that are still long the stock Toby departing does not solve Fermi’s management problems. Experts told us Fermi lacks the management talent to execute on Fermi’s Plan.

“The people that they have running it are unreliable”

“I’m just not seeing any plans nor people that can execute those plans.”

~ AI Data Center Expert

CFO & New Board Member – Miles Everson >$8 Million via alleged Fraudulent Scheme for Phantom Services w/ Toby

Fermi’s CFO, Miles Everson, may not be an expert in AI data centers, but he is a long-time friend of CEO, Toby Neugebauer. In fact, Toby used his power to name Miles to the board in the same late Friday 8-k that announced Toby’s exit. At Toby’s bankrupt venture, GloriFi, the bankruptcy trustee accused Miles and Toby “executing a scheme” to “fleece” the shareholders via Miles’ consulting company MBO. The trustee states that MBO had a “sweet-heart deal to drain the debtor” that allowed them to provide phantom services and overbill GloriFi. The scheme allegedly netted them $8.79 million in just 12 months. Miles disputes the bankruptcy trustee’s allegations that it was a “fraudulent transfer” among friends.

Fun facts about the partnership:

- Miles was also on the board of directors at GloriFi at the time

- Toby promised to Miles you will “make a s**t ton off this deal”

- Toby ensured Miles’ business, MBO, got paid even when GloriFi couldn’t make payroll

So obviously when Toby needed a CFO for the “largest energy construction site going on in the world today”…he signed up Miles.

Director – Rodrigo Acuna – Accused of Scheming with Toby to “Misappropriate” Assets Worth >$20 Million

In a new lawsuit that was filed in early April, another Fermi senior employee, Director of IR, Rodrigo Acuna was accused of allegedly scheming with Toby to misappropriate assets.

Rodrigo Acuna previously served as the VP of Finance at GloriFi with Toby – a fact that he’s conveniently omitted from his LinkedIn. The trustee’s complaint states that on the eve of bankruptcy Acuna and Toby hatched a scheme and conspired to launch a separate company, IM Financial, and without paying GloriFi investors anything they misappropriated Intellectual Property worth >$20 million.

Chief Site Officer – Charlie Hamilton – Toby’s ‘Yes Man’ That Approved Millions in Fraudulent Backdated Debt Securities

Charlie Hamilton is currently the Chief Site Officer for Fermi. Bankruptcy records describe Charlie as “Neugebauer’s long-time friend and ‘yes man.” In fact, we found 10 LLCs that are owned by both Toby and Charlie together and their business partnership spans >20 years.

Hamilton joined Toby on the board of bankrupt GloriFi after Toby ousted other board members and wanted to “stack the deck with friendlies.” Once Hamilton joined the board Toby allegedly engaged in fraudulent backdating and insider dealing.

Naturally Hamilton said “yes” to the debt transaction with the allegedly “fraudulent backdated debt.”

$19 Million+ Reasons to Backdate Securities for Charlie Hamilton & Toby Neugebauer

Entities owned by Hamilton and Toby and other insiders were accused of being involved in back-dated convertible debt worth ~$19 million. The debt agreements were allegedly backdated with false issuance dates in order to establish priority in bankruptcy over other investors like Peter Thiel. The court agreed with the bankruptcy trustee and avoided many as fraudulent transfers since the documents were actually signed months later.

Charlie Hamilton Entities:

- Lynnwood Partners (owned by Charlie Hamilton) – $200k

- Charlie Hamilton (self) – $1.175 million

- Banzai Capital Partners, (Toby & Charlie Hamilton controlled) – $3 million

Toby Neugebauer Entities:

- Neugebauer Family Enterprises LLC – $9.1 million

- Animo Bancorp, owned by Toby & his wife – $5.8 million

New Interim CEO – Real Estate Developer in Puerto Rico + Toby’s Neighbor at Golf Club

Fermi CEO Jacobo Ortiz was just named the interim CEO on Friday after the close. But long before that Jacobo was a FoT (friend of Toby). We uncovered Jacobo is Toby’s neighbor in the same Puerto Rican Dorado Beach & Golf Resort.

Jacobo appears to have ZERO experience running a massive data center & power generation construction projects. Jacobo is the founder of a Puerto Rican Real Estate Firm that is also a full-service Property Manager. It is unclear to us how his accreditations as a Licensed Real Estate Broker and Certified Property Manager will help Fermi get their AI Data Center and Power Generation operations up and running. We guess at least his experience with real estate tenants prepared him for cleaning up messes.

Toby and Jacobo apparently became good friends after Toby moved to Puerto Rico back in 2014 and became a resident reportedly to pay no federal income or capital gains taxes.

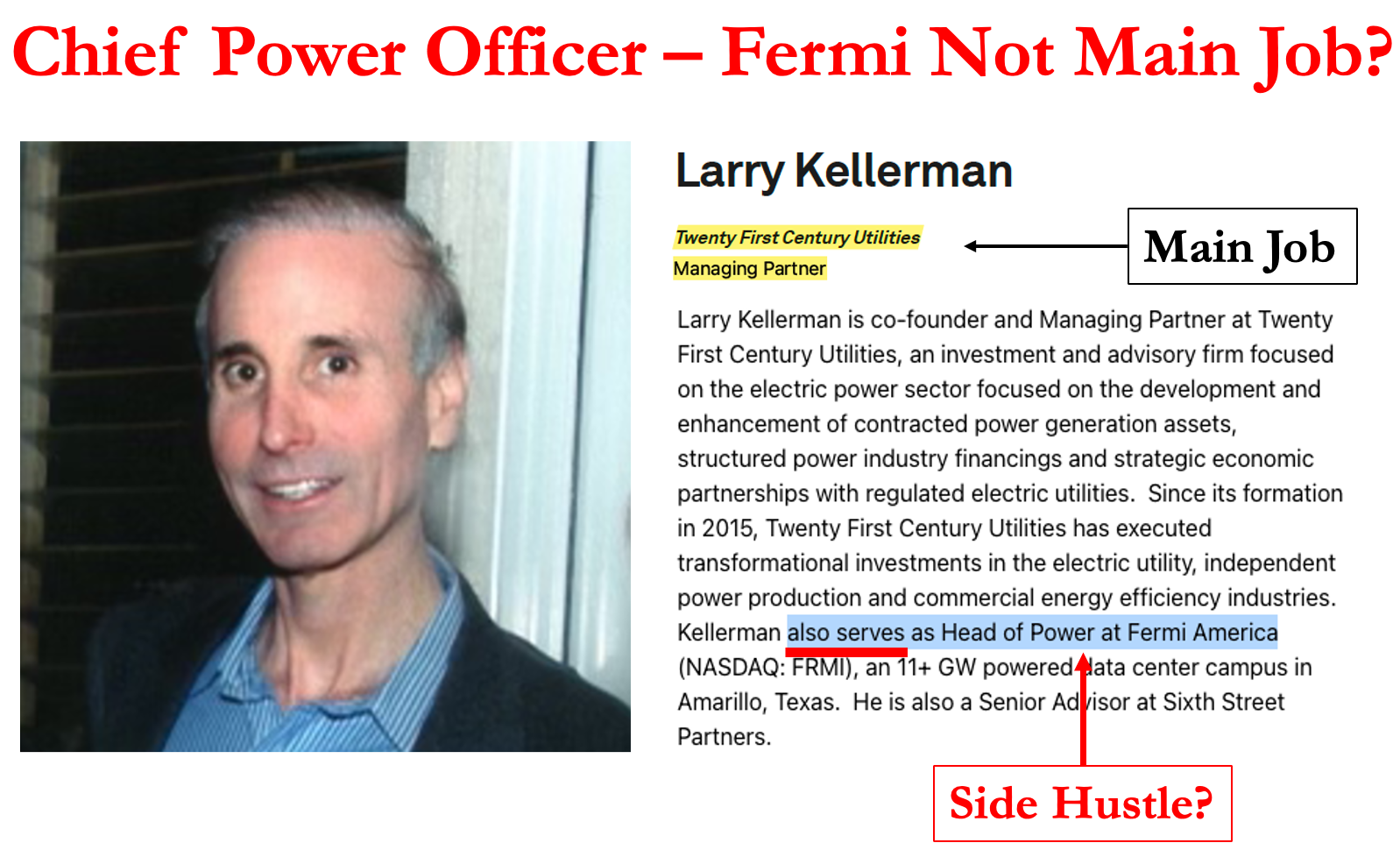

Chief Power Officer – Larry Kellerman – Long-time Friend of Toby -Fermi Not Listed as His Main Job? A Side Hustle?

Larry Kellerman is another long-time friend of Toby’s. They worked together at Quantum Energy Partners.

for multiple years and Toby helped recruited Larry to join the firm. Very strangely, Fermi says Larry Kellerman is its Chief Power Officer yet at a late March conference Kellerman’s bio appears to Not even list Fermi as his main employer.

Is Fermi just Kellerman’s side hustle?

This should concern investors even more because Larry Kellerman (70) is one of the few people on Fermi’s management team with actual Utility and Power Gen experience.

Backdated Related Party Contract for Kellerman? How Could Past Monthly Payment Amounts Increase?

Fermi first disclosed (in it’s July S-11) that it had a consulting contract with a related party to Kellerman’s to pay $35,000 per month for consulting services. The services agreement began on April 1, 2025. Then 2 months in the Sept prospectus the April 1 agreement was apparently now $15,000 a month higher and is listed at $50,000.

It’s very odd the historical monthly dollar amount paid to Kellerman’s firm increased >40% in the same contract, but I guess we gotta respect Kellerman’s hustle. Make that money Kellerman.

Other Fermi FoT’s – Friends of Toby’s + Family Members

There are even more of Toby’s inner circle at Fermi. There are both family members and long-time loyal FoT’s (Friends of Toby’s). It’s actually hard to pinpoint exactly how many people came from the bankrupt fin-tech company since most people don’t list GloriFi on their LinkedIn.

Both of Toby’s sons (1, 2) are key executives at Fermi. Toby’s wife is not an employee but Toby has stated that she run’s Fermi’s Charity. Even Toby’s Gulfstream pilot lists being a Fermi employee. Fermi’s 10-K only lists 35 employees, it’s market cap is ~$120 million per employee.

Many of the other senior Fermi executive team members previously helped Toby bankrupt the fin-tech company GloriFi. Notably, they also lack experience building AI data centers and power plants.

Fermi’s Charity – 1.8% of Shares Given to DAF Run by Toby’s Wife

Before it went public, Fermi had Toby give shares equaling 1.8% of the company to create a donor-advised foundation. Neither Toby nor Fermi have provided any details of what charitable work is being done. But Toby told the Amarillo, Texas, city council meeting in October that his wife Melissa would be leading the charitable donations.

Chief Marketing Officer, Cathy Landtroop – FoT that saw Toby Day Drink Regularly at GloriFi

Cathy also worked with Toby at bankrupt GloriFi. Cathy was the CMO at GloriFi as well. We are actually surprised that Cathy was willing to sign up for another adventure with Toby. Deposition records show that Toby tried to blame Cathy for GloriFi’s demise and that Cathy regularly saw Toby “microdose” alcohol throughout the workday.

EVP of Capital Markets – John Donovan

John Donovan also previously worked with Toby at Quantum Energy Partners. Donovan’s venture firm also partnered with Clearcove Advisors, an advisory firm that Toby’s son, co-founded.

Co-Founders – Rick Perry & Griffin Perry – Friends of Toby

Griffin and Toby are good friends and in media interviews they say that they came up with the idea to start Fermi while on of their frequent walks together.

We aren’t going to denigrate the former Texas Governor’s and his family’s legacy by writing about his past trips on Toby’s private jet or Toby’s large campaign donations for 2 reasons.

- 1) There needs to be adults left in the board to finish clearing out Toby’s FoT’s

- 2) And because Saturday Night Live already did that, so here are some of the SNL clips if our lack of depth has left you wanting more (SNL – Weekend Update: Rick Perry)

PART II – Short Fermi America – Are FRMI’s Key Suppliers Undisclosed Related Parties?

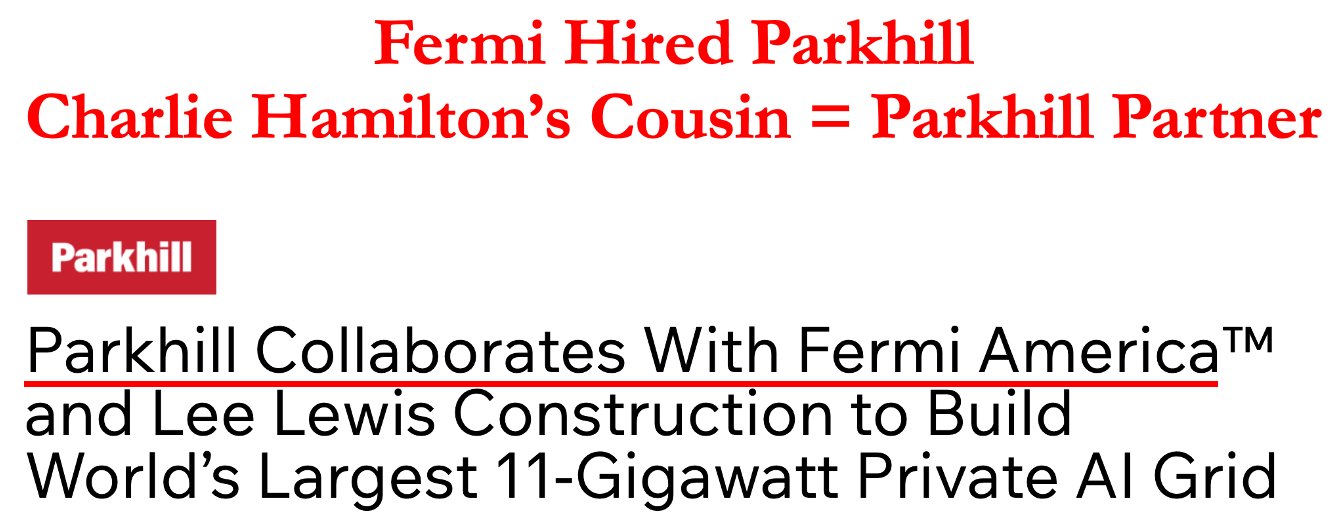

Key Engineering Firm – Parkhill – appears to be an Undisclosed Related Party

- Engineering Firm’s Co-Owner is a Relative of Fermi’s C-Suite – Undisclosed Related Party?

- No Top EPC Firm Involved in Phases 0-2

- Lack of Engineering Plans = Major Red Flag

- Another Undisclosed Related Party – Other Co Even Discloses it as Related Party Deal, But Fermi Doesn’t

- General Counsel Accused of Fraudulent Transfer Scheme too – Involving Siemens Turbines

“They’ve hired a know nothing … to do the engineering…Parkhill. I looked them up, and I can’t even find anything they’ve done.”

“They [Fermi] don’t have the engineering procurement side that’s needed for a power plant.”

~ AI Data Center Expert

Experts told us having a top EPC (engineering, procurement, and construction) firm is essential for getting a massive project like Project Matador built on time, on budget, and without massive quality issues. For a combined cycle plant, the EPC plan typically has ~1,000 components which need to be fulfilled at the correct times. The EPC firm is not only responsible for procuring all the correct components but also ensuring that all the electrical, power, and other equipment work flawlessly. But for phases 0-2, Fermi chose not to hire a top EPC firm like Bechtel or Flour.

Instead, they hired a relatively unknown and less experienced firm, Parkhill, to be in charge of the engineering plans. Industry experts told us that they had never heard of Parkhill and this choice was a huge red flag. If Fermi wanted to hire locally, there is a top EPC firm headquartered nearby in Odessa called Saulsbury Industries. Parkhill has not built any AI data centers or power plants but some of Parkhill’s recent projects include a fire station and a pickleball complex.

So why would Fermi hire Parkhill for engineering vs a Bechtel or Flour?

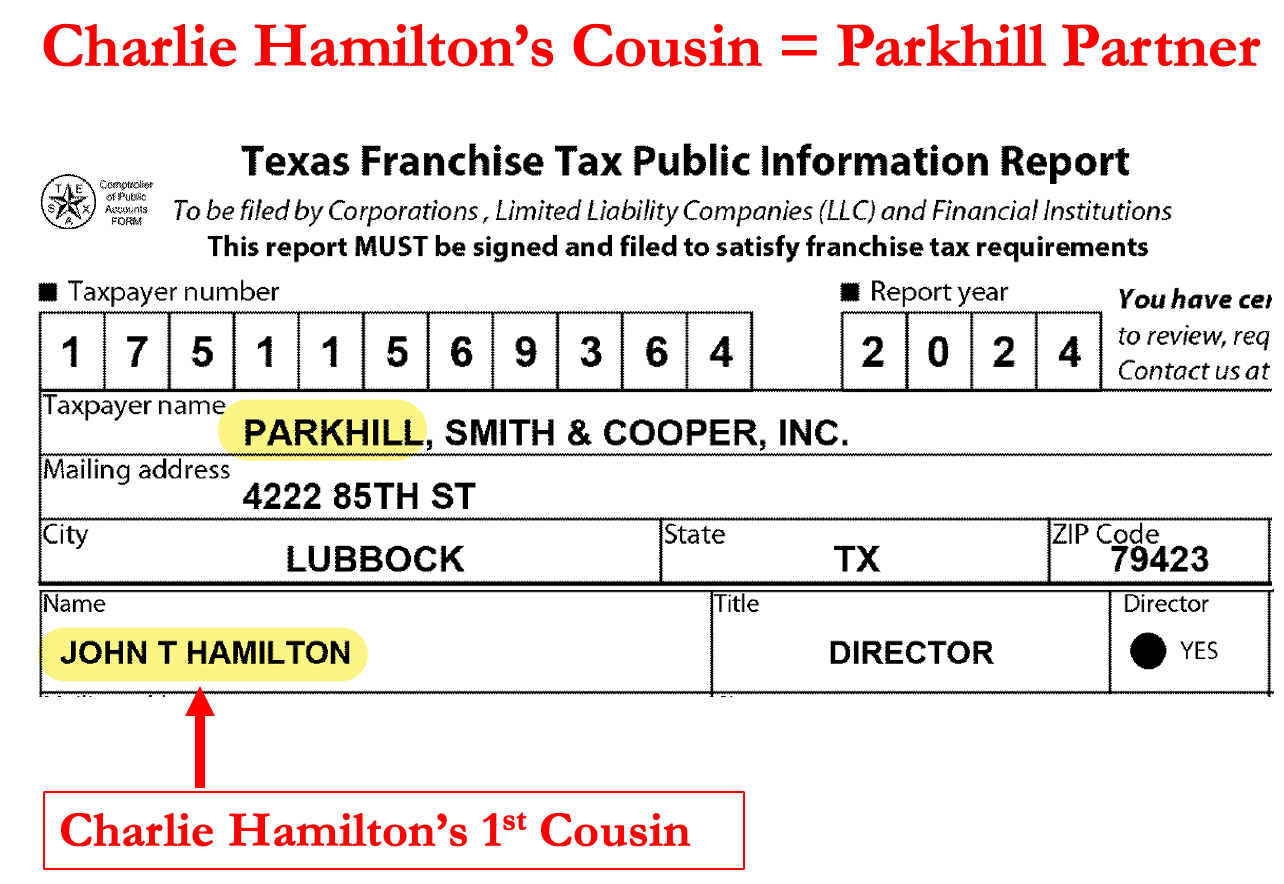

We uncovered that an owner of Parkhill is an actual relative, 1st cousin, of the Fermi C-suite. We believe Parkhill is an undisclosed related party.

- Charlie Hamilton is Fermi’s Chief Site Officer.

- One of Parkhill’s owners and partners is John T. Hamilton.

- John is Charlie’s first cousin! They are business partner in various ventures together too

Reminder that at GloriFi the bankruptcy trustee alleged that Toby & Fermi CFO, Miles Everson, schemed to execute “fraudulent transfers” for “phantom services” via a company owned by Miles. It’s extra concerning that there is a potential undisclosed related party connected to Charlie, Toby’s “Yes Man.”

Key Engineering Firm, Parkhill, is Part-Owned by a Cousin! Isn’t it an Undisclosed Related Party when you’re actually Related?

Experts thought hiring Parkhill was a red flag due to lack of experience, but since it appears that Parkhill is an undisclosed related party we believe it’s red flag status should be upgraded – Parkhill is a red Matador’s Cape calling in bulls to be slaughtered.

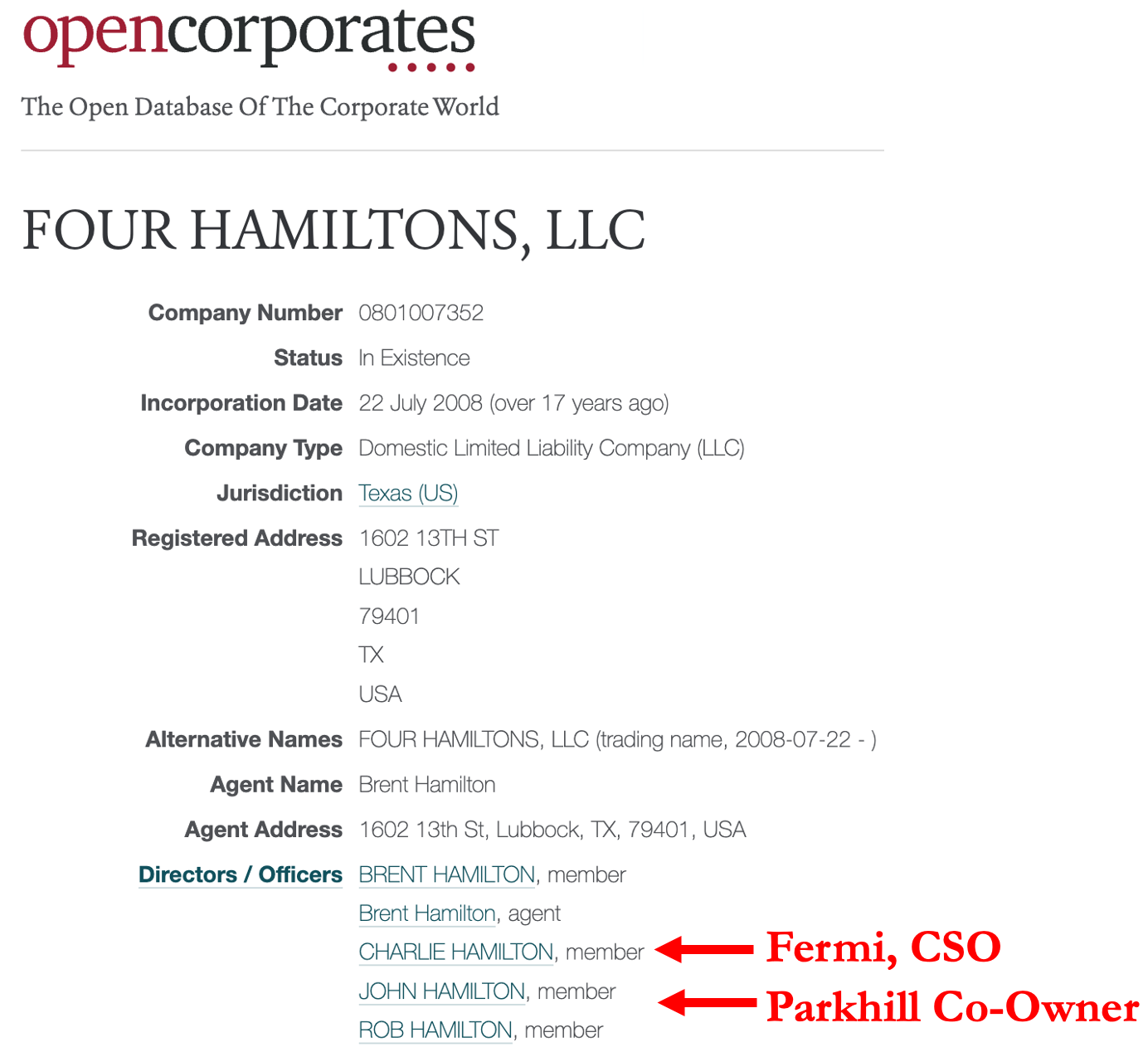

Texas Tax records show that John T. Hamilton is one of the directors and partners listed for Parkhill Engineering. We uncovered that John Hamilton is the 1st cousin of Charlie Hamilton the Chief Site Officer at Fermi.

Charlie and John are also both members of Four Hamiltons, LLC, which appears to be their family holding company, with John’s brothers and Charlie’s other cousins, Brent and Rob.

Fermi Lacks a Top EPC firm for Phases 0-2 & Experts Say they lack a real EPC Plan

We consulted experts in the AI data center field to understand the viability of Fermi’s Project Matador plans. They told us a major red flag is that Fermi lacks a real EPC plan (Engineering, Procurement, Construction) and that the project is already at least 6 months to 1 year behind schedule.

The expert also said having Jacobo Ortiz (previously the COO) as the new interim CEO is a major issue, and that Jacobo is not qualified for the job.

The biggest concern is that they haven’t hired an experienced EPC Contractor (e.g. Fluor, Bechtel, etc.). This is a major flaw for a project of this magnitude. In addition, the person they announced as the COO (Jacobo Ortiz) is not qualified for this job.”

~AI Data Center Expert

Our expert speculated there were only a couple possible reasons why Fermi would take the unprecedented step of cobbling together different small local service providers and trying to handle all the procurement themselves instead of hiring a top EPC firm. It was either that EPC firms would not take the job or that Fermi lacked the funds to guarantee the EPC firm would be paid.

- Failure Risk – Top firms “will not take a project they think will not succeed.”

- Major Timeline Change – Top firms would force Fermi to disclose major timeline changes

Notable Nuclear Exception on EPC – Leading the Fermi nuclear plans are Mesut Uzman and his wife Sezin Uzman whose credentials appeared by all our research to be incredibly legit. We think the Uzman’s could effectively get the nuclear part of the project done if only they had unlimited capital + 5-10 additional years. On the nuclear side, Fermi/the Uzman’s have actually engaged with a top EPC player, Hyundai Engineering & Construction, and they have begun to put in place long lead time agreements with Doosan and Westinghouse.

Unfortunately, we believe the Uzman power couple are going to eventually hit the harsh reality of how much more difficult it is to get a nuclear power plant up and running in the USA vs their past project successes in the UAE and China.

But many of those challenges will take place well after Fermi is bankrupt and Toby & the FoT’s are long-gone. Perhaps they will rename the Amarillo nuclear project “Project Uzmans” in 10-15 years.

Another Undisclosed Related Party Transaction? Energy Transfer Discloses Fermi as a Related Party, But at Fermi … it’s Not Disclosed

It’s ok (but still not ideal) to have related party transactions as long as they are properly disclosed. Undisclosed related party transactions are a definite No-No. We found another undisclosed related party transaction and this one involves Fermi’s key supplier, Energy Transfer, who is contracted to supply Fermi natural gas for their turbines.

Energy Transfer (which does > $85bn in revenue and >$15bn in EBITDA annually) thought it was prudent to disclose (ET 10-K – Pg 163) that a small $30 million per year transaction with Fermi is a Related Party Transaction. Energy Transfer (ET)’s affiliate ETC Marketing has a gas supply agreement to provide Fermi with natural gas for Project Matador. Energy Transfer discloses this deal as a related party transaction since it is one, Rick Perry is a board member of both Energy Transfer and Fermi.

Yet, somehow Fermi in their S-11/A, press release, and 10-K failed to disclose the important detail that the gas supply agreement that is utterly essential to the success of phase 1 and 2 of Project Matador is with a related party. In fact, Fermi spent ~2 pages of the S-11 on the Energy Transfer gas supply deal but somehow conveniently forgot to disclose that Energy Transfer should be deemed a related party transaction.

How could Fermi’s management think it’s acceptable to engage in related party transactions without disclosing them?

Oh, Fermi’s General Counsel has been accused of running a “Fraudulent Transfer Scheme” too. Now it makes more sense to us why Fermi doesn’t disclose companies that we believe should be classified as related parties.

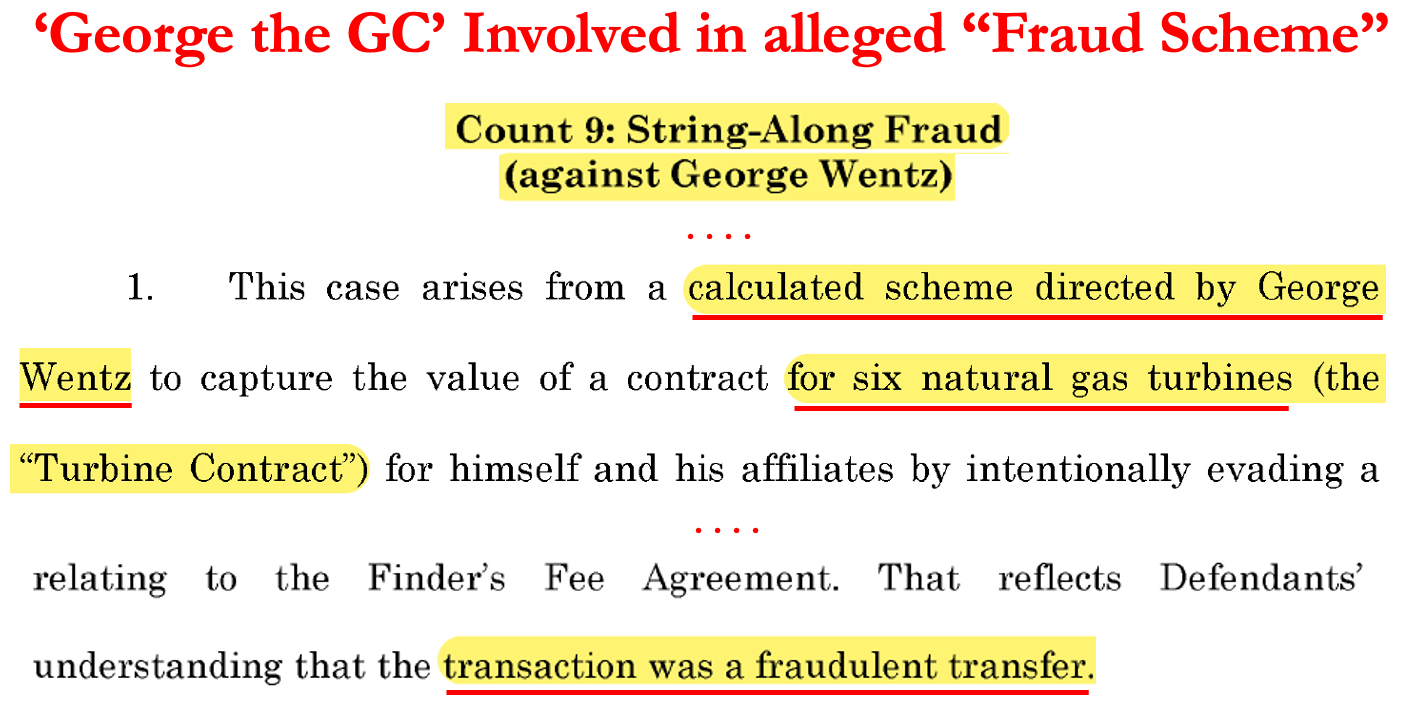

George the GC – Also Accused of a Fraudulent Transfer Scheme! It Involved FRMI’s Siemens Turbine Deal

- Siemens Turbine Deal Could be Reversed

We uncovered in another lawsuit that Fermi’s General Counsel, George Wentz, (affectionately known to us as “George the GC”) has been accused of a “fraudulent transfer scheme” too.

Before joining Fermi, ‘George the GC’ ran a company called MAD Energy. George joined Fermi and became GC after Pre-IPO Fermi bought Firebird LNG (fka as MAD Energy). Fermi bought Firebird/MAD in order to get MAD Energy’s contract for 6 Siemens Turbines. In a legal complaint, the plaintiff is suing George, MAD Energy, and Fermi regarding their Siemens Turbines Deal. The defendants are all accused of executing a “fraudulent transfer scheme” after ‘George the GC’ didn’t pay the broker for the transaction.

Essentially, the complaint states George made sketchy corporate moves in order to try to avoid paying a large broker fee he owed on the Siemens Turbines. George’s company had a Puerto Rican subsidiary/entity that signed the contract with a broker to help them sell the six turbines. Once the broker made the deal with Fermi, George’s Co, MAD Energy, allegedly pulled a move that caused the Puerto Rican subsidiary to go bankrupt. Then George completed the same deal with Fermi but under the new corporate structure, MAD Energy. And apparently ‘George the GC’ never paid the broker despite promising in writing as well as in multiple phone calls that he would pay them.

It might sound confusing, but it really isn’t. All you really need to know is that ‘George the GC’ says in writing that he definitely had a contract + “now we are in a position to pay you” and George even allegedly assured them he “did not want to see them get screwed” and wouldn’t “f-ck [them] out of a commission.”

Oh and this whole debacle might actually cause the Siemens Turbine deal to be reversed since the plaintiff is requesting the courts to unwind the deal as recourse if their $5m+ commission isn’t paid.

We actually think it’s only a small outside risk that the court would unwind the deal, but wild things are known to occasionally happen in Texas court cases. The more likely downside risk for Fermi is that Fermi/MAD Energy is forced to pay them the $5 million+ plus in broker fees.

The way larger problem and questions for investors are:

- How can investors possibly trust Fermi’s disclosures regarding things like “related parties” when even the GC has allegations of fraud against them?

- How the heck did Fermi make George Wentz the GC when they were well aware of this situation and the allegations of his conduct of running a scheme like this?

In fact, George first shows up as GC on Fermi’s website in March 2026. Fermi management was apparently well aware of these problems since July 2025.

PART III – Short Fermi America – Catch-22

Catch-22 — Why Fermi Doesn’t Have a Tenant Agreement? They Lost the Financing

- Toby Promised $5-5.5 Billion of Financing…It Never Came…So their Tenant Left

- Securing Billions of Debt for Dirt is Hard

Fermi is now stuck in a catch-22 and they can’t win.

- No tenant will sign a definitive contract until Fermi has raised multiple billions of dollars in financing that will de-risk the execution of completing Phase 1 of Project Matador.

- To raise billions of unsecured financing, Fermi would first need to get a tenant.

We believe Fermi accidentally revealed the real reason they lost the $150m of AI Hyperscaler financing from Tenant #1 (widely reported as Amazon, so we will just refer to Tenant 1 as Amazon). We think Amazon walked because the deal was contingent on Fermi raising >$5 billion of financing.

Now, we think there is no chance that Fermi can get the financing because Fermi doesn’t have the assets to back the loans. No responsible debt underwriter is going to loan this management team multiple billions of dollars unsecured by hard assets. Fermi has only been able to raise a small amount of debt, but only when it is backed by high demand hard assets like turbines, and at very conservative terms (55%-65% LTVs and with high interest rates). There aren’t assets left to finance the additional billions of debt Fermi’s needs.

The only primary assets left to secure billions of needed loans are a cancelable lease on a plot of dirt + the broken dreams of a company that just gored its own matador.

Tenant 1 Amazon Disappeared because Toby Promised $5.2-5.5 Billion of Project Financing that Never Appeared

We think Toby accidently revealed the answer to a big secret. Why Amazon disappeared?

The secret was revealed within 3 hours of an October Amarillo City Council meeting. During the meeting, Toby promised the Amarillo City Council that Fermi was going to be able to secure $5.2-5.5 billion in project financing. How he was going to do it – he told the council his plan was to use the tenant 1 hyperscaler contract (actually an LOI) to convince NY banks. Toby then gave an oddly specific deadline that the loans would be secured by:

- Toby told the Council Fermi needed to close $5.2 billion in project financing by Dec 9, 2025 (time-stamp 3:56:07)

Why does December 9th matter?

- December 9th = last day of Fermi’s exclusivity period with Tenant 1/Amazon

So it’s either a huge coincidence of date choice or Toby revealed the real reason why Amazon walked. Because Fermi couldn’t raise the $5+ billion of financing by the end of the exclusivity period.

Why Banks Said No to Fermi’s $5+ Billion in Financing Before Amazon Walked?

Clearly the banks and debt investors said no way! We believe it’s either because bankers:

- Couldn’t underwrite the deals economics – Financiers would have viewed the full terms of Fermi’s LOI with

AmazonTenant 1 - Couldn’t underwrite the assets/development plan – We know the EPC plan is still missing key parts, and only some of the high demand hard assets (e.g. turbines) could be used to secure loans

- Couldn’t underwrite the team – Or the banks did the same diligence we have. They read the bankruptcy filings and uncovered that Fermi’s founder, CFO, CSO, and others were accused of fleecing investors with fraudulent transfers.

- Or maybe banks didn’t even need to do deep due diligence. They could’ve just called investors Toby & Team allegedly fleeced like Jeff Sprecher (NYSE chairman), Ken Griffin, or Peter Thiel.

Either way, the NY banks balked and the AI hyperscaler walked. Without the billions in financing to pay for the required capex and build-out to finish Phase 1 there is no hyperscaler deal to be had.

What an AI Hyperscaler Wants?

AI hyperscalers want a stable project that has been completely de-risked. Deals that happened include some of these features:

- Top-notch Management Team that Can Execute

- Zero Financing Risks

- No Risks to Power Supply

- Proper Electrical Infrastructure & Data Interconnect

- Completed Build out of Data Center

A project without these features are non-starters for an AI hyperscaler. No one will sign a firm lease for a data center that doesn’t have all the necessary project financing and detailed execution plans in place. Having part of the power secured and air/water permits just isn’t enough.

Compare Fermi to TeraWulf which not only has an exceptionally strong management team but has already built and operated data centers, has power secured, and has even successfully run pilot programs.

PART IV – Short Fermi America – Drones Show Empty Dirt Fields

Drone Flyovers show Fermi’s Campus is Mostly Empty Dirt Field

- Initial Drone Flyovers Showed Empty Dirt Fields

- Nothing Built & Nothing Banks Can Underwrite

- Late March Visit on Foot = Not Much Happening

- Construction Halted in Feb 2026 – Workers Got Laid Off

Below is footage from our drone’s initial flyover of Fermi’s Project Matador. The project site is large…and largely filled with empty dirt fields.

It was immediately obvious why no banks would underwrite a $5 billion+ loan to Fermi. There were no real hard assets to recover in bankruptcy, just lots of dirt.

The only place where work was ongoing was along the west side of Fermi’s site with a little bit of construction around the edges (pipelines and trenches being dug up and put in). It was a very nice day out, we enjoyed it. We found rebar for concrete pads laying around and basic dirt grading was being done. At the time, no buildings had been built. The foundations hadn’t even been poured. There weren’t even concrete pads poured for the turbines.

Fermi’s social media also highlights zoomed in construction on the west side of the site. One of the construction achievements they brag about is … wait for it … 11.3 miles of fencing.

Yes, fencing is good to have, but definitely not something a bank can use to secure billions in financing.

West-Side of Fermi’s Project Matador – Looking Southwest

Middle of Fermi’s Project Matador – Looking Southwest

Above are the exciting images…but unfortunately most of the >5,000-acre project site looked like this.

South-Side of Fermi’s Project Matador – Looking East

West-Side of Fermi’s Project Matador – Looking East

Note – All the above drone videos and images are from flights that took place at the end of FY 2025 occurring near the beginning of December/end of November. We attempted to get updated drone footage, but we believe Fermi has been able to block all 3rd party drones from viewing their progress (or lack of progress). The Fuzzy Panda drone pilots have applied for additional flight permits[1] at least 5 times over the last 4 months and all of them have been denied.

If Fermi has nothing to hide shouldn’t investors be able to see what is really going on?

Northwest of Fermi Project Matador – Late March

Grounding our drones annoyed us, so we went back in late March and took pictures on foot this time. We still didn’t see much going on.

There certainly wasn’t anything that happened that would unlock billions of $’s of bank loans to be released to Fermi.

Site Visit in Early February 2026 = “Dirt with a Dream”

We spoke with multiple people that attended a Fermi site visit in February hosted for bankers and investors. We asked them what they saw. They confirmed the project still looked the same as our drone footage when they were taken on the grand tour. They said the “site was very empty” “we saw some footings with rebar, the power lines didn’t look like much.” They told us “Really there was just lots of dirt,” it was “A piece of dirt with a dream.”

Construction Halted in February 2026

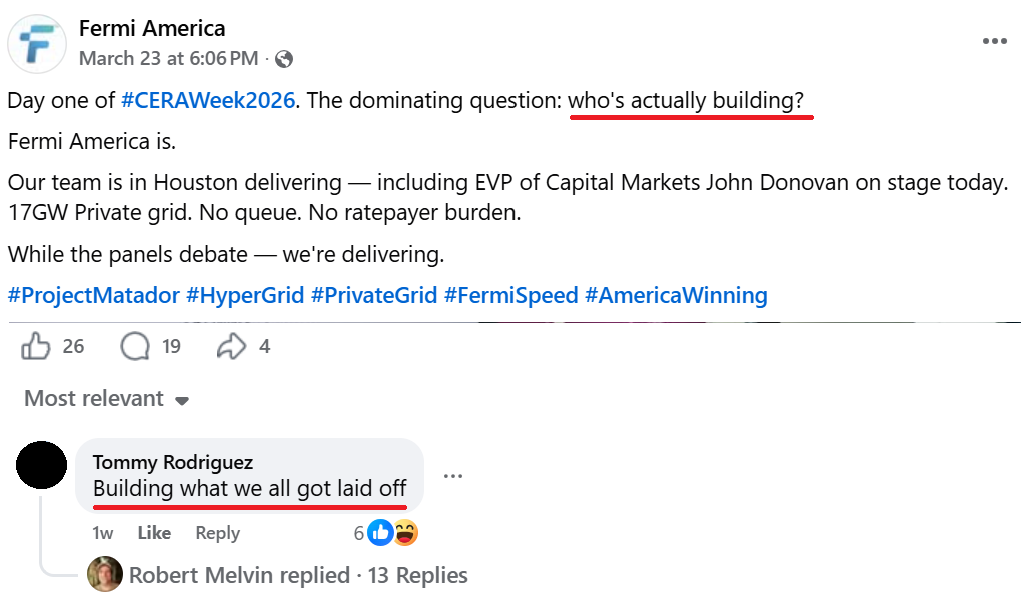

The reason why not much had changed since our drone flyovers is that Fermi halted construction in Early February 2026.

In late March, construction workers were still complaining on social media saying “we all got laid off.”

PART V – Short Fermi America – Running Out of Cash

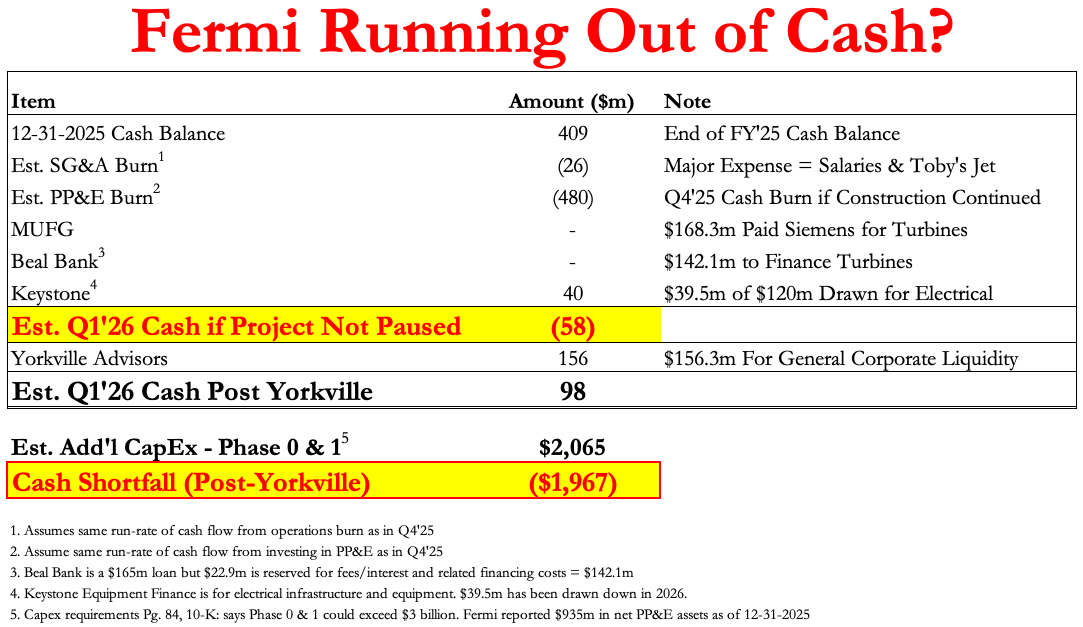

Fermi Is Almost Out of Cash!? – If Construction Continued Through End of Q1 Est Cash Balance is NEGATIVE

Fermi’s cash crunch is real. In Q1 they had to put up their assets as debt collateral to get financing at tough terms and even had to resort to death spiral toxic financing to provide near-term liquidity. This is NOT what gets you an AI hyperscaler tenant.

Our analysis shows that if Fermi had not stopped construction and instead had continued building out their site and manufacturing their power plants, then at their Q4 cash burn rate they would’ve ended Q1 with an estimated NEGATIVE $58 million of cash.

Most of Fermi’s financing went directly to turbine manufacturers. It came at high interest rates:

- MUFG loan – only shows $168.3m being released. Funds went to pay Siemens directly. Loans are secured by Siemens Turbines and came at a 55-65% LTV w/ a pretty high rate of SOFR + 4%

- Beal Bank – only $142.1m released and also went to finance the Siemens Turbines. More financing that wouldn’t have paid for site construction. Also secured by the turbines and it sports a ridiculously high 12% interest rate.

- Keystone – Drew down $39.5m of a $120m financing facility. Loan is secured by long-lead time electrical equipment at an 80% LTV. We are counting it as paying for part of Fermi’s regular construction burn. The loan has a nose-bleed 12.9% interest rate. That’s terrible!

Fermi is in a Catch-22. They need a hyperscaler to get project financing at decent interest rates to continue construction, but before they can get project financing they need to sign a definitive contract with a hyperscaler. It just doesn’t work.

It’s no wonder Fermi had to get toxic death spiral financing from Yorkville. We think it’s more likely Fermi goes bankrupt by the end of the year than signs up a hyperscaler tenant.

Our estimates and Fermi’s disclosures show that Fermi requires at least $2 billion more of equity/debt financing. And that is just to complete phase 0 and 1.

PART VI – Short Fermi America – More Capital & Time Required

>$2 Billion of Capex Needed + Project Timeline Keeps Getting Worse

- Lacks the Cash to Pay for 2026 Capex

- REIT that is NOT Cash Flow Positive Until Q4-2038

Timeline and costs have gotten way worse since Fermi went public.

At the time of going public in Oct 2025, Fermi’s plans were to deliver at least 1.1GW of power to a hyperscaler by the end of 2026. They claimed operations would launch in April 2026. It’s April 2026 now, and the site is still a pile of dirt and rebar…so they obviously failed at that.

Fermi also originally said Phase 0 & Phase 1 would only cost ~$2 billion. They have failed at that too. The capex required keeps growing. Now Phase 0-1 is said to exceed $3 billion.

Investors should prepare for both the disclosed timeline and the expected capex costs to get way worse once new management resets the bar.

Capex Keeps Increasing – Phase 0-1 alone increased by $1 Billion in 6 Months

The required capex to complete Phase 0 & 1 for Fermi has increased by ~$1 billion since IPO. The disclosed estimates provided by Fermi are set to exceed $3 billion to build the minimum product necessary.

- Phase 0 & 1 to require approximately $2 billion of capex (Sept 30, 2025 Prospectus)

- Phase 0 & 1 could exceed $3 billion of capex and $2 billion in the next 12 months (10-K, pg 84)

Our experts think it will be significantly higher as Fermi’s impending operational challenges from not having an EPC will cause costs to keep stacking up.

You only need basic math to see that Fermi is going to fail. Fermi only had $408.5m of cash as of 12-31-2025 and they disclose that they need ~$2 billion for capex for the next 12 months. Also, they just fired their CEO who was previously accused of making fraudulent transfers to himself.

We assign a <0.1% probability of Fermi raising the capital required to finish Phase 0-1%.

Total Capex Needed = $70-90 Billion; Fermi had Less Than $0.5 Billion in Cash at Year End 2025

Not many people have $69.5-89.5 Billion laying around to make a bet Fermi. Even less have that type of cash reserved for a management team stacked with the FoT’s (Friends of Toby).

If somehow your Fermi valuation is resting on all the Phases of this dream project occurring, then we have a Nuclear appendix for you. For everyone else, we think it’s pretty safe to assign a <.002% probability to Phase 3 & 4 being successful.

Why a .002% probability?

We actually think it’s a 0% chance but it’s a whole lot funnier to assign the same probability as the price that Toby & Griffin paid for their shares. Yep, the founders actually paid $0.002 a share. On a serious note, the only reason it’s not fully a 0% chance is because Mr. And Mrs. Uzman are the members of Fermi’s team that our research has found to be the most competent, they are legit experts.

So, Project Matador’s cost and timeline overruns will have killed the bulls thesis long before any analysis about Phase 3 & 4 delays actually matter. But if “Project Uzman” ever pops up in Amarillo well after Fermi likely goes bankrupt. Then we might be interested in investing.

Project Timeline Keeps Slipping = Bad News for Investors

Experts told us a hyperscaler tenant won’t sign a firm contract until Fermi has reliable power up and running at the site, so when Phase 1 is complete.

Fermi’s Timeline Keeps Extending:

- Phase 1 operations to commence in March 2026 (Sept 30, 2025 S-11/A)

- Phase 1 operations to commence in Q2 with a completion date of December 2026 (Q3-10Q)

- Phase 1’s commissioning readiness could occur 1H 2027 (10-K pg 9)

Our AI data center expert told us if Fermi had the capital required to complete Phase 1 (they don’t) and had a great EPC firm that could execute (they don’t) and a tenant today (they don’t) that the 1.1 GW Phase 1 would be completed in the best case scenario by Q4-2027

“If they were to get a tenant [today]…full Phase 1 all the way to 1GW, you’re looking at fourth quarter next year (2027)” ~AI Data Center Expert

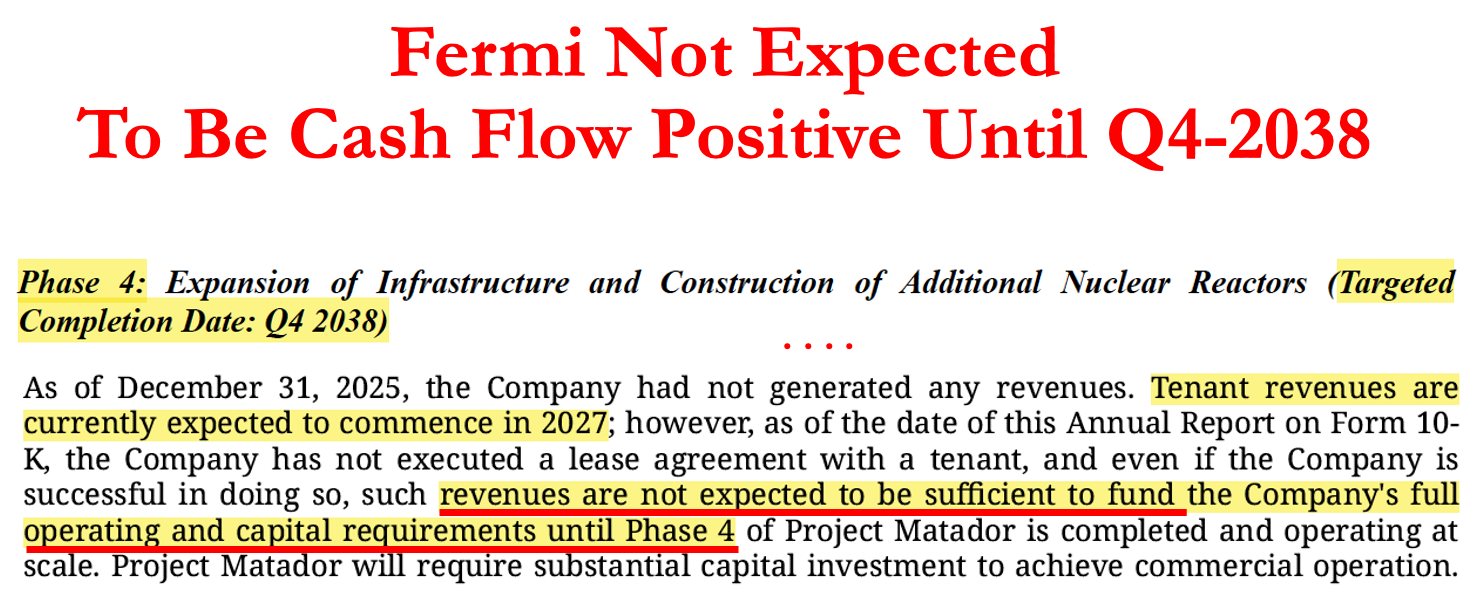

A REIT that is NOT Cash Flow Positive Until Q4-2038!

If you are betting on Fermi delivering the great economics that Toby told tall tales about, we hope you are very very patient. SEC disclosures show that Fermi’s SEC lawyers don’t expect the company to be able to be FCF positive until Phase 4.

Phase 4 is also obviously delayed but the S-11/A had targeted an expected completion date of Q4-2038.

We don’t think Fermi will survive 15 months based on their capex plan, 15 years would be a miracle.

PART VI – Short Fermi America – Power Plan’s Missing Pieces

Missing Pieces of the Power Plan – Debt Holders Can Sell the Turbines if No 400MW Tenant in <7 months

- Electrical Plan Missing Key Parts

- Less Grid Power Than Promised

- Piecemeal Procurement will Result in More Turbine Timeline Troubles

On the last conference call Toby told investors that he would rather sell his 2 kids than the turbines to raise capital: “I would auction off my 2 boys first before I would let one of these gensets go.”

The problem is that selling the turbines is up to the debt holders, not him.

Debt documents reveal a major risk for Fermi that’s been caused by the continuously slipping timeline. If Fermi can’t secure a 400MW tenant by November 10, 2026 then debt holders can begin to market the turbines for sell.

Debt holders can SELL Fermi’s Turbines in <7 months!

Experts Said Fermi’s Electrical Plan is Missing Key Parts

“(Fermi) haven’t solved the electrical problem. If I had to just boil it down to one thing. It’s one thing to have a generator. It’s the other thing to hook it up and run a building. And that’s a total electrical issue.”

~AI Data Center Expert

Experts told us they thought Fermi’s plan looked piecemeal and was missing many key parts.

- Electrical Systems Do Not Appear Fully Integrated – Key decisions for Fermi on voltage, transformers, inverters, batteries, and distribution should have all been designed together. According to experts they weren’t.

- Piecemeal is Bad Plan – Fermi’s decision to buy turbines in piecemeal fashion increases the risk of redesigns, schedule slippage, and stranded equipment.

- Generation Does Not = Unstable Data Center Power – The harder problem is not buying turbines but it is delivering clean, stable electricity to AI servers. Inverters, Transformers, and Batteries all need to be aligned and able to handle the variations in output from the generators.

In layman’s terms, experts told us Fermi’s plan is missing many key steps. It appears Fermi has just skipped solving the details. This will lead to longer delays, higher costs, and worst-case unstable power that would actually burn up an AI hyperscaler’s computers and GPUs.

Missing Power? Only 86MW Secured from Grid out of 200MW Promised

Fermi is relying on using grid energy for a portion of its Phase 1 electricity needs. But it only has 86MWs out of 200MW secured with Xcel Energy’s subsidiary SPS. Fermi had originally promised it’d have the grid power by end of 2026. Now they are hopeful it will happen in 2027.

This is important because Fermi needs the 200MW to either provide the initial power for the facility and/or as a fail-safe if their on-site generators go down once the turbines are up and running.

No Secure Uninterrupted Power Source = No AI Hyperscaler Tenant

Turbine Timeline Troubles from Piecemeal Power Procurement

“Based on the lack of detailed engineering plans, piecemeal procurement, current management structure/personnel and contractors they have hired to do engineering and construction, there is very low probability that they can get these power plants operating on the current schedule.”

~AI Data Center Expert

Fermi has procured gas-powered generators and turbines from Siemens, GE, and Mobile Power Solutions. Fermi has stated plans to get the combined cycle system up and running by the end of 2026. Experts suggested this won’t happen until mid-2027 in the best case.

Below are some likely issues with each of Fermi’s Phase 1 power solutions:

Mobile Power Solutions (MPS) – Fermi plans on leasing generators from MPS to provide initial power for Phase 1. Experts said Fermi’s timeline for the MPS is “highly unlikely.”

For example, experts told us it took another company, CPS Energy, over a year to lease and install similar mobile power gen units into the South Texas Grid.

GE Turbines – Fermi acquired these pre-owned turbines with plans of refurbishing them in Houston. We don’t foresee issues getting the turbines refurbished since GE does this all the time, but we believe the timeline for getting them up and running is also highly unlikely.

“It will be impossible to get them [GE turbines] back, installed, and completed testing for operations in Q1, especially with the lack of substation infrastructure… the combined cycle addition would not occur until mid-2027.”

~AI Data Center Expert – Commentary Dec 2025

Siemens Turbines – Fermi acquired an LOI to purchase Siemens turbines from Firebird LNG. Experts opined that the price paid by Fermi for these capable units is in-line with industry estimates. But they also said getting them delivered and installed in one year is highly unlikely because of the lack of electrical infrastructure which is “very problematic.” They estimate it will take 18-24 months.

“It will take 18-24 months to design, engineer, procure, build, and test the new Siemens Turbines and Steam Systems once financing is available. Therefore, it will be 2027-28 before these new units are completed and tested.”

~AI Data Center Expert – Commentary Dec 2025

PART VII – Short Fermi America – Fermi Could Lose its Land Lease

Lease Docs Reveal More Problems – Another Reason Why Construction Paused + Could Lose Lease in <9 Months if No Tenant

- Real Reasons for Construction Paused

- Fermi Could Lose Lease if No Tenant by Dec 2026

- Key Water Permits Still Missing? Local Officials Said Fermi Hasn’t Even Applied Yet

Construction at the Fermi Matador site had been paused. Local newspapers reported the layoffs and workers recently complained on social media that “we all got laid off.”

Cantor and other sell-side analysts have said if Fermi builds it, a tenant will come. We agree, but there’s one big problem with that statement. Fermi is actually NOT allowed to build it unless they have a tenant, according to their lease agreement.

Toby blamed it on a delayed clean air permit but to be sure, we FOIA’ed local government and county municipalities to get copies of Fermi’s original & amended lease agreements with Texas Tech University (TTUS). We uncovered other key issues that investors need to be aware of.

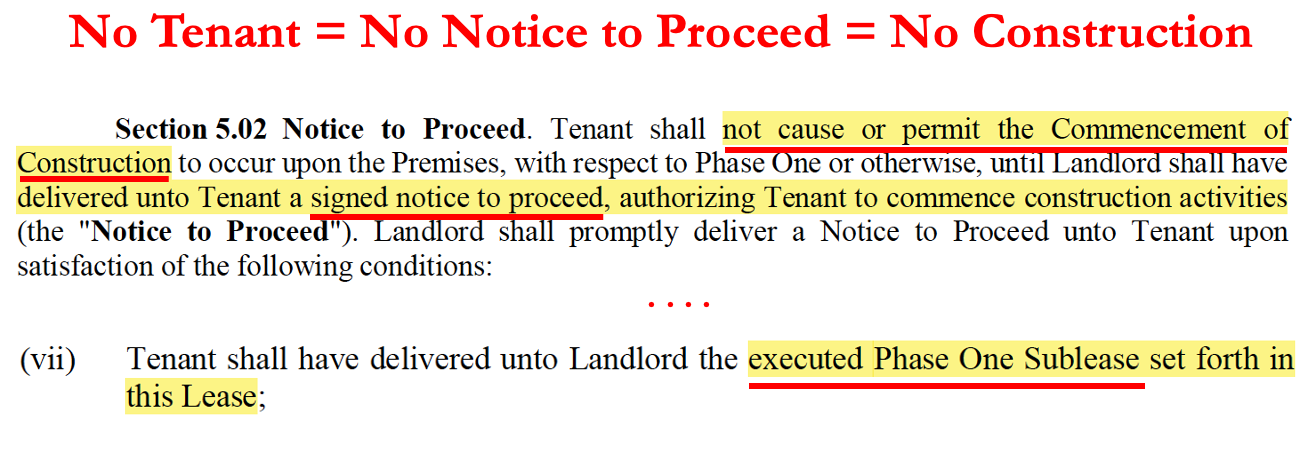

Construction Paused for Phase 1 Because Fermi Lacks University’s “Notice to Proceed”

Toby tacitly admitted on the March 30, 2026 earnings call to investors that construction has been paused. He said it was because he was a “financial sissy” he wanted to wait for a tenant to finish deploying and commissioning the power gensets. Local News reported Fermi’s construction actually paused earlier on February 6, 2026.

It appears that’s not the full truth. Besides the fact that Fermi is running out of cash, Fermi actually needs to have a “Notice to Proceed” from Texas Tech before Fermi can start the phase 1 construction. In order to get a “Notice to Proceed” Fermi is required to have a signed ‘phase one sublease’ which is defined as requiring a hyperscaler tenant that commits to a minimum of 200MWs utilizing at least 200,000 sq ft.

No Tenant = No University Notice to Proceed = Paused Construction

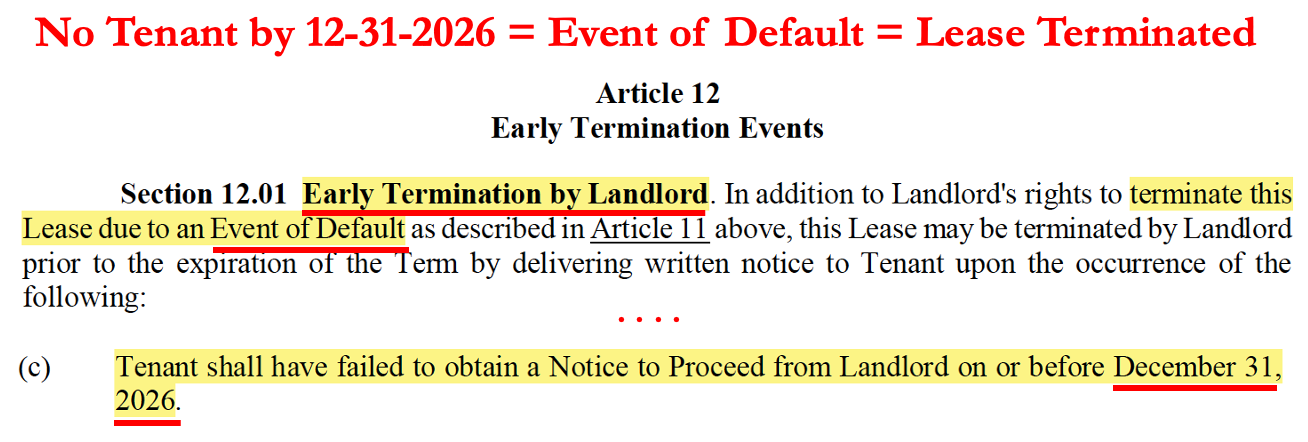

University Can Terminate Lease if No Tenant by 12-31-2026

If Fermi does NOT execute a Phase 1 sublease before Dec. 31, 2026, it’s considered an Event of Default under the terms of the lease agreement and gives the university the right to terminate the lease early.

Once Fermi receives the Notice to Proceed is when the clock starts running on key deadlines. And the lease states the target for Phase 1 is to be up and running in 2 years = 2028! Meanwhile, Fermi says Phase 1 is expected to be up and running in 2026.

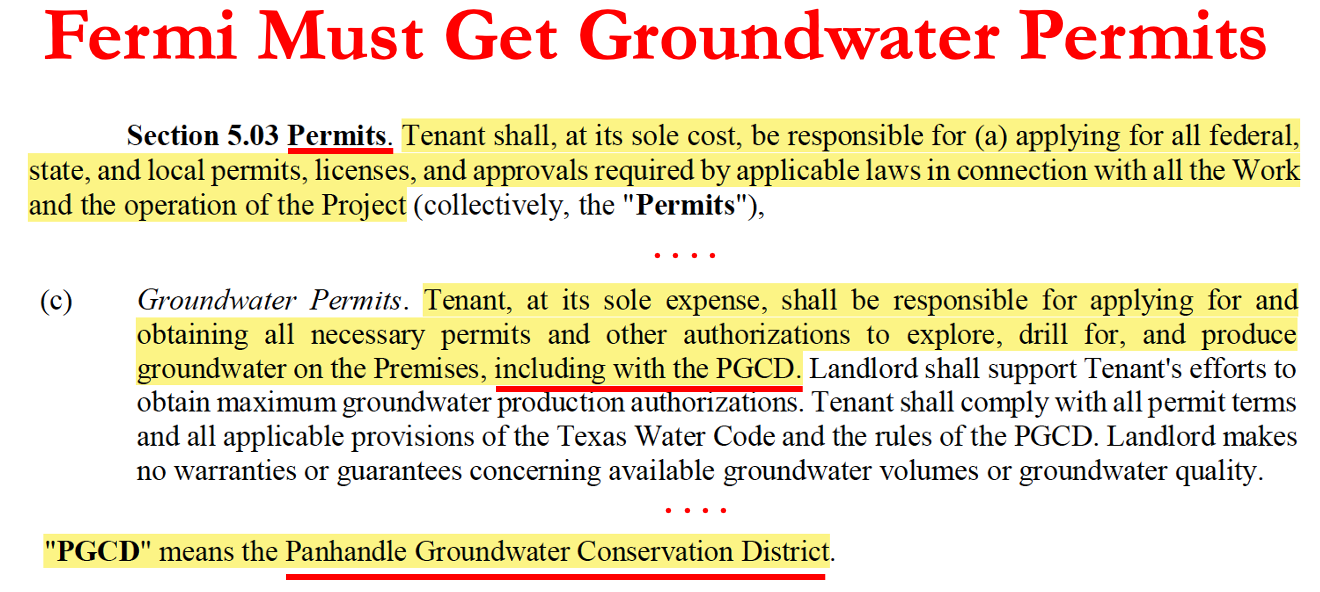

Still Missing Some Key Water Permits

Toby likes to brag about Fermi receiving Amarillo City Council’s water-supply agreement which allows the city to sell up to 2.5 million gallons per day to Fermi. Fermi contracted to pay a rate of 2 times higher than Amarillo taxpayers.

Something Toby neglects to share is that Fermi does NOT yet have all the water permits the project requires. Fermi’s lease lays out that Fermi is also required to get water permits from the Panhandle Ground Water Conservation District (PGCD).

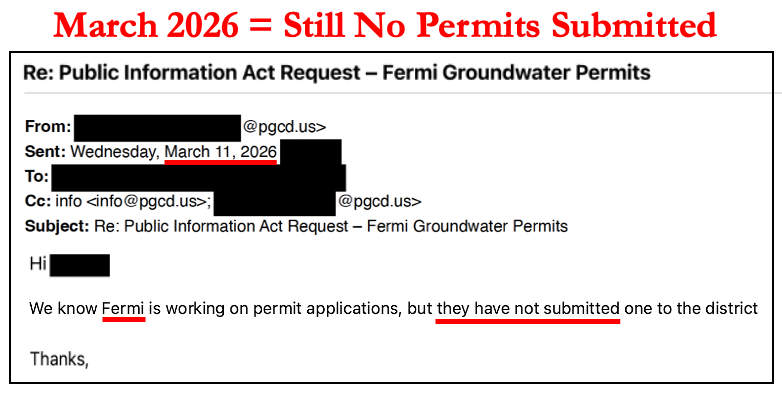

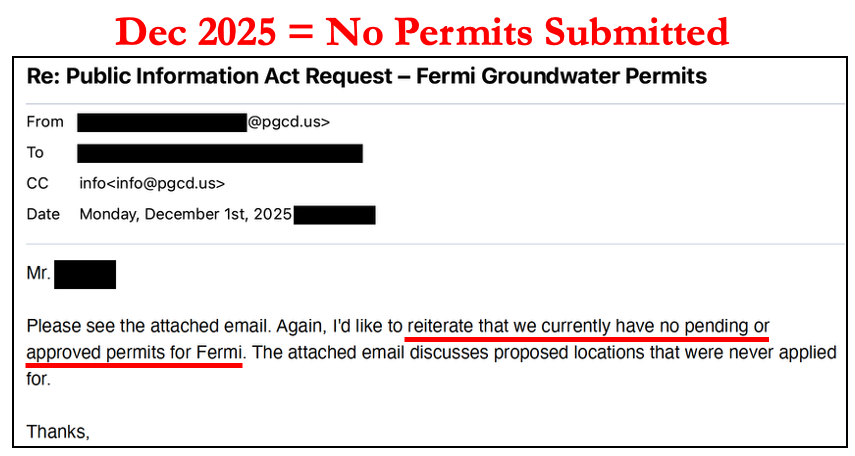

We uncovered via Public Information Act Requests that as recently as mid-March Fermi has NOT even submitted an application to apply for these necessary groundwater permits.

Fermi’s Amarillo Water Rights = only 2.5% of What Fermi’s Plan Requires

The City of Amarillo granted Fermi a water permit for 2.5 million gallons per day. But Fermi forgot to mention to investors that they will need >100 million gallons per day.

“(Fermi) will need more than 100 million gallons per day minimum just for the power plants alone”

~AI Data Center Expert

Other Undisclosed Financial Lease Terms – Investing in Texas Tech Seems Better Than Fermi

Looking at the actual lease terms of the Texas Tech-Fermi agreement, it seems like Texas Tech would be the way better investment. If Fermi scales, Texas Tech wins. If Fermi has delays or fails, then Texas Tech still wins.

- Phase 1 Delay = Large Penalties – $100,000 fine per day for each day of delay in achieving Phase 1 Sublease Commencement beyond the Target Phase One Date

- Increasing Rent Payments if Fermi ever scales:

- Annual Variable Rent – Fermi pays 1% of Data Center’s appraised value annually (up to $30 million) and 0.5% of the appraised value after that.

- Power Sales Revenue Rent – Fermi pays 1% of gross revenue power sales revenue

- Water Sales Revenue Rent – Fermi pays 25% of their water sales revenue

- Sinking Fund – Fermi has to build up a decommissioning fund starting at $10 million per year and growing over time

Additionally, Fermi must give free land to Texas Tech and build them facilities for a research campus, at their own expense. Essentially, Texas Tech gets a free data center built for them…if Fermi ever builds one.

If Fermi doesn’t ever get around to building a data center, Texas Tech still wins as Fermi took their plot of low value dirt and spent hundreds of millions of shareholder dollars on land upgrades and equipment.

PART VIII – Short Fermi America – Toby’s/Fermi’s PJ

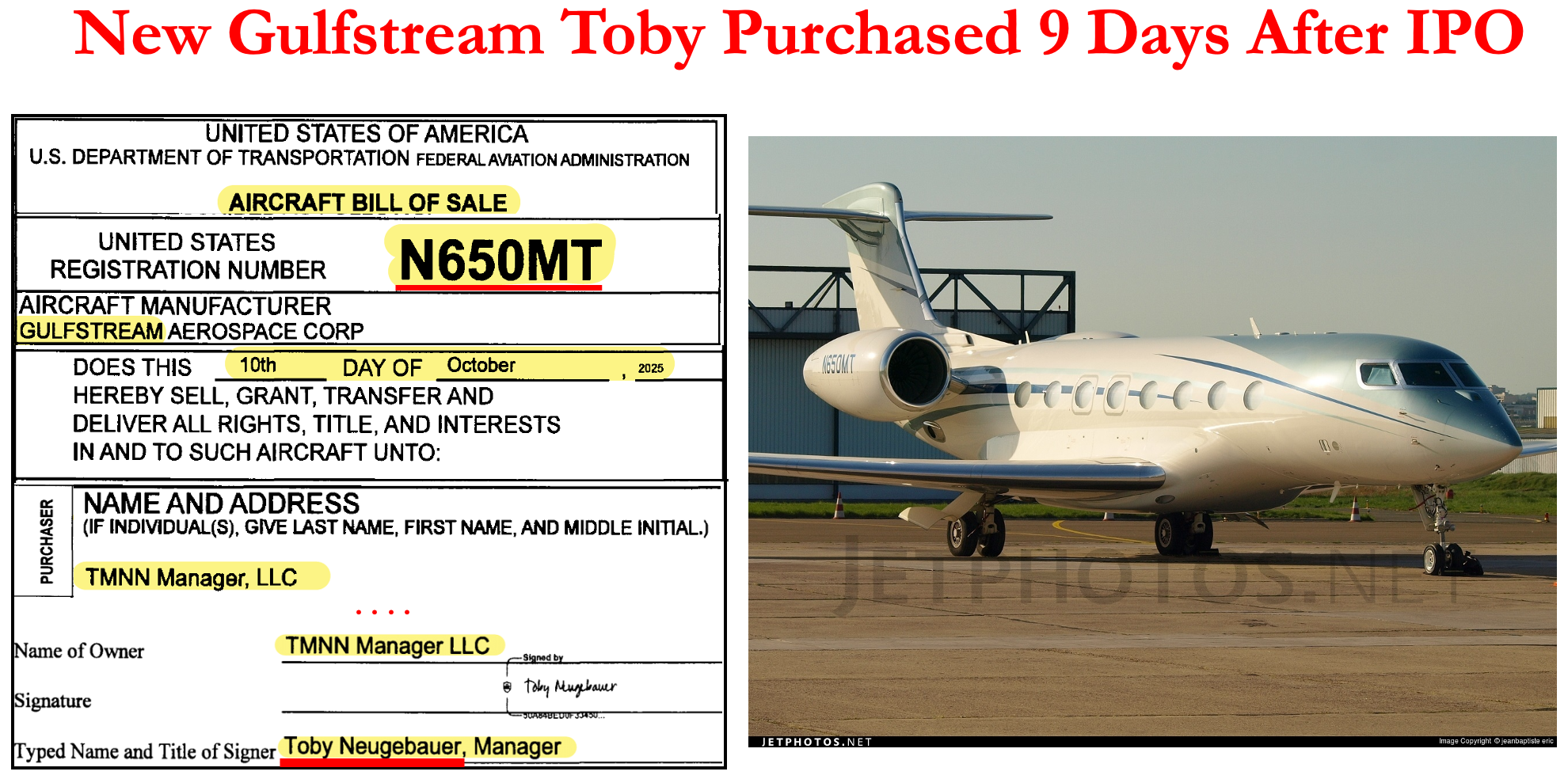

Tracking Toby’s Gulfstream – It’s Flown to Airports Near All Possible Tenants; Even Asian Ones (like China) & No Tenant!

Fermi went public on Oct. 1, 2025, so Toby did what any new executive tasked with deploying ~$750m of investor capital did. Toby went out and bought a Gulfstream G650 Private Jet valued at $44 million. FAA records show on Oct 10th Toby bought a Gulfstream (tail number N650MT) via his entity, TMNN Manager LLC. It’s unclear from the purchase documents if the est $44 million was paid by Toby personally or by Fermi’s shareholders, but we are sure we are going to find those spicy details out soon. However, the plane’s pilot definitely lists his employer as Fermi on LinkedIn.

Why has Toby Flown His PJ to China?

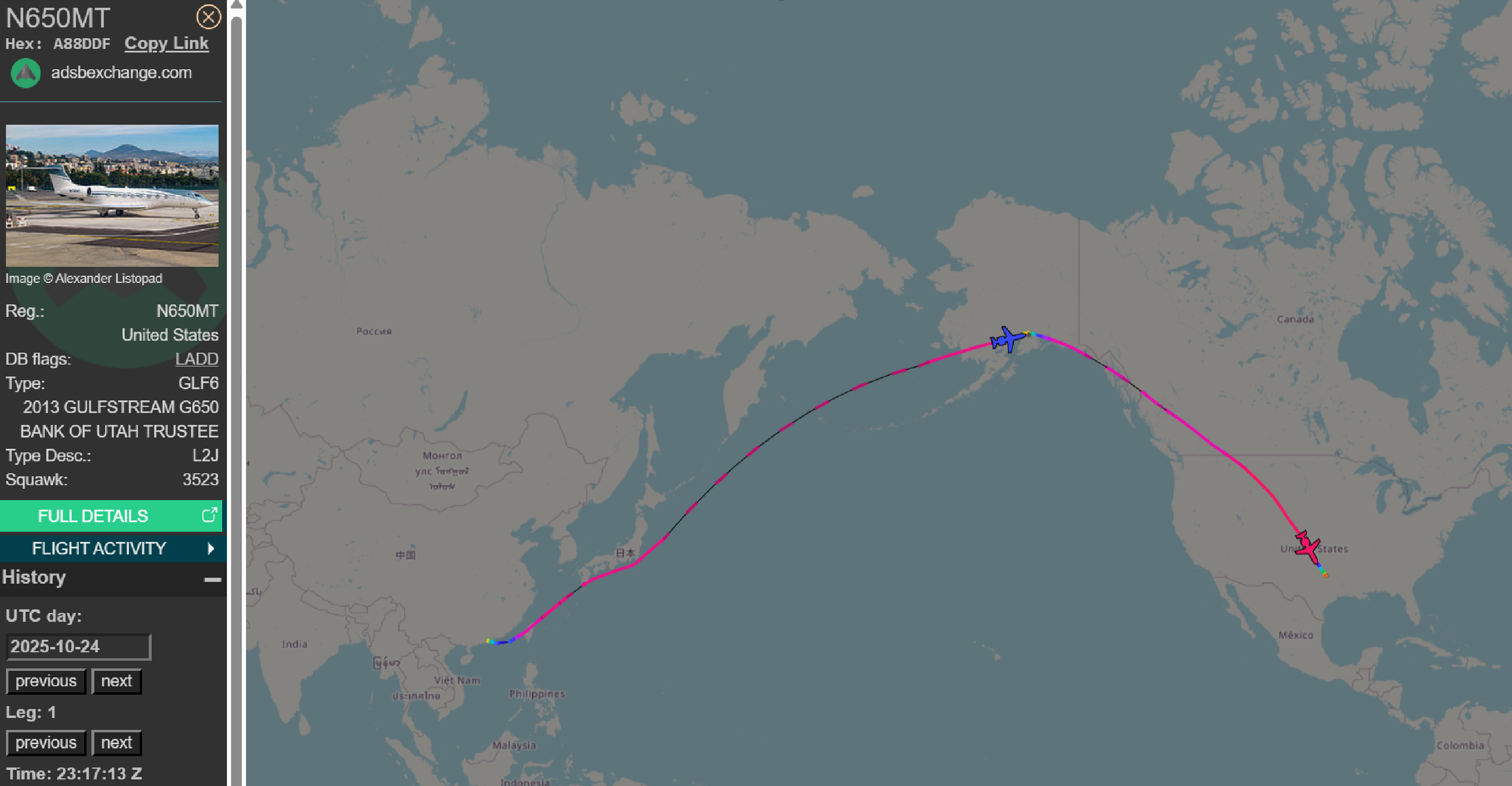

Oddly, one of the first thing Toby did after acquiring the jet was to fly to China & back in late October 2025.

Another odd trip took place immediately after the disastrous Q4-2025 earnings call at the end of March 2026. Toby flew directly to Asia. He spent 1 night in Tokyo landing at ~6:30pm local time and flew out at ~4am the next day. But as he left Tokyo his plane tracker turned off? It reappeared multiple days later flying towards Hawaii on a trajectory that appears as though he could have been flying from China again.

Toby’s Private Jet Flight Logs Show Flights to All Potential Hyperscaler HQ’s & Still No Tenant

Toby has used his private jet more often then we commute in a car. He’s put on more “Air Toby” frequent flier miles than Bonnie Blue has hammered on her bang bus.

Toby and his management team appear to be scrambling manically. There is still no tenant and they have visited the location of most of the hyperscaler HQs multiple times.

- Seattle – 5 times – and notably twice in the week before (Dec. 5 & 12) Fermi announced losing the $150 million construction loan from Tenant 1 and twice since (Jan 20 & Feb 4). But still no Tenant!

- Miami & West Palm Beach – 3 visits

- California – 2 visits

- New York – 3 visits

- DC – 4 visits

- Amarillo – 26 visits – in 5 months of being public, Toby has spent less than 1 month in Amarillo which is Fermi’s main project site

- Outside the US, Toby has also been to China, Singapore, England, Dubai, Turkey, Thailand, South Korea, and Japan.

Fun fact – Toby has flown to Colorado 12 times (normally landing at Eagle Airport). Toby has a house in Aspen so obviously it would be a shame for not having a tenant to have ruined a whole ski season.

From our public information requests we got the list of all the permitted Phase 1 tenants and their locations in the US. Toby’s visited each of these states multiple times yet can’t seem to get a tenant signed.

PART IX– Short Fermi America – Insider Selling, the Large Overhang

Insiders Dumping Shares – 94% of Float Just Unlocked

- 94% of Shares Just Unlocked on March 30th

- Fermi Insiders Already Sold >$67 Million

- >$1.2 Billion Left to Sell for Insiders + Another $1.3 Billion Can Be Sold by Toby

- Insiders Only Paid $0.002 per Share pre-IPO

A tight float and lack of shares to short were the primary things that has kept Fermi’s stock from collapsing to its current est cash value of (estimated at $0.33 per share). Even at $0.33 a share that is 148x above the founders cost basis of $0.002 from 14 months ago.

94% of Fermi’s float (71 days of ADV selling pressure) became available to sell last Monday 3-30-2026 and insider selling began immediately. The company has no AI tenant and lacks the cash to complete Phase 1 of the project. If you had hundreds of millions of your net worth tied up, what would you do?

Fermi Co-Founder Selling:

Fermi co-founder, Griffin Perry, immediately filed a form 144 to sell 20 million shares and proceeded to sell 11 million shares on the first 2 days on the unlock for ~$56 million. What’s even more surprising is that pre-unlock scuttlebutt we heard from traders was that Griffin was marketing a block of 30 million shares to sell on day one from his Pencross Energy entity.

Fermi CFO, COO, CSO Sold:

Last week, Fermi’s CFO, COO (now interim CEO), and CSO all sold shares for proceeds of ~$11.5 million. We speculate the only thing that stopped insiders from selling last week was that they were aware of the material event of Toby’s departure, aka being put out to pasture, was impending.

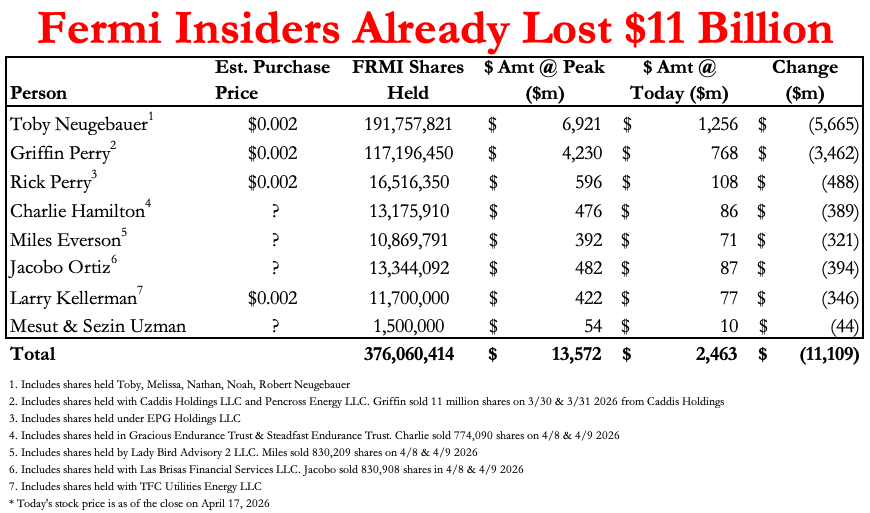

No Mas Tres Coma’s – Insiders Net Worth Has Been Decimated – Founding Shareholders Price Basis is ~$0.002

The internet was going wild about how many new billionaires were minted by Fermi IPO. But it’s playing out more like a scene from the TV Show Silicon Valley. Fermi’s insiders net worths are getting decimated faster than Pied Pipers’s code base when their investor put a ‘Tres Comas” bottle on the delete key. It’s especially fitting since 2 of those founders are already “out of the 3 comma club.”

Most of Fermi’s management team has already seen their net worth’s plunge by ~$350-500 million in the first 6 months post-IPO. There is lots of motivation to start realizing their profits since otherwise they might soon drop down into the 2 comma club.

Oh and the price that founding investors paid is absurd. They actually have a cost basis of $0.002.

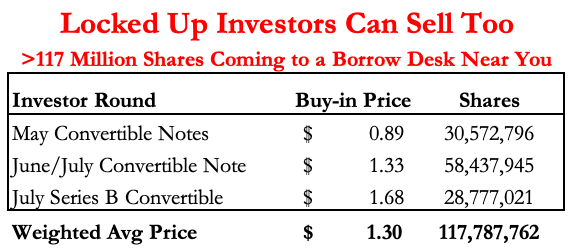

Expect >117 Million of Shares Coming to a Borrow Desk Near you – Financial Investors Can Dump Too

Financial investors similarly have an absurdly low-cost basis with a range between $0.89 to $1.68. These investors shares also unlocked on March 30th. We assume most of those investors have started slowly selling already, so you should expect~120 million shares of borrow to continue freeing up.

Fermi’s huge lock-up is like the gift that keeps on giving for short-sellers.

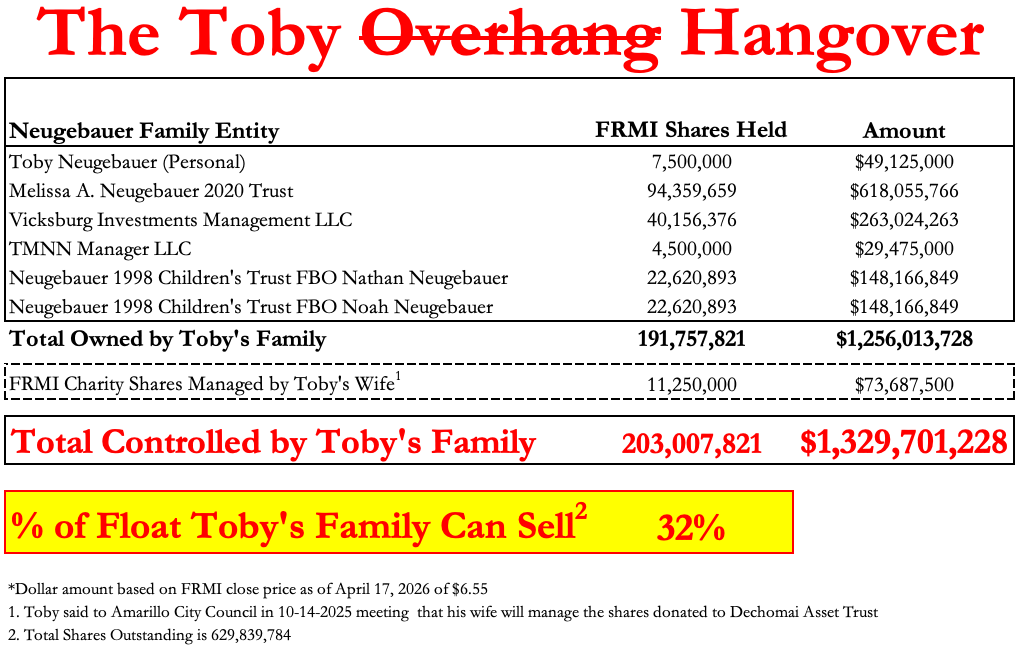

PART X – Short Fermi America – Toby’s Selling Soon – 32% Hangover

The Toby Overhang Hangover: Plans to Sell Stock – Controls 32% of Company Shares

- Toby Claims Planning an “Orderly Sell-down”

- Neugebauer’s Control 32% of Company Shares

- Toby Was Fired From CEO Position on Friday

- Let the Toby

OverhangHangover Begin

Toby and his family control 32% of Fermi’s float, he was just fired departed on Friday. But before that even happened Toby announced that he plans to sell stock. That sounds like a massive Toby overhang hangover to us.

On the March 30th Q4 earnings call Toby publicly admitted that he has hired an advisor to help his family sell a large block of shares. But now that Toby is no longer the CEO and has been removed from the board, will the sell-down be orderly?

Fermi/Toby’s Donor Advised Fund Also Needs to Sell – There’s also >11 million shares that Fermi donated to a donor-advised fund for Toby’s wife, Melissa Neugebauer, to manage (4:09:30). According to Toby, these shares will be used to make philanthropic donations in the Amarillo area. But in order to do so, those shares need to be sold for cash.

PART XI – Short Fermi America – Death Spiral Toxic Paper

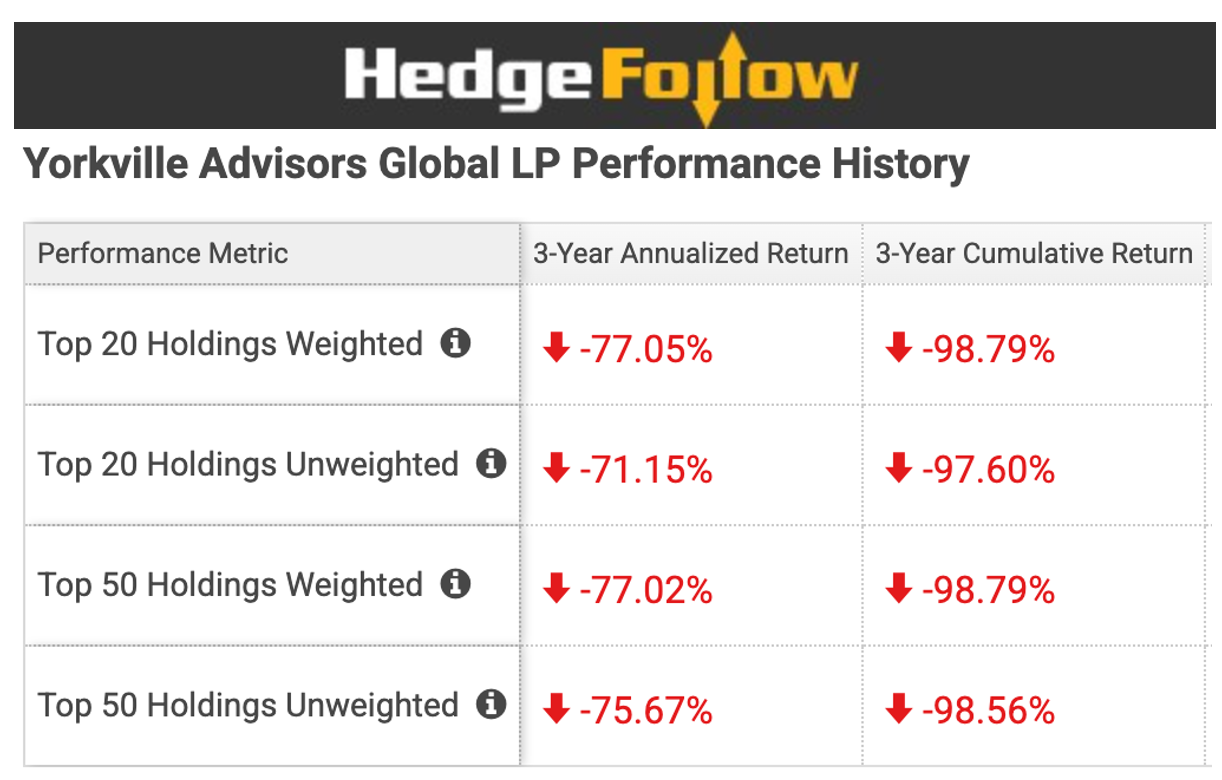

Death Spiral “Toxic Financing” Has Begun – Welcoming Yorkville to the Dirt Patch

“OMG, Yorkville’s involved now, Fermi’s toast. I used to screen for companies that had Yorkville toxic financing and short their stocks. It was a great source of alpha”

~ Former Hedge Fund Analyst, Current Fuzzy Panda Analyst

Fermi’s recent source of financing shows desperation and a huge cash crunch. Fermi committed to $156.25m of death spiral toxic debt financing from Yorkville.

Investopedia defines this type of toxic financing deals as “a type of debt often issued by companies in desperate need of cash.”

Yorkville terms include that the debt has to at least be partially repaid in stock. Fermi not only pays Yorkville an immediate 4% return but if Fermi repaid in cash instead of in shares, then Fermi owes an additional 2% premium. For Fermi to tap into this financing, they must issue shares to Yorkville at either the lowest daily VWAP of the days prior or a 9% discount to previous day’s closing price. Yorkville takes the Fermi shares they were issued and sells them in the open market causing downward pressure on the stock. And the further down Fermi’s shares fall, the more shares Yorkville receives, creating a negative cycle.

Yorkville wins while common equity holders lose. A service that tracked Yorkville’s top holdings calculated that equity holders in Yorkville’s top holdings on average lose >97%.

Interestingly not even Yorkville is willing to stick around long for Fermi. The amount Yorkville is willing to commit to Fermi declines monthly.

Note: the table above is NOT Yorkville’s actual returns. In fact, we believe Yorkville actually has quite good returns. This table shows the returns of the companies Yorkville provides toxic financing to and illustrates the equity performance of how stocks of companies needing toxic financing perform in the following years.

PART XII – Short Fermi America – Conclusion

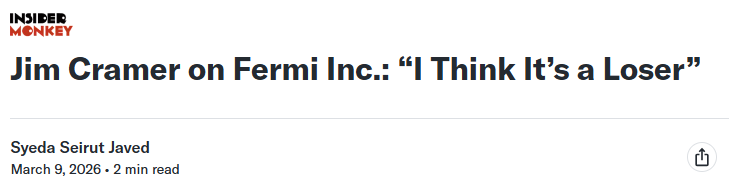

Conclusion – Even Cramer Thinks Fermi “is a Loser”

We obviously do not take our investment advice from Jim Cramer, but the true kiss of death is when even Cramer thinks your business is busted. Take Lordstown Motors, for example, a failed EV company that Jim Cramer called out for lying to him about having a serious order book for their EV’s.

Some people might think it’s a bullish argument for Fermi, but we think it just shows you how bad things really are if even Cramer thinks you don’t have a chance.

In March 2026 Cramer called Fermi “a Loser.” It was a loser from the day it came public”

In January 2026, Cramer said it’s more of a business plan than a business:

“Fermi’s more of a business plan than a business … I almost lost my mind when the market bestowed this thing a $19 billion valuation right out of the gate. Like I said at the time, no business plan is worth $19 billion. Fermi was at $32 back then. Now, it’s at under 10 bucks. I hope you dodged that bullet.”

~ Jim Cramer on Fermi

Toby is gone but not forgotten. Toby’s long-time friends and loyal lieutenant in (alleged) fraudulent transactions are still running Fermi. Fermi is in just as horrible a place as they were before the project’s mastermind “departed” — acres of empty dirt, turbines that could be auctioned off, and a cap table filled with high-cost debt and toxic financing. Even with the toxic financing they are still multiple billions of dollars short of the cash hole they need to climb to get an AI hyperscaler deal. Fermi’s Tenant 1 bailed because Fermi lacks the capital and management skill needed to turn build this field of dreams.

The co-founder and former CEO who controls 32% of the stock – and already suggested he planned to sell – is on the outside looking in. Other insiders and FoTs have already sold >$65 million, and collectively they + Toby have >$2.4 billion to dump. If there was a hyperscaler on the horizon, would insiders be cashing out? Of course not.

Fermi was once described to us as a piece of land with a paper-napkin business plan. The most expensive paper napkin ever sold was Lionel Messi’s original contract, it was sold at auction for nearly $1 million. It’s fitting that Fermi’s business plan could now be called the most expensive ever paper-napkin…because we think it’s bankruptcy will be very messy.

Now is the best time to Sell/Short Fermi. If you don’t prepare to be gored by the Matador.

Fuzzy Panda Research is Short Fermi (FRMI)

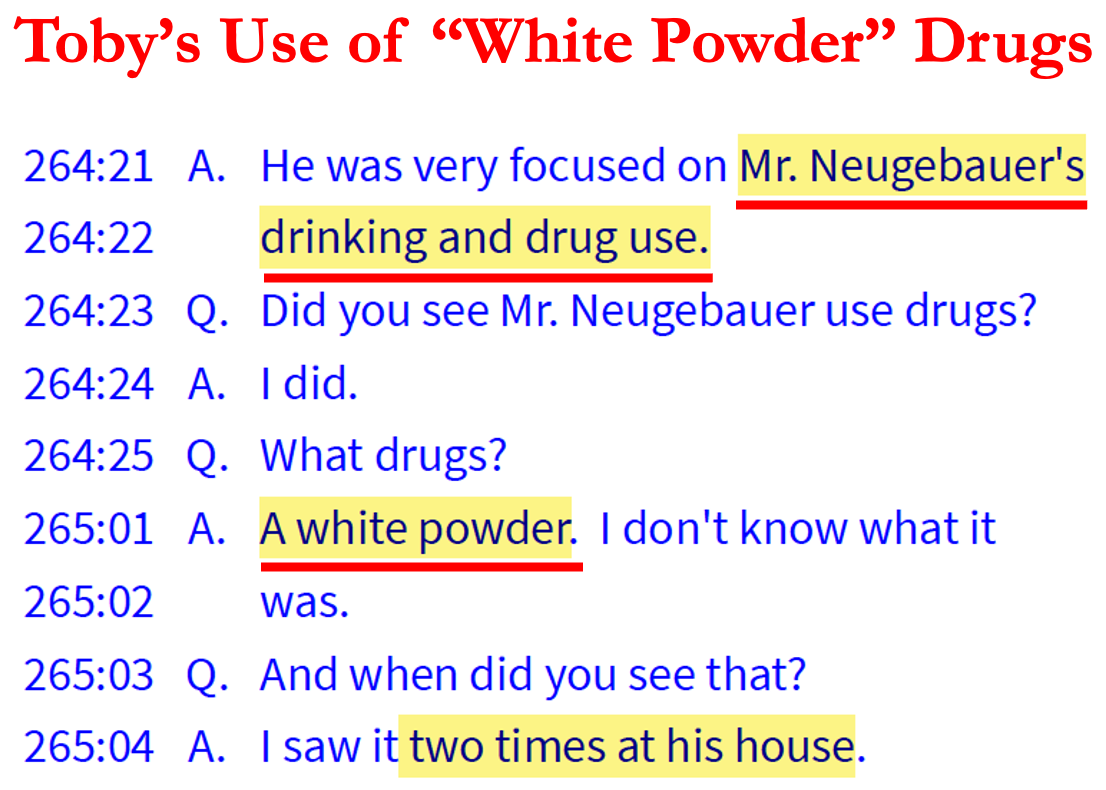

Appendix AA – Toby’s Alleged History of Drug and Alcohol Abuse + Threatened to Kill an Investor

- Did Toby drink “alcohol” throughout the day? YES

- Did Toby threaten to kill an investor? YES

- Did Toby use “white powder” drugs at work? YES

- At Fermi – Toby Had Yelling Outbursts

Bankruptcy dockets show that Toby managed to accomplish an “employee of the year” trifecta that not many people have done. Multiple employees said Toby would:

- Day-drink during work – Toby called it “microdosing alcohol”

- Used “white powder” at work

- Then threatened to grab a gun and kill Vivek Ramaswamy

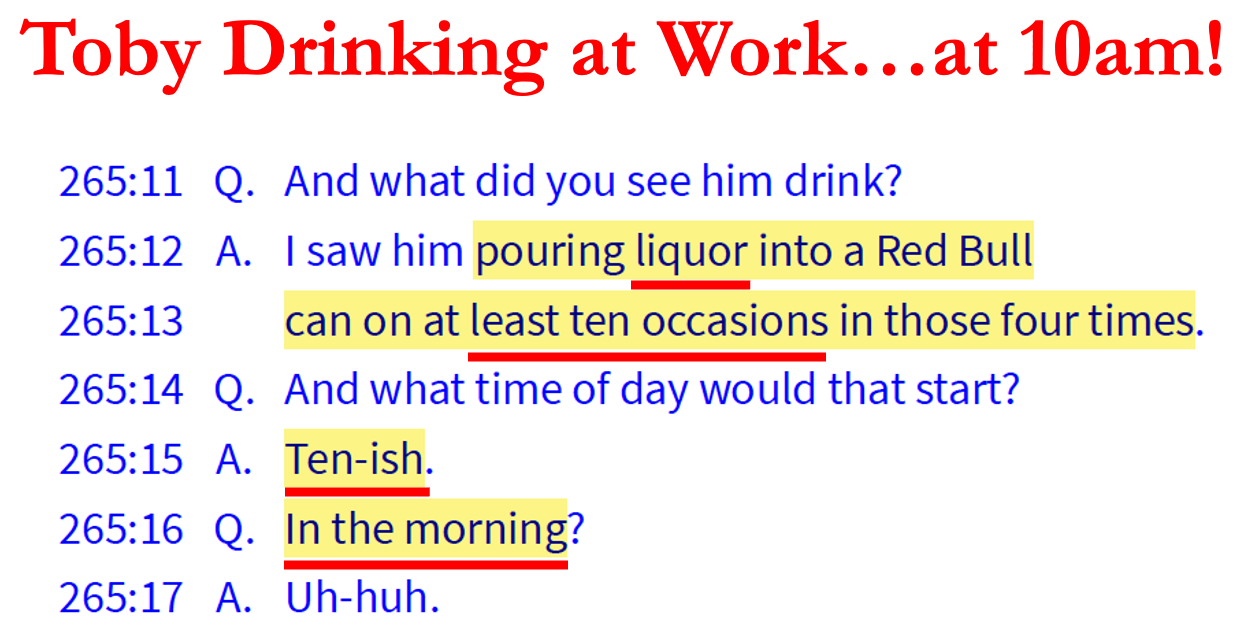

Multiple former employees state that Toby would often drink throughout the workday. Depositions state that somedays Toby would start at 10am. They’d see Toby splash some rum into a red bull or into a diet coke. We are not sure what is sadder. A deposition calling you out for drinking at work at 10am or being a billionaire and still drinking Bacardi superior rum.

- General Note – If you are struggling with drug or alcohol abuse then don’t be ashamed and tell your friends and most importantly get help. Help is available 24/7, it’s even available at 10am on a workday. Call 1-800-662-HELP

- Personal Note – Toby, Barcardi superior, wtf … that’s disgusting! That’s what we drank freshman year of high school. Grow up and have a scotch or an extra anejo tequila like a gentleman.

Shockingly drinking throughout the day resulted in abusive tirades for employees who reported erratic and paranoid behavior.

Drug Use on the Job – Deposition says Toby Used “White Powder” at Work

Apparently, Toby never did a stint in investment banking because he thinks it’s ok to do “white powder” in front of his board members. Come on Toby, keep that to yourself, that is what the Morgan Stanley bathroom is for.

Day Drinking on the Job: Depositions Show Toby Would Start Drinking Alcohol at Work at 10AM

In a deposition a board member admitted said she saw Toby drinking at work on at least 10 occasions. Toby would start drinking at 10am in the morning (pg 119).

The GloriFi’s HR chief, Britt Amos, confirmed this habit and reported to the board that employees reported seeing Toby putting vodka in his red bull in the morning and that she was warned to leave by 6pm because Toby really started drinking “after 5pm Toby starts drinking and things at the house deteriorate quickly.” (pg 17).

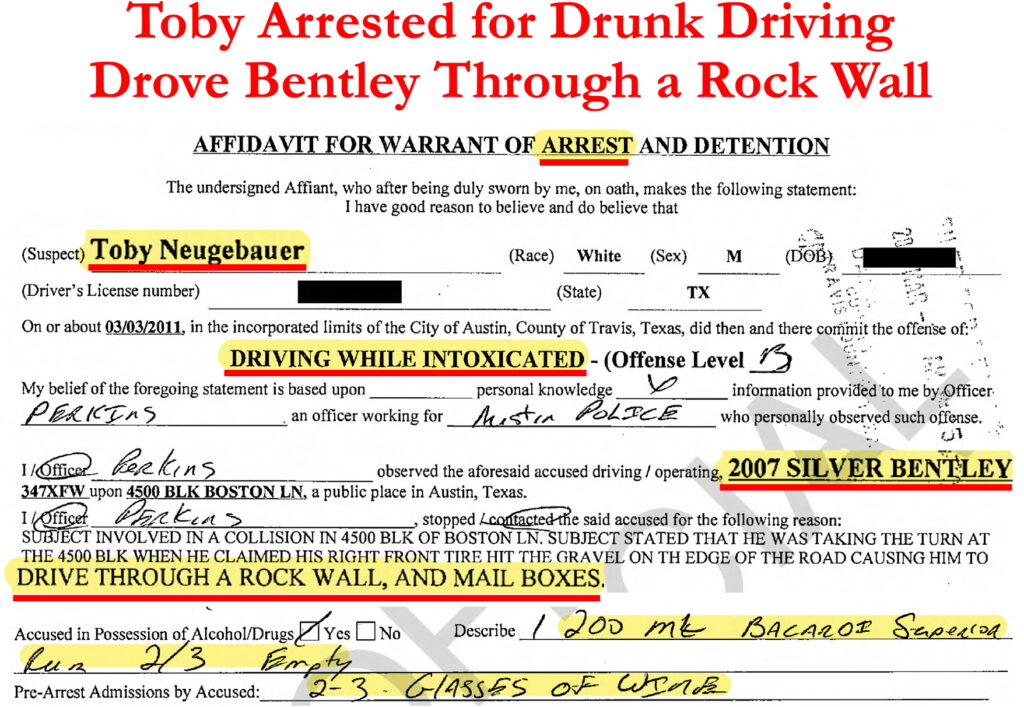

Drinking Off the Job: Toby Arrested After Drove His Bentley into a Rock Wall & Mailboxes while Drunk

We uncovered that Toby was arrested for drunk driving after Toby crashed his Bentley through a rock wall and mailboxes. Toby’s rum of choice for that evening was Bacardi superior according to police reports. We made public records requests to get the Austin, Texas police report. Despite swaying and losing balance, Toby was polite and cooperative.

FoT Charlie Hamilton Testified Toby Often Sees “Black Helicopters”

The trustee describes Neugebauer as having “manic paranoia.” Long-time friend Charlie Hamilton isn’t much nicer. Hamilton testified (pg 36) that Toby “often sees ‘black helicopters’ (meaning Neugebauer sees things that are not there, – i.e., a classic conspiracy theorist).”

Appendix AA – Part Deux – Toby’s alleged Securities Fraud & “Fraudulent Transfers” Fleeced Silicon Valley AI Legends

- Bankruptcy Court Found Millions in “Fraudulent Transfers” to Toby & Associates

- Toby Fleeced the Wrong People:

- Palantir Co-Founders Peter Thiel & Joe Lonsdale

- Former Presidential Candidate Vivek Ramaswamy

- Financial Titans like Ken Griffin

We find it rare for a bankruptcy trustee to accuse a former CEO and a creditor in a bankruptcy. But that’s what happened with Toby Neugebauer in the GloriFi bankruptcy. This isn’t hyperbole from a tort securities lawyer, the bankruptcy trustee accused Toby of “securities fraud,” “egregious self-dealing,” engaging in “lies and deceit,” and alleged he “defrauding” other major investors.

He allegedly backdated debt documents to enrich insiders, including himself, and even allegedly set up a “sweet-heart deal” with a friend to skim money from GloriFi.

The bankruptcy trustee alleges Toby attempted to funnel >$27 million to himself and friends and the company was only operational for 18 months. The problem for Fermi investors is not just Toby’s history of bankruptcy and fraud allegations, but also who allegedly helped Toby with the fraudulent transfers (hint – most of them are on Fermi’s management team today), and who Toby screwed over.

Toby Burned Palantir Founders, Financial Titans and Republican Heavyweights

We think that Fermi investors that are praying for a hyperscaler contract are finding out the hard way that it’s Toby’s turn to “take it” from the billionaires. There is the old Silicon Valley adage … you don’t f—k Peter Thiel (unless he wants you to).

“My family is just gonna take it (the assets) … I am not going to give a bunch of billionaires a free call option.” ~ Toby in a text message

The details we uncovered by pouring through debt documents and interviewing formers go far beyond what has already been reported in the WSJ and elsewhere.

Millions Worth of “Fraudulent Transfers” to Himself

Toby initially fought to have GloriFi go through a chapter 11 bankruptcy rather than a chapter 7 liquidation. Investors fought back because they thought Toby was trying to misappropriate assets. The reason why Toby likely preferred Ch. 11 to Ch. 7 became clear years later after internal business transfers and transactions came to light and were able to be scrutinized by the bankruptcy trustee. The bankruptcy court ruled Toby’s transactions were to be avoided as a “fraudulent transfer.”

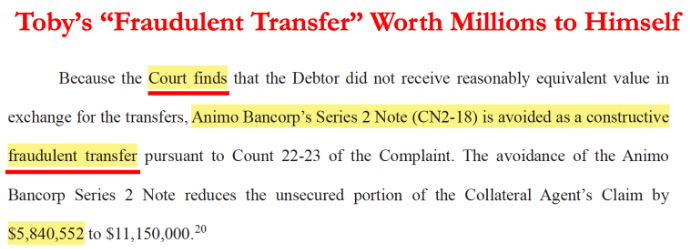

For example, a Toby family-owned entity, Animo Bancorp was on the balance sheet as providing ~$5.8 million of debt but the court found Toby’s entity never made a cash investment matching that amount. Toby essentially gave himself securities.

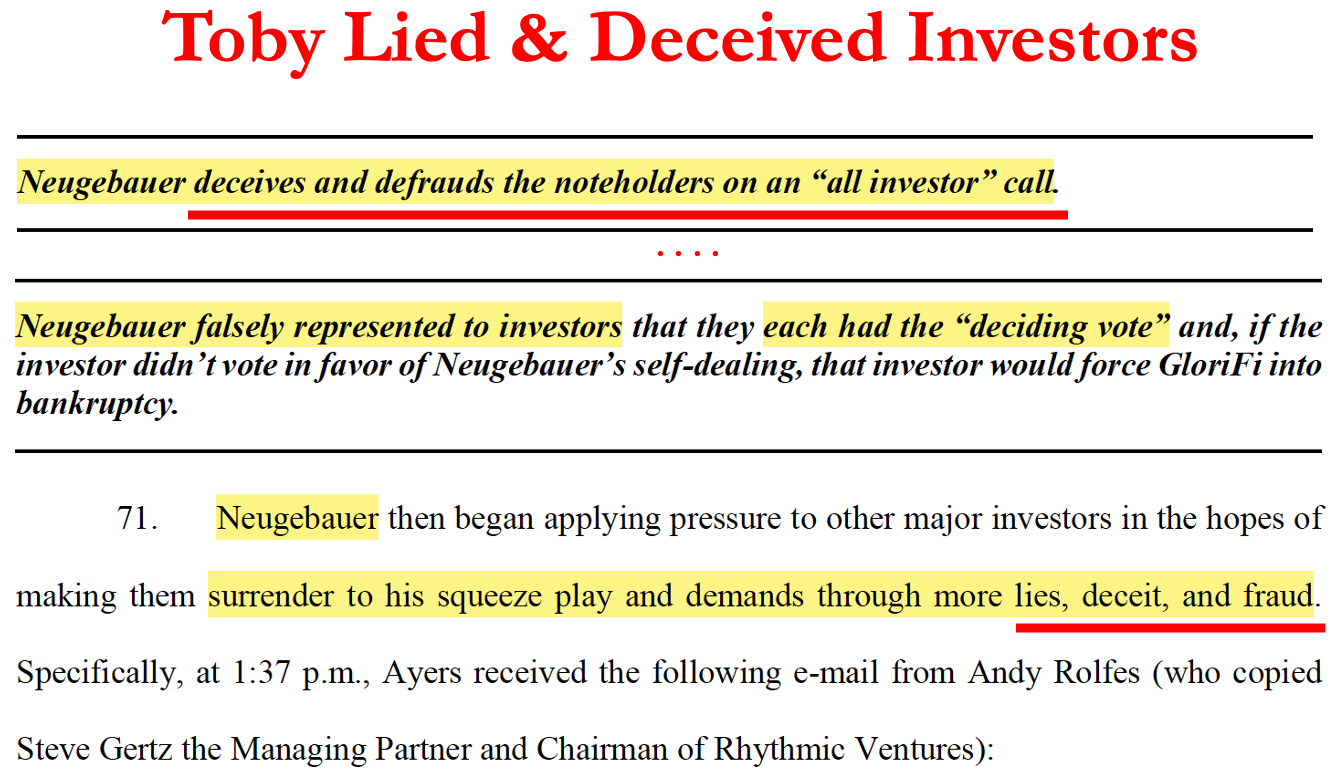

Toby Lied To & Deceived Investors

Anyone who has participated in a Fermi Earnings Call or spoken to Toby 1×1 is probably not surprised to hear that at GloriFi, Toby was accused of having lied to and deceived investors. Getting a hyperscaler contract is the easy part…hmm well why don’t you have one anymore Toby?

Toby accused of Misappropriating Assets & Intellectual Property via Alleged “Fraudulent Backdating” of Debt

As GloriFi was failing Toby admitted that in phone calls, texts and emails that he wanted to misappropriate the tech stack (GloriFi’s most valuable asset for) for himself. Toby said “I think my family is just gonna take it.”

Source: Seidel v. Neugebauer, Doc 1, pg. 12

Legal docs state that Toby then engaged in “fraudulent backdating” of debt agreements in order to attempt to control the company’s technology in bankruptcy. Debt agreements with were signed on dates in October & November 2022 yet the debt issue date was backdated to dates months early (like May & June of 2022)

Source: Seidel v. Neugebauer, Doc 1, pg. 34

More Appendix AA – Why Toby’s Volatile Background Matters?!? Yelling at Investors & Howard Lutnick

Toby Yelling on Fermi Investor Calls

On Dec 12 the day of announcing losing the hyperscaler LOI. Toby had two back-to-back sell-side 30-minute Zoom calls schedule to explain the loss of the most important part of his business.

- Sell-side call one (Evercore) started on time and was ok, not great.

- Sell-side call two (UBS) began 5-10 min late, and Toby showed up with new accessory, a large coffee mug.

Toby took slow sips out of the mug throughout the call and then about 10-15 min into the call Toby began to shout and act erratic. Then Toby started yelling at everyone

(Toby Yelling) “if Fermi was weak, we would’ve done the deal. For me personally it was billions of dollars. So if we were weak, we would have just said yes. But we didn’t.

~Toby Neugebauer”

We wonder what was actually inside Toby’s coffee mug, that caused him to start yelling.

Toby’s Also Yelled at US Commerce Secretary Howard Lutnick – His Antics Annoyed Lutnick & Other Gov’t Officials

Toby was counting on his Trump World ties to attract investors and AI hyperscalers to Fermi. But even before his outburst last month at the Commerce Secretary, Toby had irked Lutnick, advertising Fermi’s ties to the Commerce Secretary’s kids to The New York Times in November.

“Did he think that New York Times piece was good for him? Does he think it helps to make it look like he’s in some kind of quid-pro-quo with the secretary’s family? Because he’s not”

~ senior Commerce Department official B

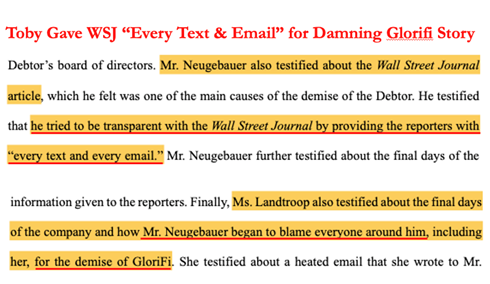

Toby Exposed Himself – Toby was the Key Source for his own WSJ Expose

After an October 2022 expose in The Wall Street Journal, “How a New Anti-Woke Bank Stumbled,” helped seal Glorifi’s demise, Toby blamed the paper for killing the company, according to former employees cited in the legal filings.

But it was Toby who loaded the gun – he provided the WSJ with “every text and email,” according to court records. Yet despite Toby’s “propaganda” his “fairytale [is] ever-changing and completely bereft of evidentiary support.”

Appendix – Toby’s Taxes? — Is Avoidance of US Federal Taxes Patriotic?

- Toby & Charlie Hamilton Became Puerto Rico Residents to Avoid US Federal Taxes

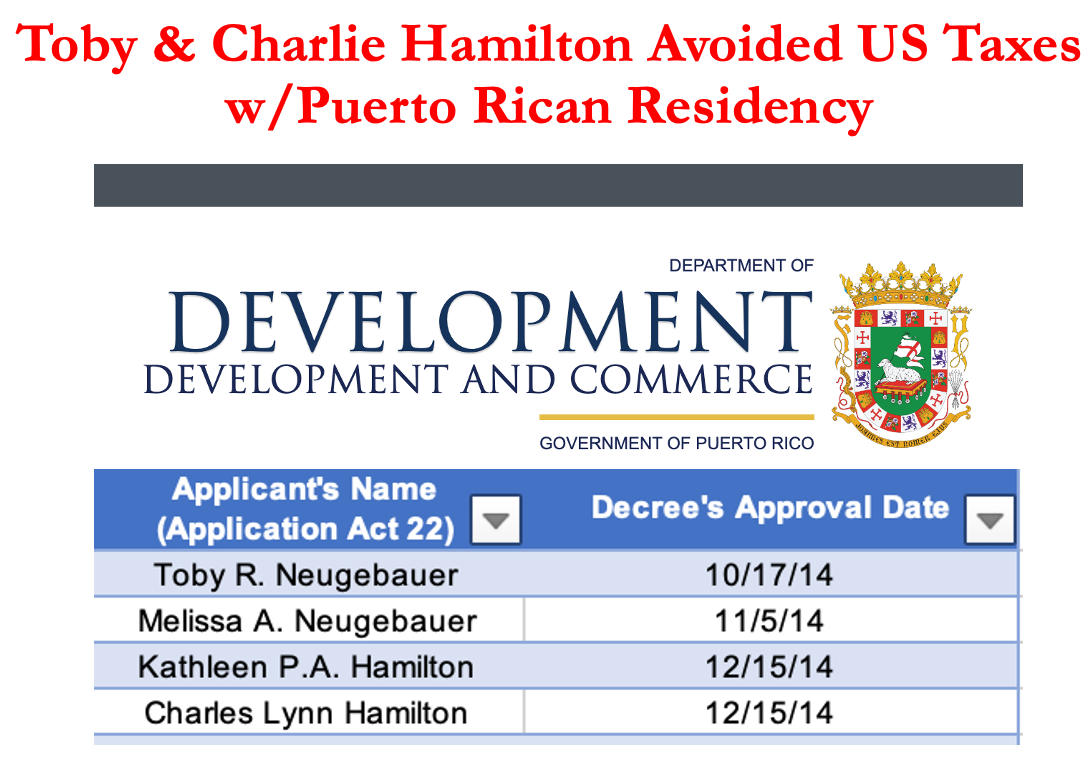

Toby Neugebauer says he is all about America, Toby even built a mansion that is a replica of the ‘White House.” Toby claims the government is going to help Fermi get investment. However, we uncovered that Toby likely stopped paying US federal taxes long ago. In 2014, Toby became a Puerto Rico resident reportedly in order to pay no federal income or capital gains taxes.

Toby is not the only Fermi executive that stopped paying US federal taxes. Charlie Hamilton also became a Puerto Rican resident.