- Spent 2.5x More on Stock Promotions Than on Operating Oil & Gas Wells

- CEO’s Shady Past: ~20 Years Running Pink Sheet Co’s into the Ground with Paid Stock Promos

- Former Colleagues Call Him a “Great Bullshitter” Who “Doesn’t Execute” & “Wouldn’t Trust My Money with Him”

- Related Party Enrichment – Free Assets & Cash for Insiders

- AI Data Center Narrative is a Fantasy:

- 40+ Yr Old Wells Only Produce 5% of Required Gas

- No Customers, No Permits, No Financing

We are short New Era Energy & Digital ($NUAI), a purported AI data center play whose stock ran up >20x after it began a massive paid stock promotion campaign in September, and that is set to end soon. The company originally came public as New Era Helium (NEHC) via a 2024 Roth SPAC, and we could find only 4 employees on LinkedIn. So shorting NUAI is essentially a bet against its CEO, E. Will Gray II, and its old gas wells, which a 3rd party study deemed uneconomic. We uncovered that Gray has a long history (~20 years) of incinerating value at oil & gas pink sheet companies. In fact, Gray was first accused of securities fraud back in 2007. The story of each Gray-led public company is basically the same: sketchy related party dealings, false promises and paid stock promotion often using the same promoters. And each time, retail investors lost big — on average, Gray’s companies DECLINE -98%.

We are short NUAI because we believe it is Gray’s next flameout. New Era started off 2025 as a helium company where Gray pitched investors he would extract helium from old gas wells. He failed, so Gray changed the company’s name and added the letters “AI” to the stock ticker. NUAI’s stock popped 20x only after Gray began its >$1 million stock promotion campaign to push the fantasy that the company’s 40+ year old deteriorating & money losing gas wells can power the AI revolution. Clearly, insiders disagreed as the CFO and 3 out of 4 independent board members quit.

NUAI’s old gas wells DO NOT have the production necessary to power even ~5% of its announced plans. But, more important, Gray’s company lacks all the other ingredients it needs to succeed. We pulled public records and obtained satellite images that show it has no permits and no development. We uncovered related parties siphoning off assets and found that insiders have registered to sell all their shares.

- CEO E. Will Gray II has a colorful 20+ Year History of Multiple Penny Stocks

- Shareholder’s wipeouts – 4 past company’s Gray was CEO of declined by >98%

- Gray faced past allegations of securities fraud.

- History of sketchy related party transactions, insider dealing – news organization ProPublica even exposed fees paid to friends & family at one of Gray’s companies

- Gray frequently used paid stock promoters including RedChip & Proactive Investors

- Interviews of recent former colleagues of Gray’s said he’s a “Great Bullshitter” and “Talks Big” but “Doesn’t Deliver”

- Gray using the same paid stock promotion + toxic financing playbook at NUAI

- NUAI spent 2.5x more on paid stock promotion than on costs operating wells.

- Gray using the same stock promoters that he did before – RedChip & Proactive Investors

- Largest paid stock promotion set to end Dec 13. What happens then?

- Toxic death spiral financing – share count has increased by >300%

- Suspicious Related Party Transactions – NUAI’s Unrelated Loans to Related parties

- “Loaned” ~30% of the Co’s cash ($4 million) to former chairman & Gray’s business partner, Joel Solis, with no explanation

- Loan only Secured by property worth ~$1.3 million

- Zero cash recovered from another ~$1 million related party loan to Solis — settled for a royalty Gray valued himself & NUAI still took a six-figure loss

- A real bank, Wells Fargo, accused Solis of “diverting and misappropriating funds” after he defaulted on a $5 million loan & declared bankruptcy.

- NUAI also gave Solis “free assets” as a gift was for “past contributions to the company.”

- “Loaned” ~30% of the Co’s cash ($4 million) to former chairman & Gray’s business partner, Joel Solis, with no explanation

- Suspect New Mexico Land Deal – NUAI Paying $70 Million for land assessed at $28k

- Seller “Coincidently” owns other land Where New Era Has Gas Wells

- Seller also “Coincidentally” appears to own land where NUAI’s Helium Plant

- NUAI Paid >750% More Per Acre for Roswell, NM Land than Tom Ford’s Santa Fe Ranch sold for. E. Will Gray II is no Tom Ford.

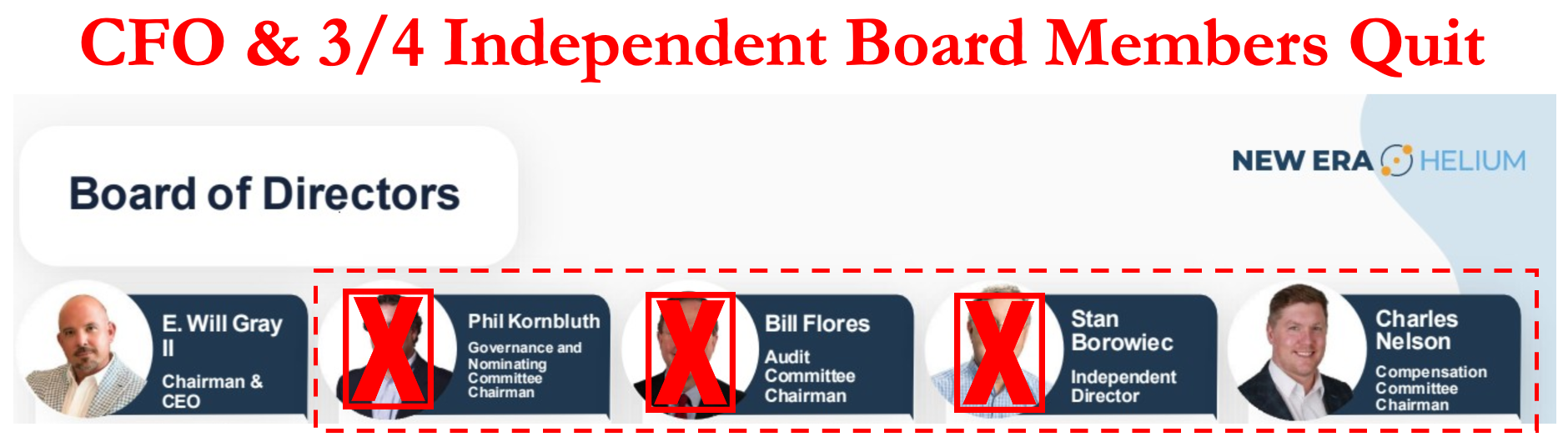

- CFO & 3 out of 4 Independent Board Members Quit Last Spring

- NUAI Has Bad Gas Wells – Old Wells can only produce ~5% of what Co’s plans call for

- 3rd Party appraisal shows wells value is a NEGATIVE NPV

- Would Require ~$370 million of Capex to Develop

- Lost ~$1,600/well in 2024

- 87 Wells came from a past company Gray drove into Bankruptcy

- Wells Exposed by ProPublica – described as “The Industry Dregs” & “Deteriorated”

- 3rd Party appraisal shows wells value is a NEGATIVE NPV

- Gray’s Data Center Plan is More Decrepit Than NUAI’s Aging Gas Wells

- No Permits Filed

- No Guaranteed Financing

- No Data Center Engineers & No Open Job Listings Found

- Announced deals are worthless pieces of paper – non-binding MOU’s with recently formed companies that lack experience.

- JV Partner in Texas Project, Sharon AI, is another reason to short NUAI

- Sharon is an Australian company built off a related-party transaction

- Sharon is a Roth Reverse Merger that met NUAI, a Roth SPAC, via … Roth

- Satellite images reveal empty brush where Gray promised a Plant Should Be

- Helium customers bailed & NUAI doesn’t have $45 million needed to finish the project

- “Going Concern Notice” & Admitted “Ineffective” Financial Controls in latest 10-Q

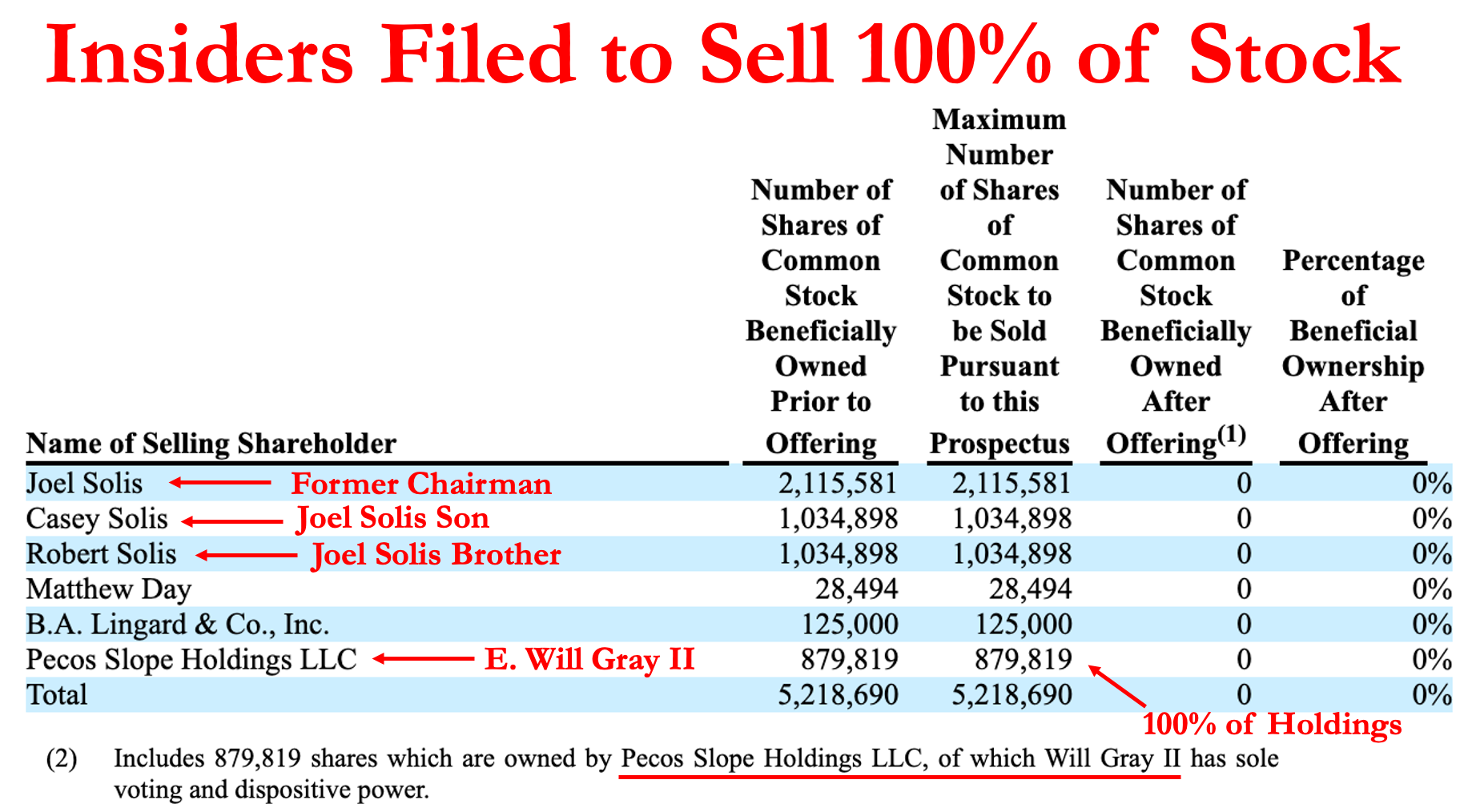

- Insiders have filed to sell 100% of their shares

We are short NUAI because it’s not a new era — it’s the same story as Gray’s past failed ventures.

Read on to learn more about Gray’s History running Penny Stocks and Paid Stock Promotes into the Ground … aka the “Fifty Shades of Gray.”

We are short NUAI and think investors probably need a safe word even more than a stop loss to protect them from Gray’s history of value destruction.

Fuzzy Panda Research is Short New Era Energy & Digital (NUAI)

Fuzzy Panda Research and Fuzzy Panda “Affiliates” are short securities of New Era Energy & Digital (NUAI). Please see additional disclosures at the end of report and in our terms of service.

PART I – Short New Era Energy & Digital

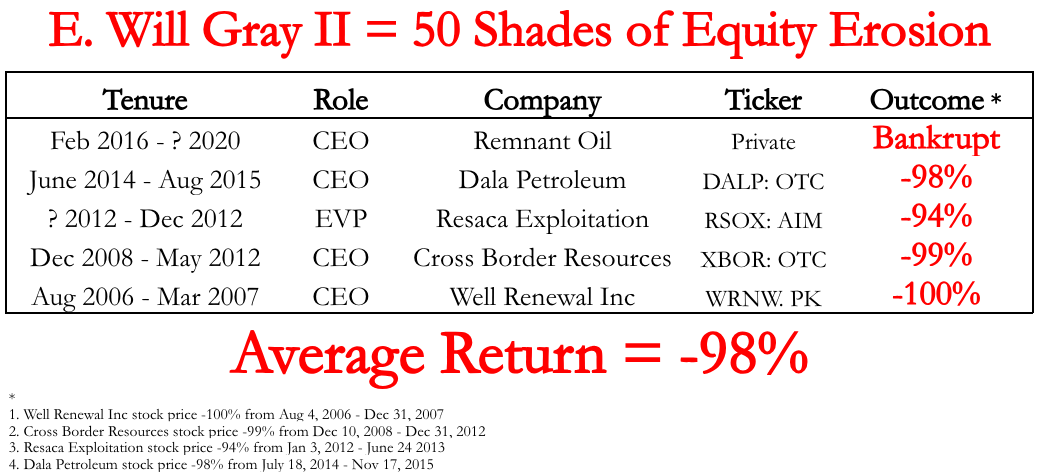

CEO’s History – “Fifty Shades of Gray’s Equity Erosion” – Pink Sheet Co’s & Paid Stock Promos

- Colleagues Call Gray a “Great Bullshitter” Who “Talks Big” But “Doesn’t Execute”

- Will Gray Has 20 Year History of Penny Stocks Implosions, Paid Stock Promotion & Accusations of Securities Fraud

- Gray’s Past Pink Sheet Co’s Down on Average -98%

A bet on New Era Energy (NUAI) is a bet on E. Will Gray II, so it’s important to understand that Gray is NOT the successful visionary oil & gas entrepreneur he pretends to be. The reality is that Gray started as a medical device sales rep before pivoting to a long career as a pink-sheets CEO who pushes dreams of oil & gas riches to retail investors. Gray was first accused of securities fraud back in 2007, and his career since has been filled with penny stock implosions that regularly engaged in paid stock promotion and suspicious related party dealings. We uncovered that Gray’s playbook includes financial tricks to enrich insiders, like converting related party loans to equity or paying fees to friends and family.

Gray has incinerated value at multiple pink sheet oil & gas companies where he previously served as CEO. Gray tries to hide the painful truth of what actually happens to investors that owned one of his past paid stock promos. But we uncovered the truth, and we are calling it the “Fifty Shades of Gray.”

Each time, investors’ portfolios got spanked with reality, and they lost their shirts. Investing in a company with E. Will Gray II as CEO lost investors an average of –98%.

Gray’s History of Equity Erosion

The results from Gray’s stints as CEO are eerily consistent: Gray makes money while investors get drilled.

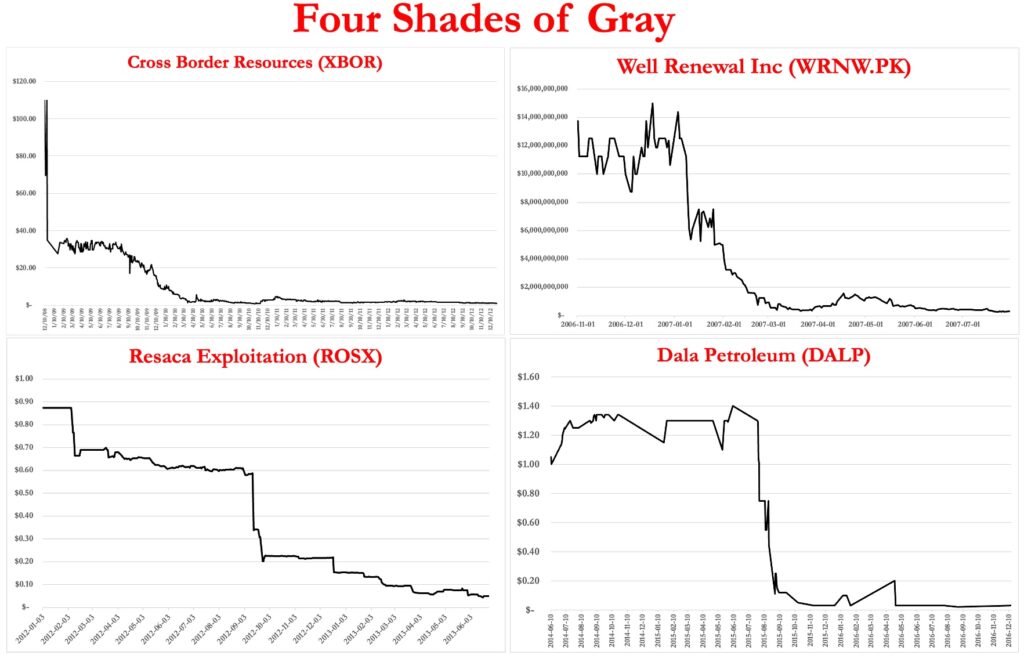

- Remnant Oil (private) = Bankruptcy + Related Party Payments – Gray was Co-Founder & CEO of Remnant Oil, a private co, which went bankrupt in 2019 after hundreds of “regulatory violations.” ProPublica uncovered Remnant “paid hundreds of thousands of dollars in consulting fees” to related parties owned by management. Remnant’s “deteriorated wells” were described as the “industry dregs,” so naturally they were acquired in bankruptcy by a related party, Acacia Resources, and were then sold to Solis Partners, a subsidiary of New Era Energy (NUAI).

- Dala Petroleum (DALP:OTC) = Pink Sheets Reverse Merger –98% – Gray was CEO of Dala Petroleum & this pink-sheet stock declined -97% from peak before another co reverse merged into it. Before it ceased to exist Dala was #3 on a list of Texas’s 13 most distressed energy companies.

- Resaca Exploitation (RSOX:AIM) = –94% + Paid Stock Promotion – Gray only served as EVP & head of capital markets but shareholders got decimated just like at Gray’s other companies. Before it liquidated in 2012, disclosures indicate Resaca paid Proactive Investors for stock promotion.

- Cross Border Resources (XBOR:OTC) = Pink Sheets + Paid Stock Promotion –100% – Cross Border was another pink sheets, paid stock promotion that Gray ran into the ground (literally, as it was a failed oil & gas wells company). Like at NUAI, Gray used RedChip to promote the stock. XBOR declined -98% during Gray’s tenure as CEO, and it currently trades for $0.0001 — on the rare occasion the stock even trades.

- Well Renewal Inc (WRNW.PK) = Pink Sheets Reverse Merger –100% – E. Will Gray II co-founded this pink sheets penny stock with his father, and it went public via reverse merger. The company defaulted and lost its Oklahoma assets. The company and Gray II were sued by an investor. Their complaint made allegations[1] of securities fraud and making fraudulent transfers.

Formers Say They “Wouldn’t Trust” Their Money with Gray

“He’s a Great Bullshitter”

We spoke with some of Gray’s former colleagues who are familiar with NUAI. They told us they would NOT bet on Will and “I wouldn’t trust my money with him.”

Gray is “a great bullshitter … he talks big. But he doesn’t play big” ~ Former Colleague A

They said he sells you his “outgoing personality” but “he can’t get it done.”

“Don’t make it a personal bet on Will Gray because he sold you with his outgoing personality … he’s got the gift of gab, and he can present himself pretty well. But don’t make it a personal bet on Will” ~ Former Colleague B

Gray Lacks Focus, Gets Distracted by “Shiny Pennies” & “Doesn’t Execute”

Recent former colleagues of Gray told us that Gray can’t execute on his plans because he gets distracted by new shiny pennies. That’s especially ironic because companies he has led often end up trading for pennies.

“[Will Gray II] doesn’t execute. He needs people around him to make his plans come true.” ~ Former Colleague A

Former colleagues blamed New Era’s helium failure on Gray’s lack of focus. He was always chasing “shiny new things,” which is how New Era’s helium plans evaporated into … AI data centers?!?

“Every day there was a new shiny penny that distracted him. And one of those shiny pennies was the data center stuff” ~ Former Colleague B

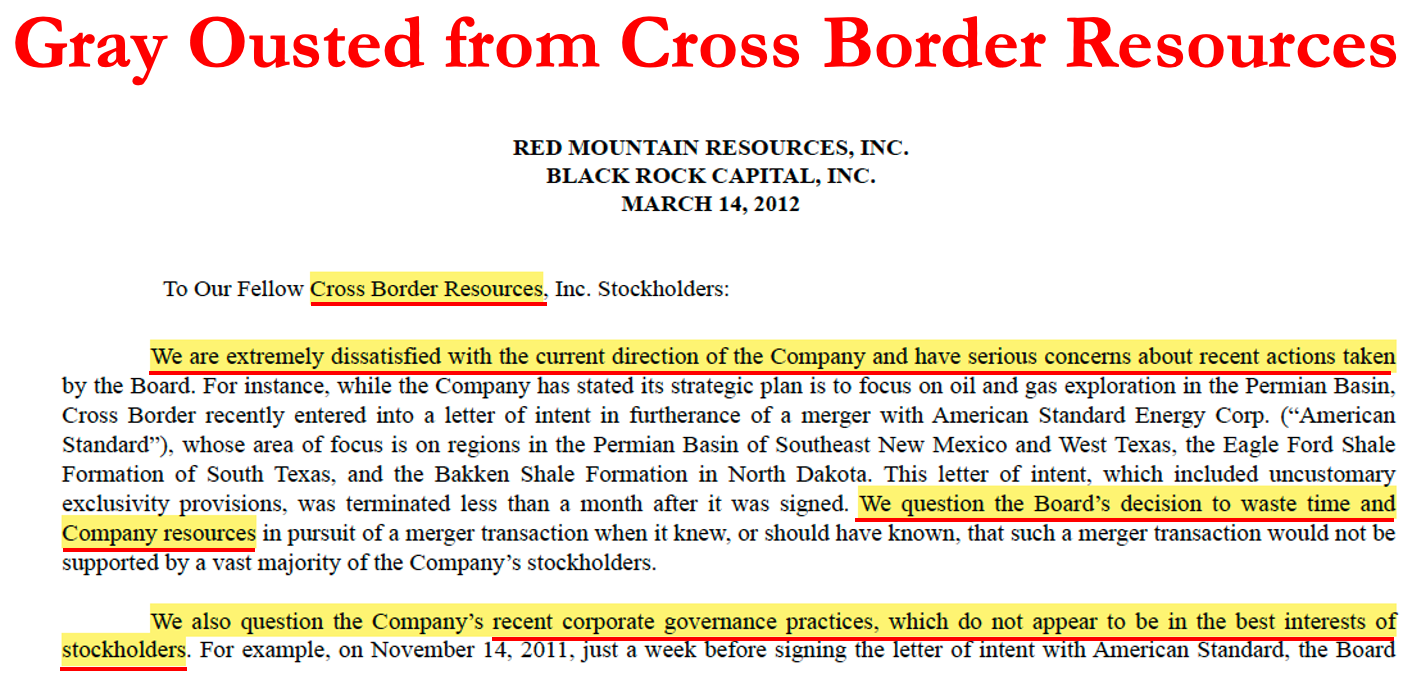

Gray Fired at Previous Public Co. For Wasting Time & Money & Attempting to “Disenfranchise Shareholders”

Gray was forced out as CEO of Cross Border Resources in 2012 by an activist investor who said it was “extremely dissatisfied” with the company’s direction after a failed merger proposal that was a “waste of company time and resources.”

The activist investor, Red Mountain Resources, also raised concerns over “corporate governance” problems that it said was an attempt to “disenfranchise stockholders and entrench the current Board members.”

PART II – Short New Era Energy & Digital

Paid Stock Promotion & Toxic Financing – NUAI Spent More Promoting Stock Than Operating Wells

- Spent >$1 million on Paid Stock Promotion v. Est ~434k Operating Wells Over Last 4 Months

- Stock Promotion Set to End This Week

- NUAI’s Toxic Death Spiral Financing Boosted Share Count >300%

You can’t build data centers with paid stock promotion and press releases. NUAI has spent more on stock promotion this year (>$1 million) than it did on costs to operate its wells (~980k in first 9 months).

Gray has a history of paid stock promotion at other penny stocks that he was involved with. Gray paid for stock promotion via Red Chip at Cross Border Resources (XBOR) back in 2012, and we found his next company, Resaca, using Proactive Investors.

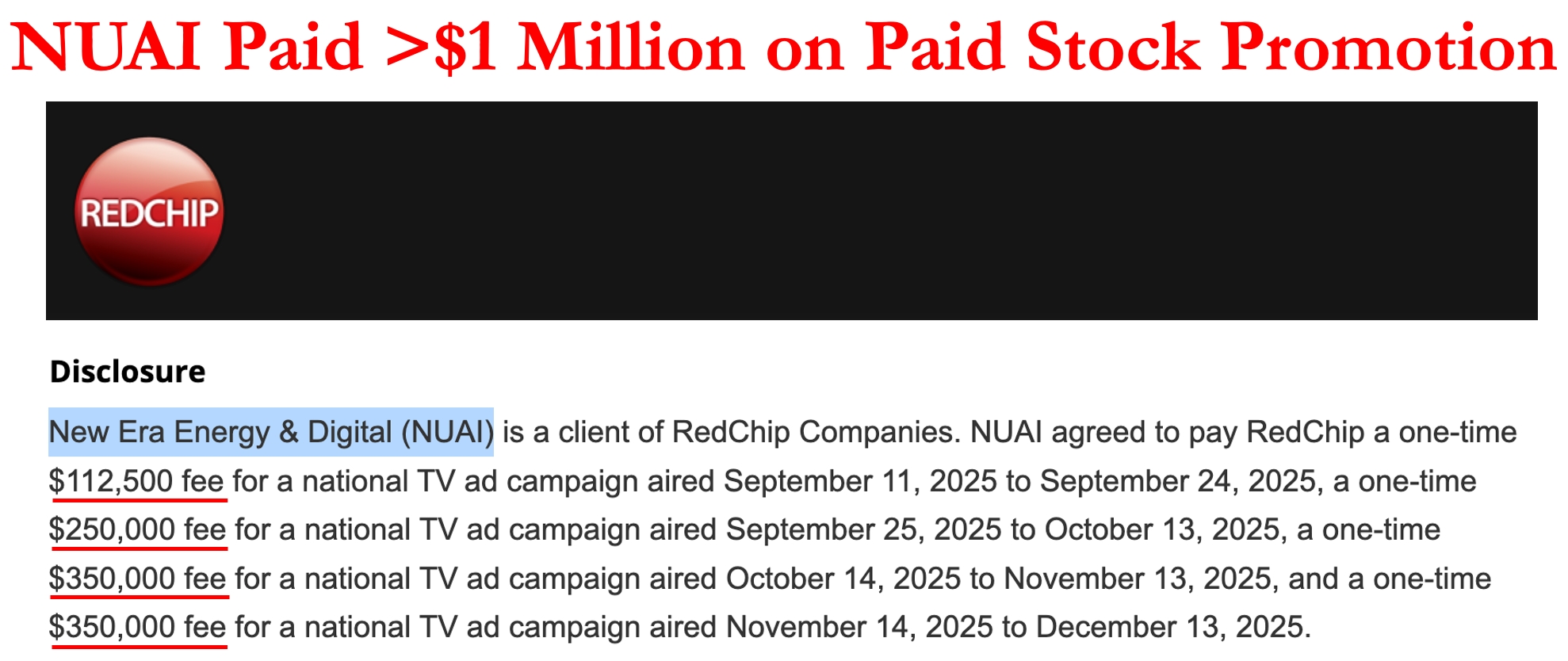

Gray turned on the stock promotion spigot for NUAI this September in a major way. Since September, NUAI has already spent >$1 million on paid stock promotion.

RedChip – Large Paid Stock Promotion Set to End December 13

The >$1 million campaign through RedChip ends later this week — what is going to happen then?

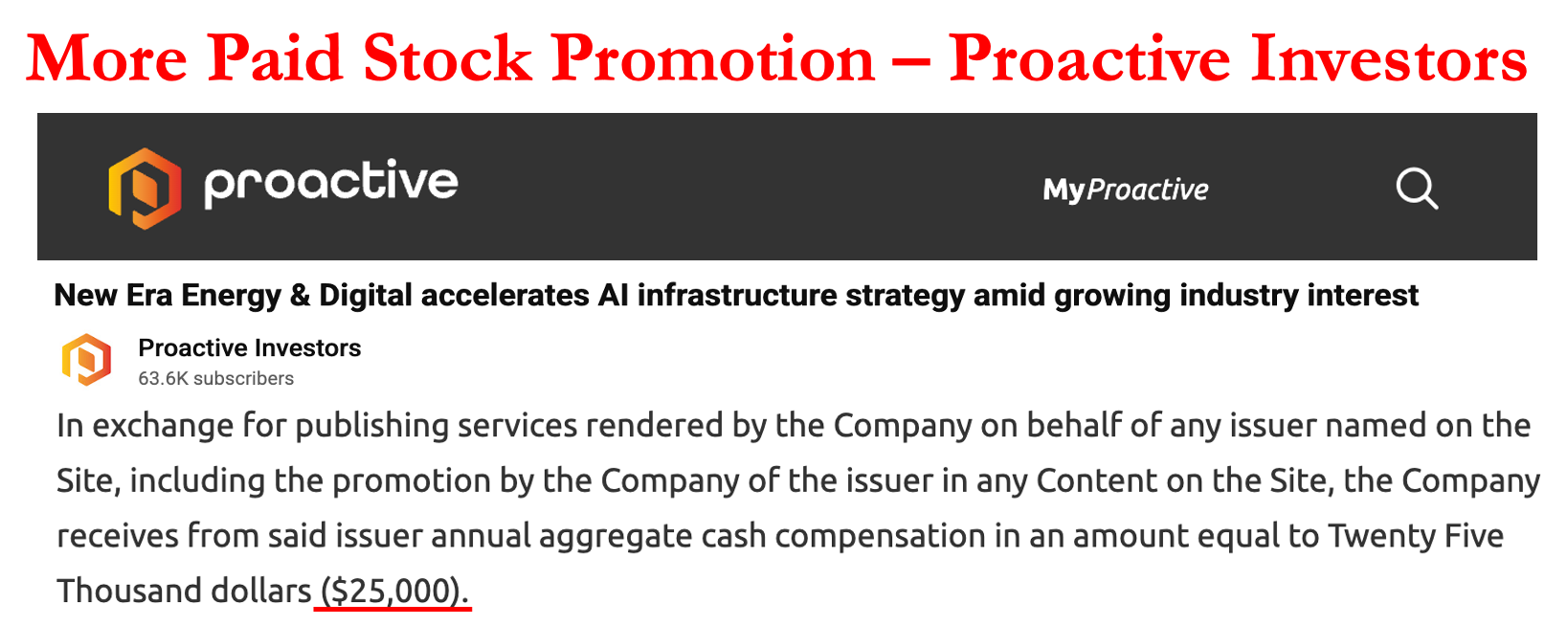

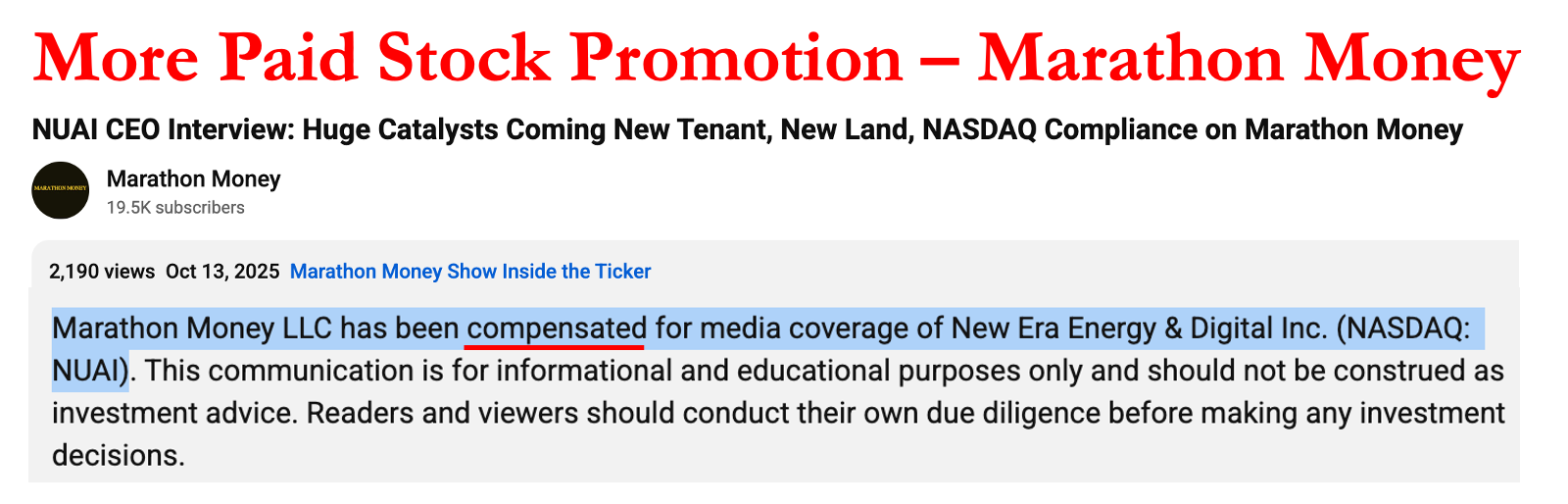

More Paid Stock Promotion: Proactive Investors & Marathon Money

NAUI also recently ran paid stock promotion campaigns through Proactive Investors – a platform Gray’s past company’s Resaca and Remnant Oil & Gas were featured on.

They have also paid Marathon Money for stock promotion although the amount paid is not disclosed.

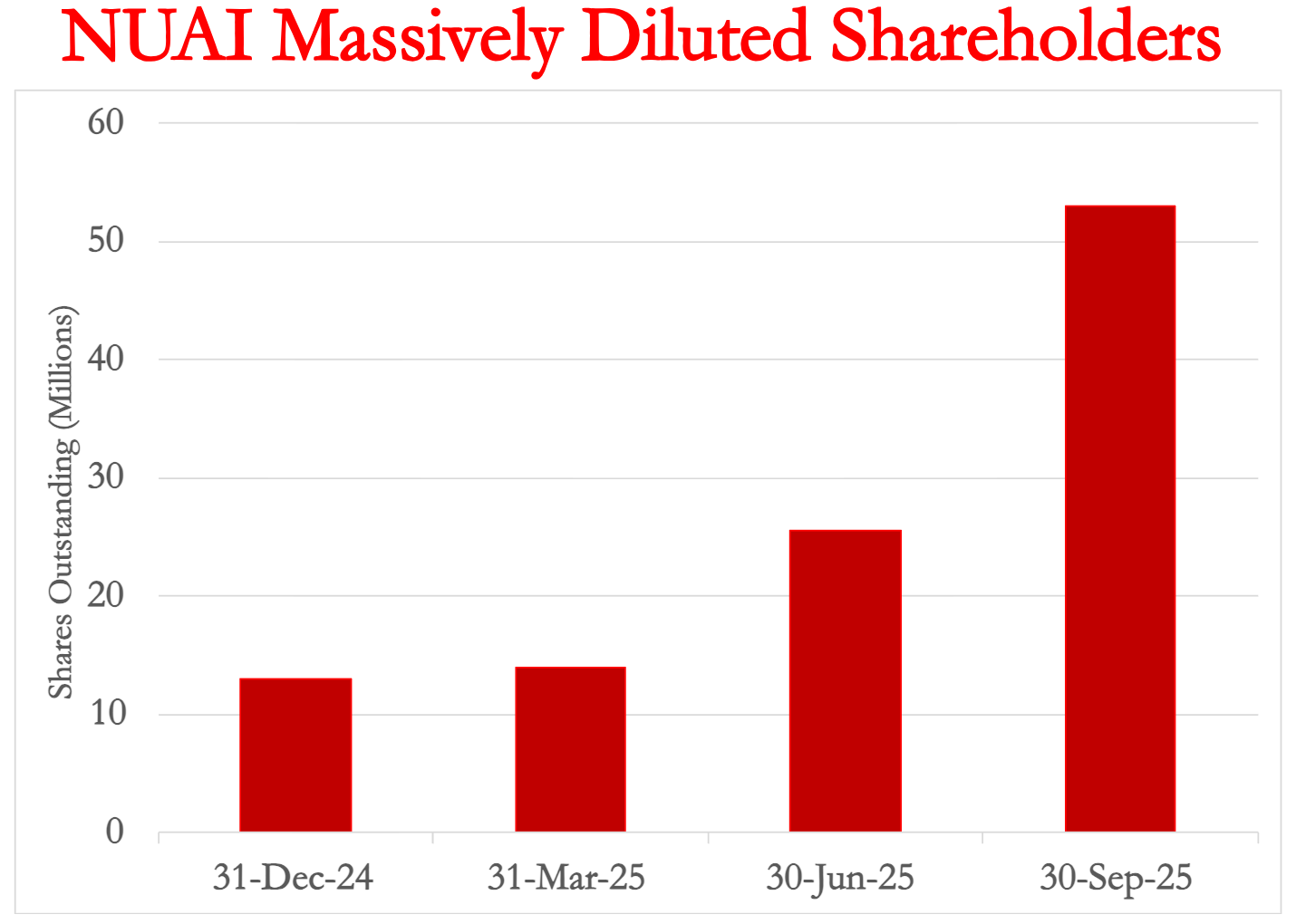

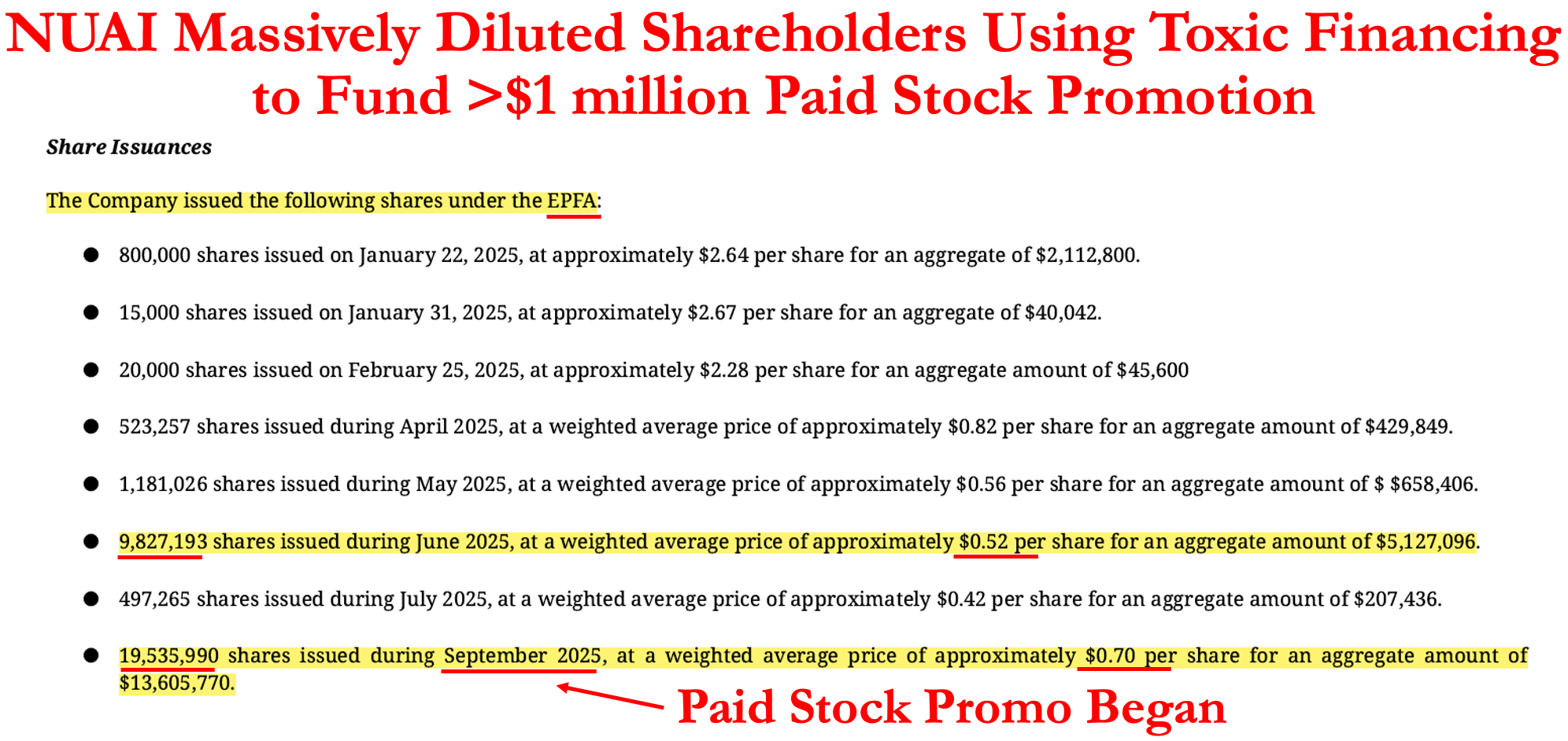

Toxic Death Spiral Financing – Share Count Increased by >300%

After the CFO and most of the board quit, NUAI massively diluted shareholders via its toxic death spiral financing to solve a desperate cash crunch. Then it used funds it raised to pay for stock promotion.

Death spiral financing allows the lender to buy stock at a guaranteed discount and sell it at market prices, allowing the lender to make money as the stock price falls. It’s a toxic cycle that leads to massive dilution and selling pressure.

This is exactly what Gray did to existing NUAI shareholders by massively diluting shareholders near stock price lows through their equity purchase facility agreement (EPFA). Shares outstanding ballooned >300% so far this year.

The toxic financing facility was terminated at the end of October but was followed up with a registration statement allowing insiders to sell 100% of their shares just weeks later.

PART III – Short New Era Energy & Digital

NUAI’s Assets Are Disappearing into Pockets of Formers & Related Parties

- Assets Vanishing Faster than NUAI’s Helium Hot Air

- Free Money to Former Co-Founder by Forgiving Loans

- Assets Given Away to Entity Controlled by Wife & Kids of Related Parties

Similar to many other paid stock promotions we have uncovered, NUAI is transferring assets to related parties. This year alone, New Era has spent nearly 3x more on a loan to co-founder Joel Solis ($4 million) than it has on capex (~$1.3 million).

Related Party Loans for Completely Unrelated Projects – Why Has NUAI’s Cash Become a Piggy Bank for Related Parties?

We uncovered that NUAI appears to be a personal piggybank for related parties. NUAI gave former chairman, Joel Solis’s entity, Aventus Properties LLC, a $4 million loan in October.

NUAI has not disclosed the reason for the loan. But it was secured by a bleak industrial yard and a barren dusty lot that county assessments (1, 2) say are only worth~$1.3 million. The loan was due Dec. 6.

- Would a normal bank not make Solis a loan?

- Why are related parties able to use NUAI’s cash as a personal piggy bank?

Past Related Party Loans Weren’t Repaid with Cash – Bad for Shareholders but Free Money for Related Parties!

New Era also previously gave a ~$1 million related-party loan to Solis’s Melius Energy LLC without saying when or why. Instead of having to repay the loan, Solis gave NUAI a royalty worth ~$316,00 LESS than the loan value. Essentially, a related party got free cash!

Maybe this is a good time to remind you that Gray is the CEO and CFO and that NUAI has an unknown auditor.

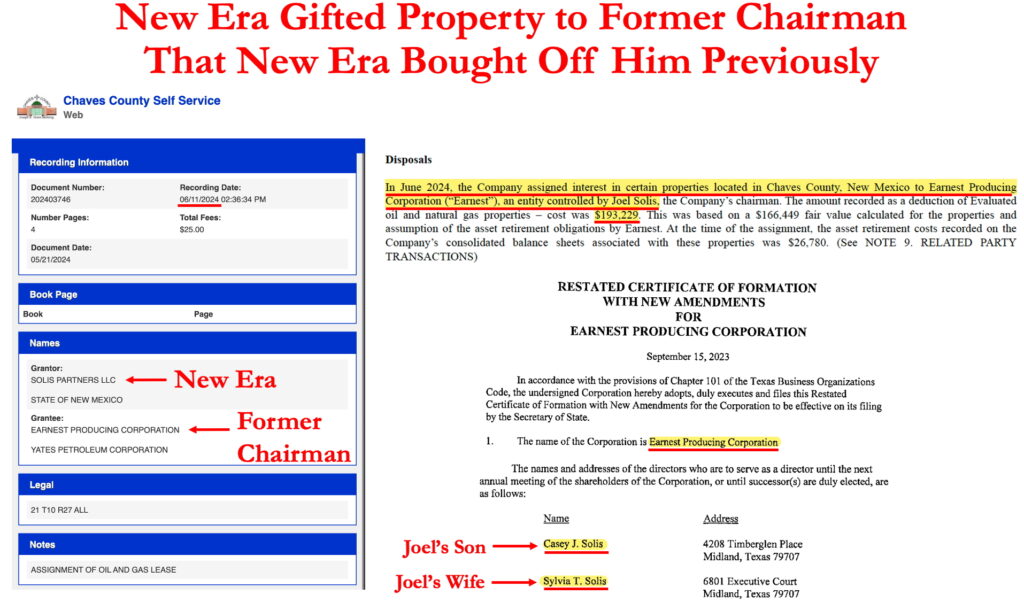

Paid Related Party for Assets & Then Gave it Back to Them for Free

It’s good to be a related party with NUAI. They will give you back assets for free that they already once paid you for, and then say the give-away is for your “past contributions to the company.”

It’s like Oprah — you get assets! you get assets! you get assets! — except “you” means only Joel Solis.

NUAI was founded by buying Solis’ company, Solis Partners, in 2023 for 5 million shares, which ended being worth ~$50 million at deSPAC. Solis also served as chairman until the deSPAC, and when he stepped down, NUAI gave him back ~$193,000 of the property that it acquired from Solis Partners.

New Era said it gift was for Solis’ “past contributions to the company.”

New Era Paid Another Solis Company >$720,000 for “Consulting”

In July 2024, NUAI issued Joel’s entity, Tall City Well Services, a secured convertible note for $720,000 plus 10% interest in exchange for equipment and consulting. New Era has not exactly said what kind of consulting it is getting from Tall City.

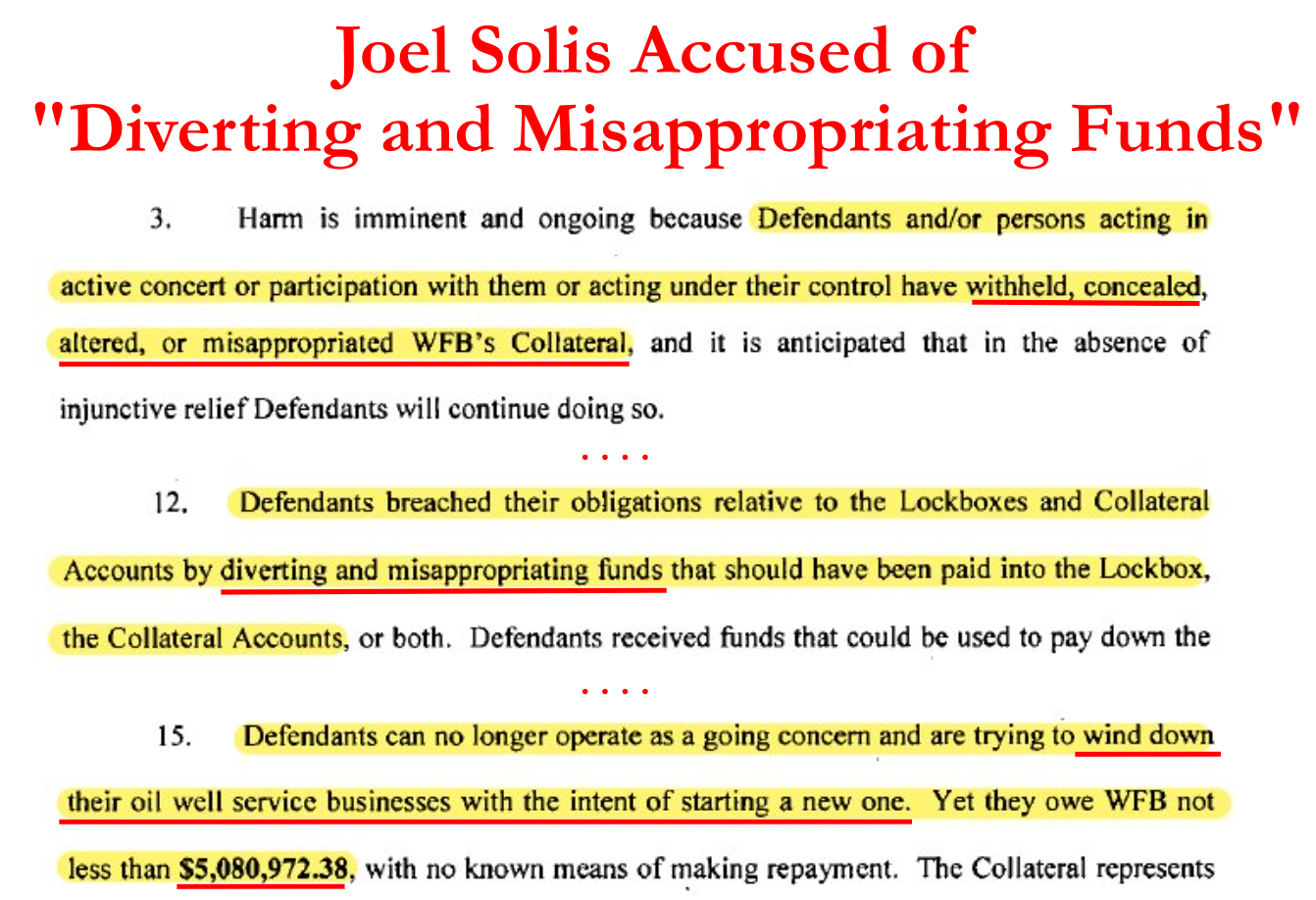

Wells Fargo Sued Solis for “Diverting & Misappropriating Funds” After Defaulting on $5 million Loan

Wells Fargo accused Joel Solis and three of his other companies of “diverting and misappropriating funds” and defaulting on a $5 million loan in May 2016. It appears Solis potentially avoided additional litigation by filing for personal bankruptcy the following month. Filings showed he had >$50,000 in assets and $10-50 million in liabilities.

PART IV – Short New Era Energy & Digital

Breaking Bad – Suspiciously Overpaying $70 Million for Land Assessed at $28k Near Roswell, NM

- Land Seller “Coincidently” Owns Other Land Where New Era Has Gas Wells

- Appears that “Coincidentally” the Helium Plant Site Is Also on the Same Seller’s Land

- NUAI Paid >750% More Per Acre for Roswell, NM Land than Tom Ford Sold His Santa Fe Ranch For

New Era struck a “land option purchase agreement” to acquire ~3,500 acres of land in New Mexico for $70 million in November. The land is for planned 7GW data center campus and the price appears wildly inflated: The most recent tax assessment valued the land at $28k. Recent comparable land deals show NUAI paid 750% to 8850% above recent prices.

Unsurprisingly, the seller, Benjamin Pearce has multiple other connections to New Era. Benjamin Pearce of Pearce Land & Cattle also owns a company called Buckeye Water, which drills water wells.

- New Era has eight gas wells in New Mexico on land owned by Pearce.

- New Era’s helium plant site also appears to be on land owned by Pearce.[2]

This $70-millon land deal is near Roswell, NM — the middle of nowhere, except if you want to see where people claim aliens landed. For the price NUAI is paying, the land better have both aliens and a stash of Breaking Bad’s meth hidden on it.

NUAI Buying New Mexico Scrub Brush for Prices Way Above Comps – 8,500% Above a Recent Large Land Deal – Even 750% More Than the Cost of Tom Ford’s Stunning Ranch

NUAI’s $70-million land deal with that same suspiciously connected seller, Pearce, looks like a ‘bad break’ for shareholders when you line it up against comparable New Mexico land sales.

- New Era’s Data Center Site = ~$19,800/acre

- Undeveloped, sparsely populated region except for maybe the aliens

- Great Western Ranch = $228/acre

- Largest land sale in NM history, ~504k acres sold for $115 million in August 2025

The price looks even more absurd when you see that NUAI is going to pay 754% more per acre than fashion-designer Tom Ford got for his ranch outside Santa Fe, which is the most expensive part of the state.

- Tom Ford’s Ranch = ~$2,300/acre

- >20,000-acre ranch sold for $48 million in 2022.

- Includes a private airstrip + town used as the set for the Hollywood movies “Silverado” & “Thor”

Do you know why New Era is paying Pearce $70 million?

If you do and you are not a New Era insider, please contact us at [email protected].

New Era Also Overpaid for Texas Data Center Land

Someone needs to teach New Era’s management team a lesson in negotiating because they keep using shareholder’s capital to overpay for land.

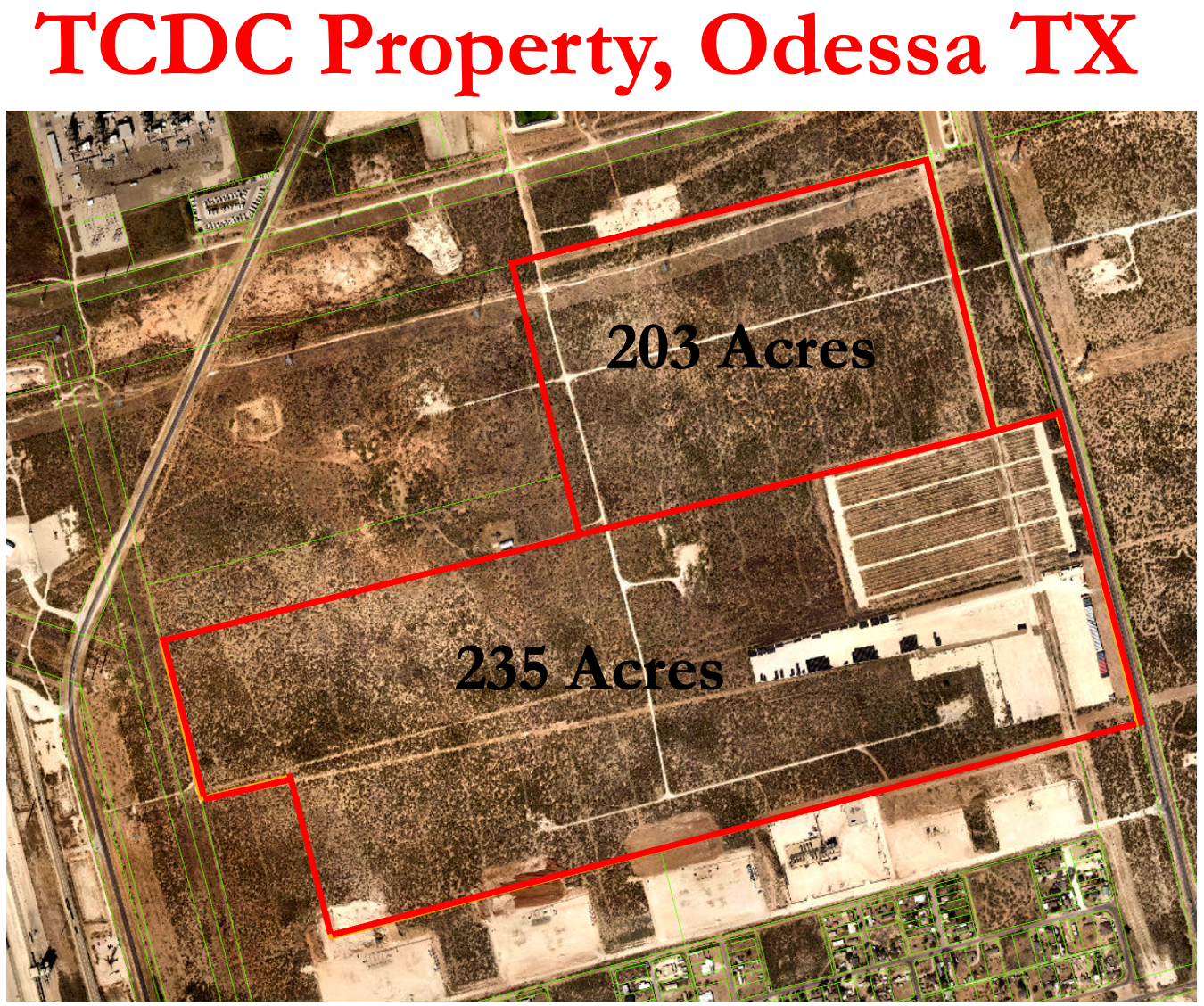

New Era reports owning 438 acres of land in Ector County for its Texas data center project. The first 235 acres were bought in July for an estimated $1.65 million. Despite NUAI not disclosing the price, NUAI spent $825k on their JV in that quarter. Since it’s a 50/50 JV, we believe the total purchase price of the land was $1.65 million. Ector County assessed the plot at $117,500.

Then in late November, New Era announced that it had paid ~$5 million for another 203 contiguous acres that Ector County assessed this year for only $144,000.

PART V – Short New Era Energy & Digital

3 Out of 4 Independent Board Members & CFO Quit – No Talent to Build Gray’s Pipe Dream

- CFO & 3 Board Members Quit as CEO Added Letters “AI” to Ticker and Started Spinning an Data Center Fantasy

- Only 4 Employees Listed on LinkedIn: ~$50 million of Market Cap per Employee

- Company Doesn’t Even Have Open Job Listings

Dental companies used to claim that 4 out of 5 dentists recommend their product. NUAI has a similar claim to fame, but it’s darker (grayer) — 3 out of 4 independent board members quit! And so did the CFO!

So what happens when the CFO and the Chairs of Audit & Corp Governance Committees all resign – naturally CEO who is now also CFO gets a salary raise that year!

Gray, CEO is Now Also CFO – What Could Possibly Go Wrong?!?

Right now, NUAI has no team to actually build much of anything. Earlier this year, Will Gray abandoned the company’s helium extraction plans for a new shiny penny … dreams of being an AI company.

Gray said in a Nov. 25 paid-stock promotion video that the company was looking to still looking to replace the old CFO who left in April. That’s 9 months without a CFO at a company that’s admitted a material weakness in financial reporting.

In the meantime, Gray, who’s faced past accusations of securities fraud is serving as CFO too. Should investors be worried? We think so.

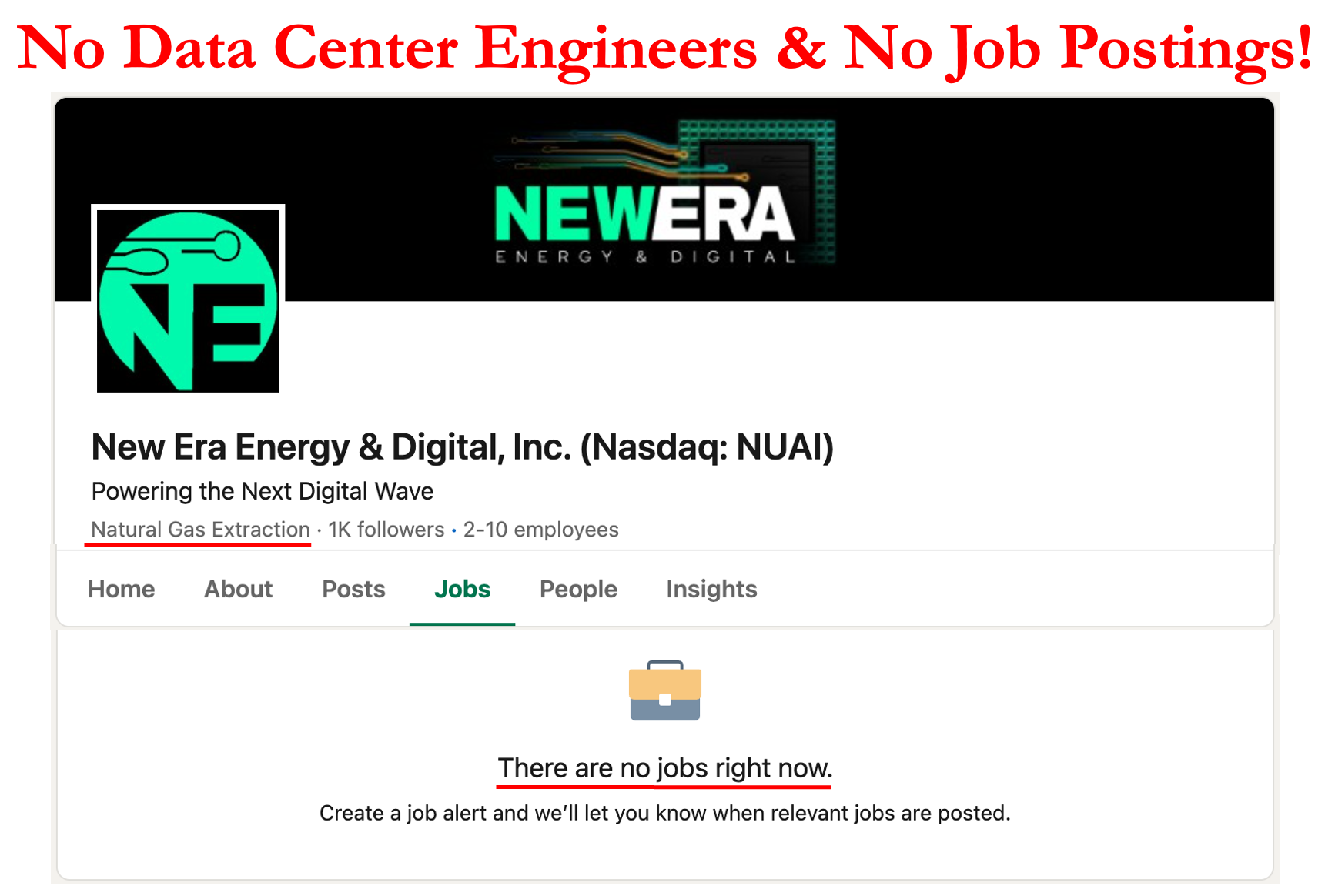

NUAI Has No Data Center Engineers & No Job Listings

Gray also said in the Nov. 25 paid-stock promotion video that the company needs engineers who know how to build data centers and a chief development officer. But is he actually hiring? We couldn’t find any job listings for any role at NUAI.

NUAI Only Lists 4 Employees. That’s ~$50 million of Market Cap Each!

In March, NUAI’s 10-K said it had 7 employees, but that was before everyone quit. In our recent searches we could find only 4 current employees on LinkedIn besides new board members (1, 2 and 3), and like Gray, all of them lack the necessary experience to build a major power plant or an AI data center.

New Era’s current employees consist of only CEO E. Will Gray, a Land Director from Gray’s previous Bankrupt Company, and 2 oil & gas operations engineers that manage the depleting gas wells.

Hilariously one of the newest board members listed in New Era’s November 10-Q doesn’t even bother to mention the company on his LinkedIn. But luckily for investors that board member already has experience with failed SPAC’s having previously been a board member at Lightning eMotors.

PART VI – Short New Era Energy & Digital

NUAI Has Bad Gas (Wells). Wells Lose Money & Can Only Produce ~5% of Power Needed

- NUAI Wells Only Produce ~5% of Gas Texas Data Center Requires

- 3rd Party Appraisal Shows Wells Are Unprofitable

- Require ~$370 million of Capex to Develop

- Lost ~$1,600/well in 2024

- Wells Described as “The Industry Dregs” & “Deteriorated”

- 87 Wells came from a Company Will Gray, was CEO of and Ran into Bankruptcy

Now that it’s failed at extracting helium from its >400 hundred gas wells, NUAI says the gas will power its Texas data center data, ensuring price stability. We talked to experts who thought that must be a joke.

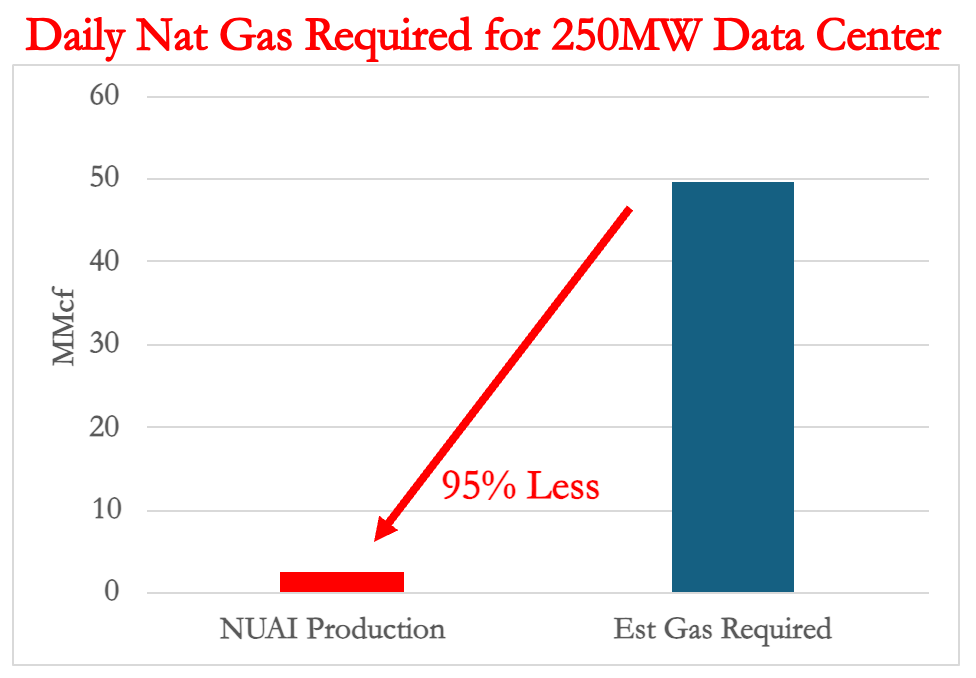

NUAI Produces Only ~5% of Gas Required for Texas Data Center

Experts told us NUAI cannot possibly supply enough gas to power their Texas Data Center, from the wells they own despite what NUAI has claimed. Best case they can only supply ~5% of what they promised.

NUAI produced ~2.5 MMcf/day in 2024 while a 250 MW data center requires 42-57 MMcf/day of gas based on the heat rate of the power plant. Experts told us a new efficient reciprocating engine has a heat rate of ~7,500 Btu/kWh while Siemens and GE turbines typically run around 9,000-9,500 Btu/kWh. Using this information, we estimate NUAI’s proposed 250 MW data center requires 42-57 MMcf of gas per day. The bad news for NUAI investors is that NUAI produced only ~2.5 MMcf of gas per day in 2024.

That means NUAI’s own gas wells can only supply ~5% of what their plans call for. This exposes NUAI or a potential customer to natural gas price fluctuations if they have to drill new wells in the future. See Appendix C for details on how to do the math.

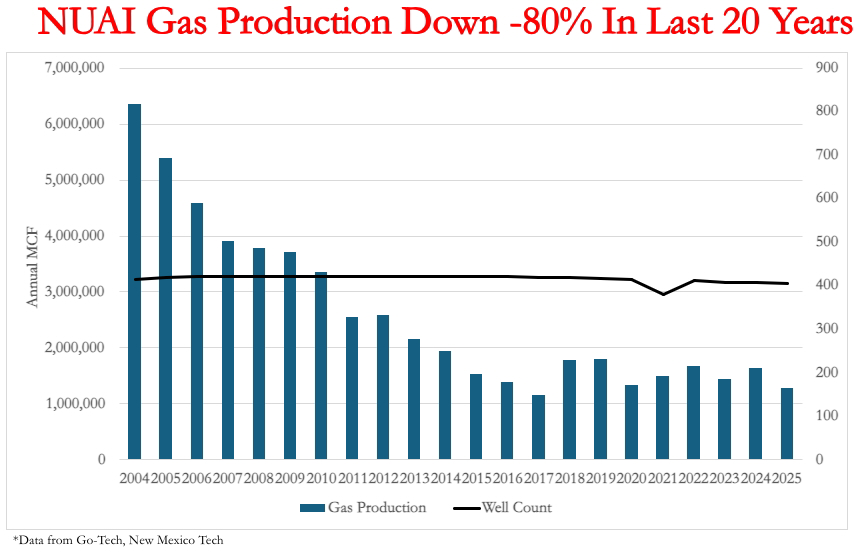

Here’s NUAI’s declining gas production over the last 20 years. Paid stock promotion hyping a data center is not going to make them more productive.

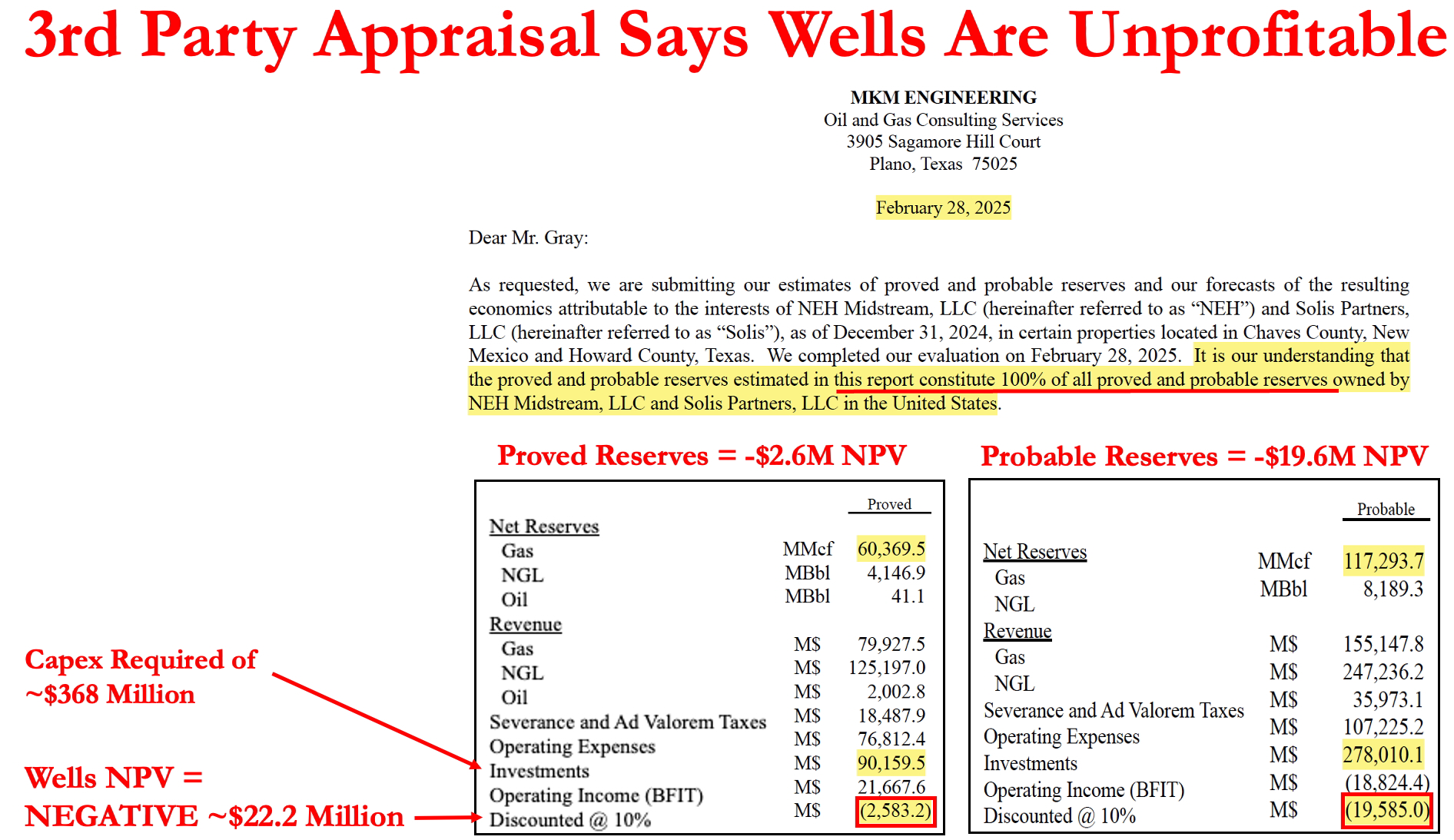

3rd Party Appraisal Commissioned NUAI Says Wells Have Negative NPV – Wells Would Require ~$370 million of Capex to Develop

NUAI’s wells are old — the median age is 42 years, well beyond the 20-30 average lifespan of wells in the Permian Basin – and the economics are terrible, according to a third-party appraisal commissioned by New Era this year.

The same can be seen in NUAI’s financials. In 2024, New Era operated 406 gas wells and lost ~$1,600 of cash per well.

- Revenue from oil & gas = ~$533k, or $1,300 per well

- Lease Operating Expenses = ~$1.2 million, or ~$2,900 per well

- Total cash loss per well = ~$1,600 per well

85% of Wells Were Bought Off Companies That Went Bankrupt Operating Them

Of NUAI’s 406 gas wells, 346 were acquired from companies that went bankrupt operating the very same wells, including 87 wells from the company E. Will Gray II was CEO of and bankrupted himself, Remnant Oil.

The company that operated 259 of the wells, Grizzly Energy, twice went bankrupt trying to squeeze cash from declining production!

PART VII – Short New Era Energy & Digital

No Customers Because Gray’s Plan is More Decrepit Than NUAI’s Old Gas Wells – No Permits, No Guaranteed Financing

- Has NOT Applied for Construction Permits or Air Permits

- Strategic Partners are Actually Recently Created Co’s that Lack Experience and Have Never Executed

- Deals are Non-Binding MOUs — a.k.a. Worthless Pieces of Paper

- No Wonder There are No Customers

It’s easy to assess New Era’s plans for two data centers campuses because the plans barely exist. Building power plants and data centers requires great execution and reliable partners. New Era has none of the required pieces.

Not only are NUAI’s natural gas assets old and decrepit but investors are relying on strategic partners that are only months old, have never executed a similar size project, and the agreements are only non-binding MOUs, aka worthless pieces of paper.

There is a reason there is no data center customer. In fact, there are multiple reasons, NUAI has:

- No Air Permits & No Construction Permits – Haven’t Even Applied

- No Gas Turbines & No Reciprocating Engines

- No Financing – Non-Binding MOUs w/Co potential collaboration = BS

- No Active Construction at Claimed Sites

- No Surprise … NO CUSTOMERS!

The only thing New Era actually has is old bad gas wells that can’t even produce the energy necessary for the project Gray is pitching to investors.

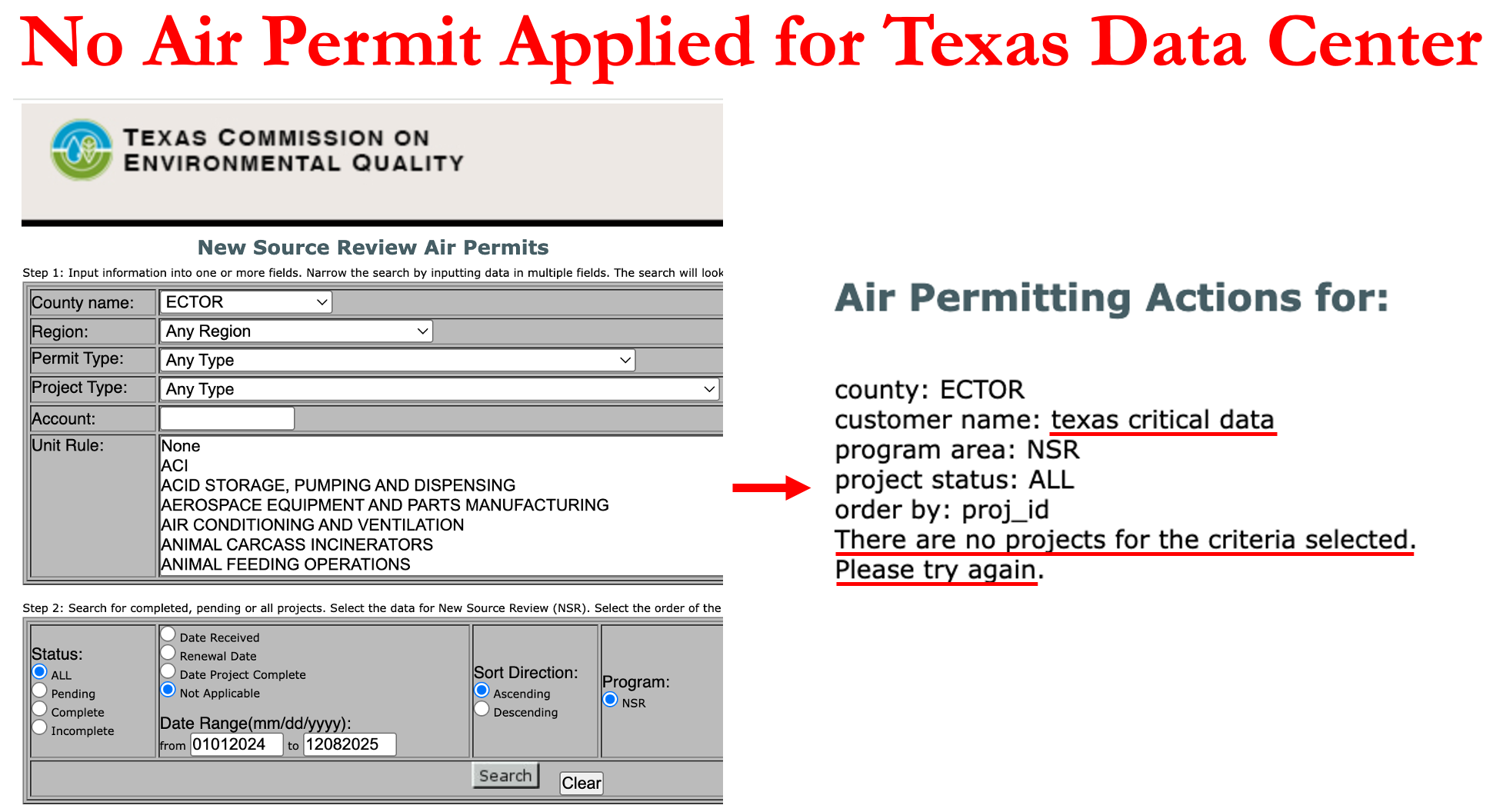

Gov’t Databases – NUAI’s Has NOT Applied for Needed Permits

We searched Texas, New Mexico and Federal government databases for the construction and environmental permits that NUAI will need to start building its data centers and power plants. We found NOTHING – not even an application.

Texas Commission on Environmental Quality would provide the air quality permit. It’s supposed to be among the easier permits to get. Yet searches under all possible permutations of NUAI, their subsidiaries, and project names shows no applications have even been submitted, despite NUAI telling investors it’s made significant progress.

Experts in the field told us NUAI or any of its affiliates are required to get an air permit especially because they claim to plan to operate behind the meter, 24/7. “If they don’t tie to the grid, they have to get a major source submission or permit for those gas units, no matter where they are in Texas”

Non-Binding Term Sheet – Power Gen “Partner” Created Last Year – No Other Major Projects & Only 5 Employees on LinkedIn

NUAI is planning a reverse Field of Dreams for its Texas data center – if the customers come, NUAI and its partners will build it.

AI Data center experts told us they didn’t believe NUAI’s 18-month timeline. They told us at a bare minimum that:

- Siemens & GE gas turbines are 4-5 years backordered

- Reciprocating engines would take >24 months (12 months backordered + at least another 12 months to install)

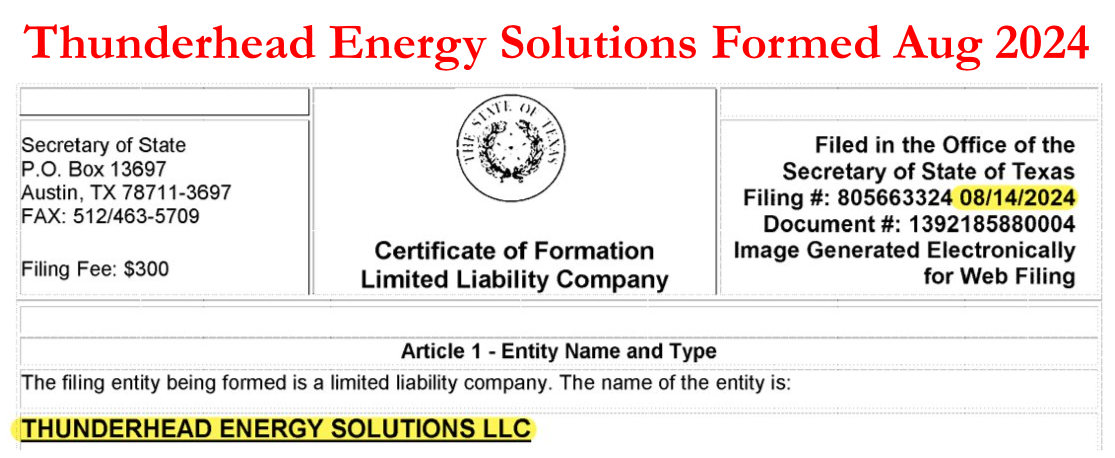

NUAI hyped its construction deal in September when it signed a non-binding term sheet with Thunderhead Energy Solutions, which will own and operate the 250MW plant at the data center site. But there is a catch – the MOU only becomes binding if NUAI signs up a customer.

Thunderhead also has no track record and does not even appear to have guaranteed funding. Besides the MOU with NUAI, the only deals Thunderhead has announced is a “funding relationship” arrangement with an investment fund that agreed to collaborate with them. Strategic collaborations are just a fancy way of saying another BS non-binding LOI that you can’t bank on.

Even in the farfetched world where Thunderhead does get funded, NUAI still DOES NOT own or profit from the power generation. Thunderhead has not appeared to have completed any power plants or even started building one according to our diligence.

Another Non-Binding MOU w/GlobeLink – Created in June 2025 & Only 2 Employees on LinkedIn

NUAI said in September that it signed a non-binding MOU with GlobeLink Holdings LLC for 1,600 miles of fiber optic network across Texas to connect would-be customers to its still imagined data center. GlobeLink appears to have never done anything before – like nothing at all. It is a brand-new business:

- GlobeLink’s website was created on May 31

- GlobeLink was incorporated in June.

- GlobeLink’s LinkedIn shows 2 employees

The employees appear to at least know how to cut-and-paste a press release. They announced their only other business – another fiber optic network for a company called GGS Energy — with a press release that is nearly identical to one NUAI put out about its own fiber optic network plans.

No Guaranteed Financing for Data Centers – Est Cost $72.5 billion

It’s hard to fund $72.5 billion of capex when cash is primarily being spent on stock promotion.

NUAI claims to have two data center projects: Texas Critical Data Centers (TCDC), which is slated to start at 250MW and scale to 1GW, and the still unnamed New Mexico project which is supposed to power 7GW of data centers. CEO E. Will Gray II has said it will cost $10 million per megawatt to develop these data centers. That implies the total cost of the data centers at ~$72.5 billion.

NUAI Has No Answers – Can’t Say How Cash Will Flow to Shareholders If Data Centers Ever Come Online

Gray and Executive Board Director Charlie Nelson made a promotional pitch on a X/Twitter Space on Dec. 8, and were asked: “How do NUAI shareholders get paid?”

They could barely answer, rambling on about how they need to raise billions of dollars in debt to pay for infrastructure at the sites, and how the power plants would be owned by the company hired to build them. NUAI’s revenue would come mostly from land leased by customers, which they don’t yet have, and that it would have to pay down its large debt, they said.

“Equity gets paid, obviously debt gets paid, and then there’s yield paid … this is where you can kind of flex” ~ Charlie Nelson, NUAI Executive Board Director

Translation: NUAI shareholders eat last. Anyone who knows corporate finance knows debt gets paid first, especially during bankruptcy, a process that Gray’s past investors are very familiar with.

PART VIII – Short New Era Energy & Digital

Co-Founder of NUAI’s Texas JV Partner, Sharon AI, Accused of “Self-Dealing” at Previous Company

- Sharon AI (Roth Reverse Merger) first met NUAI (Roth SPAC) via … Roth

- Sharon Created via Related Party Transaction

- Also Has No Experience Building Massive Data Centers

A big part of the bull case for NUAI is its JV partner for its Texas data center, Sharon AI. Sharon AI is set to come public soon by reverse merging into a liquidated Roth SPAC. But our research revealed that Sharon is another reason to short NUAI: Sharon is a small-time Australian company built off an apparent related party transaction and whose founder has been accused of “related party transactions and self-dealing.”

Furthermore, NUAI management admitted on a recent Twitter spaces that they were only introduced to Sharon AI via their SPAC Co-sponsors, Roth Capital. Roth is better known for past conferences & parties featuring topless models, not underwriting and connecting AI leaders.

Sharon AI Co-Founder Accused of “Self-Dealing” at Previous Co;

Now Appears to be Using Same Setup at Sharon AI

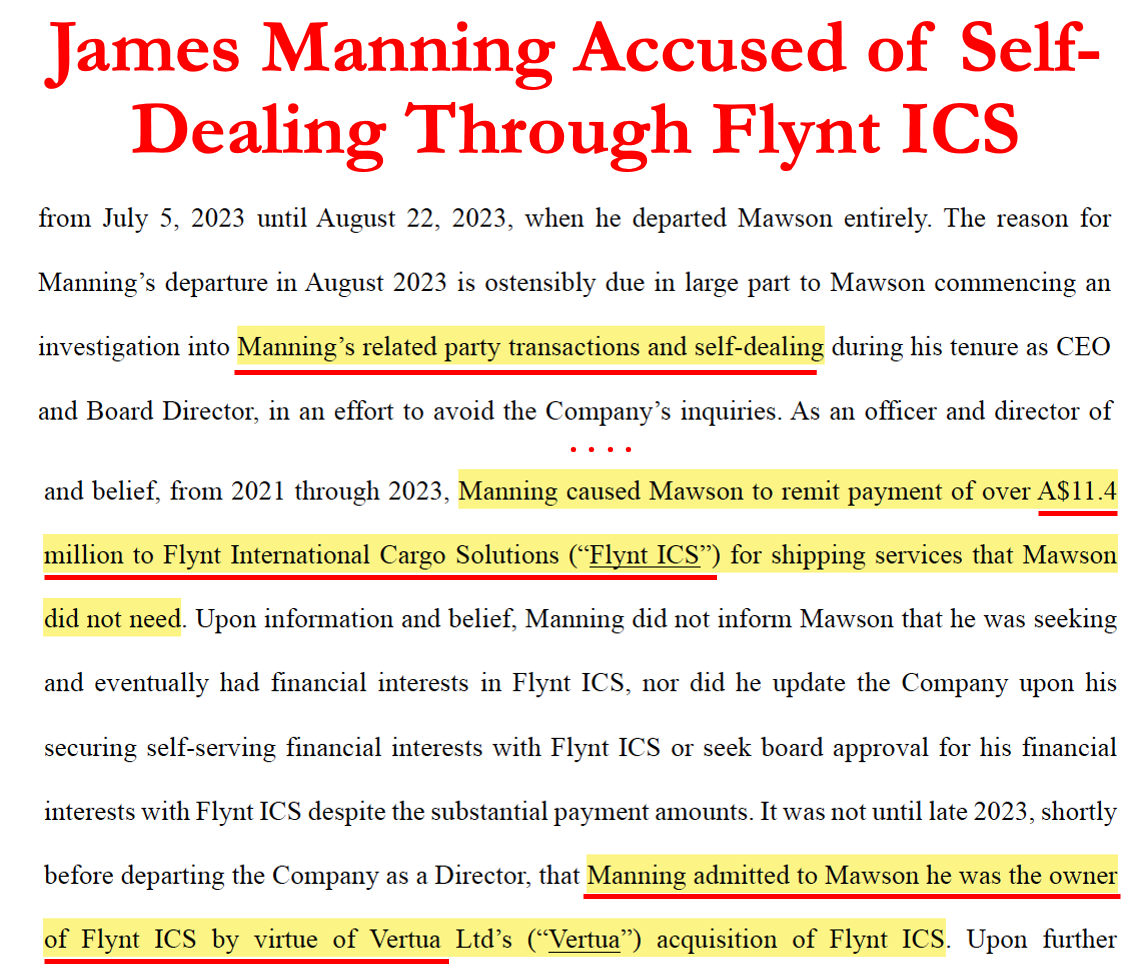

Sharon’s co-founder and chairman James Manning was also the former CEO and Director of Mawson Infrastructure Group, a company now down -100% and in bankruptcy. A debtor in the ongoing bankruptcy proceedings has accused Manning of “related party transactions and self-dealing” for using Mawson to pay another of his companies, Flynt ICS, $7.5 million (A$11.4 million).

And now Sharon AI is paying Flynt ICS — it made a payment of ~$168,000 in 2024 for “storage services.” The payment should be a massive red flag to the bulls.

Sharon AI was Created by Related Party Transaction; Also Has No AI Data Center Experience

Sharon AI was incorporated in 2024 and then bought Distributed Storage Solutions, a cloud computing and blockchain company that was partly owned by Sharon co-founder James Manning. Sharon paid $25 million for DSS, even though Australian financial filings for Manning’s investment firm, Vertua Ltd., show it was worthless only eight months earlier.

The Australian filings reveal a lucrative related party transaction for Manning, who grossed ~$1 million:

- Sept. 2023: Vertua Ltd valued its est. 4% stake in DSS at ZERO (Pg. 3)

- March 2024, Vertua valued its DSS stake a $396,000 (giving DSS a $9.9 million value)

- In May 2024, DSS is sold for $25 million – Manning gets ~$1 million.

- That’s ~2.5x more than what it was worth just 2 months prior!

Sharon AI currently lists its Australian headquarters at the same Sydney address as another Manning firm, Defender Asset Management. Sharon’s U.S. offices are in a Pennsylvania coworking office.

Like NUAI, Sharon and has no experience building massive power-generating AI data center projects.

Sharon also plans to use Roth – which New Era used in its deSPAC – for its plan to go public by reverse merging into an OTC-listed liquidated Roth SPAC shell.

PART IX – Short New Era Energy & Digital

Gray Promised Helium but Delivered Hot Air – Satellite Images Reveal Brushland Where Plant Should Be

- Helium Customers Bailed; No Funds to Finish the Project

- Satellite Images Reveal the Truth When Mgmt Won’t

- They Show Empty Land Where Gray Promised Helium in Q1, Q2 & Q4

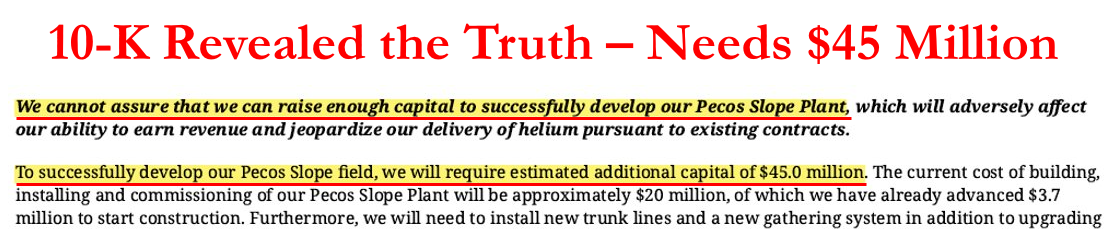

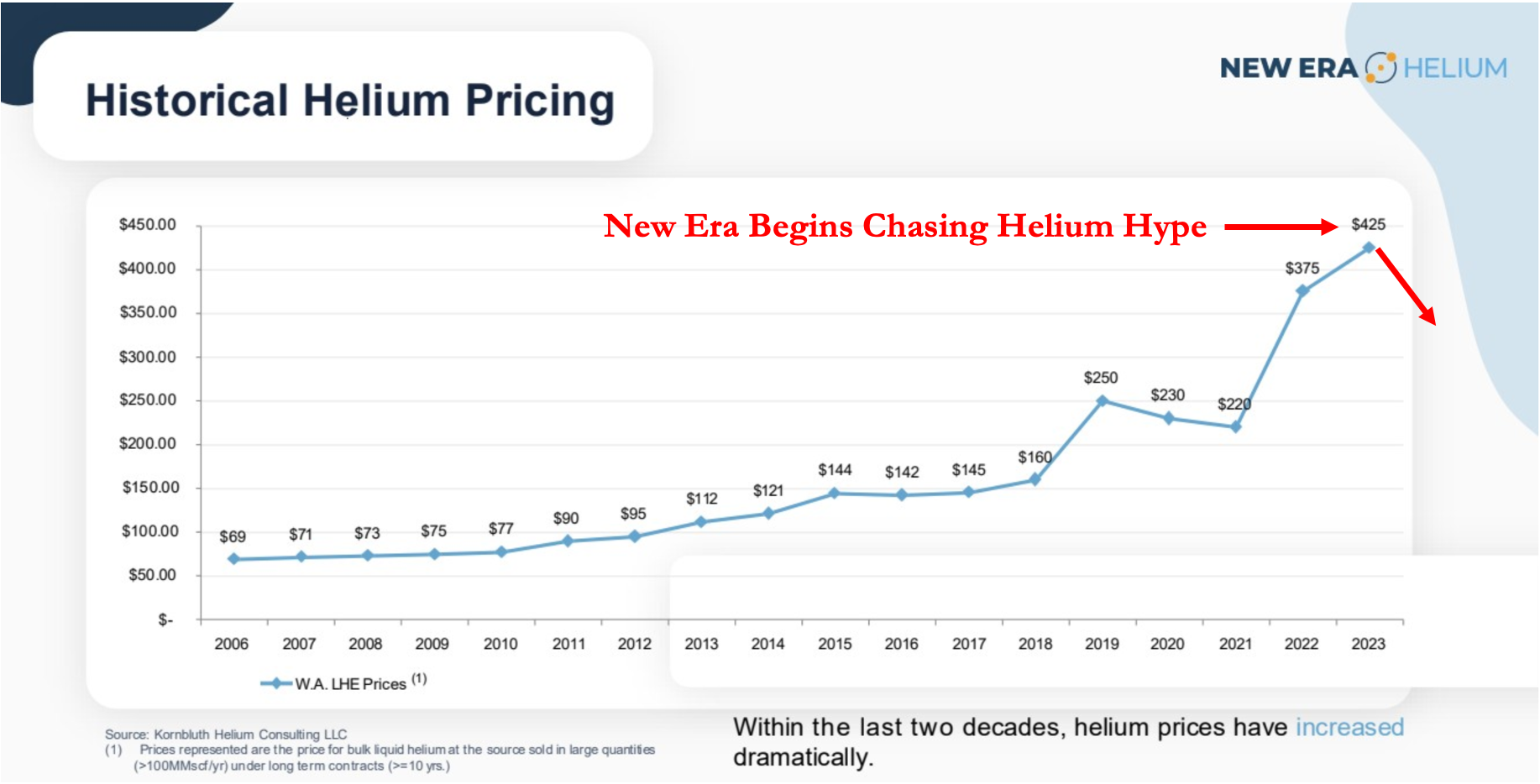

New Era’s AI data center hype story is entirely based on it raising tens of billions of dollars. But it couldn’t manage to raise $45 million for its helium extraction plant back during Helium Squeeze 4.0 when prices for the gas were still high. And now the plans are “on hold” according to a person familiar in the project.

“The [helium] project has been on hold … the company is short the funds to complete the plant” ~ person familiar with NUAI’s Pecos Slope project

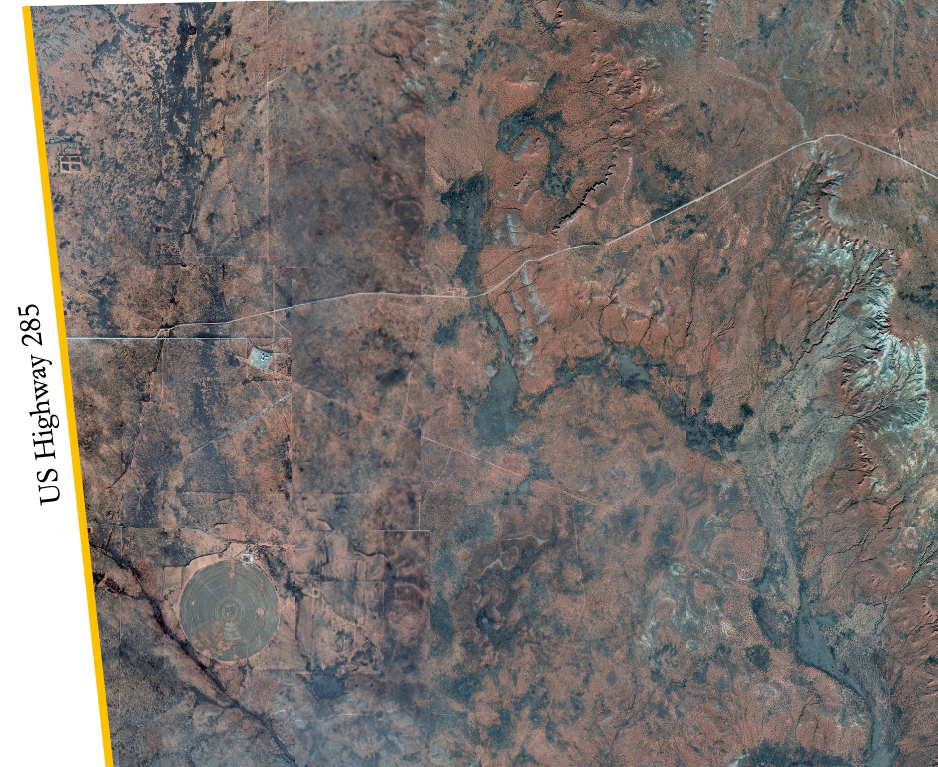

Satellite Images Reveal Scrub Brush Where Helium Plant Should Be

NUAI’s latest line is that the plant will be operational before the end of the year. But satellite images of the New Mexico site show empty brush scrub with no helium plant or even a hint of construction to be seen.

NUAI Keeps Promising Helium and Delivering … Nothing

New Era has spent 1.5 years promising its Pecos Slope Plant was about to come online and failing to deliver.

“Plant is expected to commence operations sometime in the first quarter of 2025” ~ S-4, June 2024

“We expect the Pecos Slope Plant to commence operations in Q2 of 2025” ~ 8-K, Dec. 2024

“The Pecos Slope Plant is expected to commence operations in the fourth quarter of 2025” ~10-K, Mar 2025

But even as it was promising the plant would be ready in Q4, New Era also admitted that it had run out of money for the plant, saying in its latest filings that it had only spent ~$4.95 million and has not been able to secure the remaining $45 million it needs.

The person familiar with the project said that the spending numbers in New Era’s March 10-K remain largely unchanged today.

NUAI Failed to Catch the Helium Squeeze & Lost Customers

Both of New Era’s helium offtake agreements with AirLife and Matheson Tri-Gas were terminated because New Era could not get their plant built.

Helium was New Era’s first attempt to capitalize on the latest hype. Helium Squeeze 4.0 began in 2021, and New Era was founded two years later, near the top of helium prices. The helium balloon has since deflated, along with NUAI’s helium ambitions.

Conclusion – Short New Era Energy & Digital

Short New Era – Your Safe Word Should Be “Sell”

If you’ve read this far, you know that New Era is not a serious business with real plans. Its prospects are as invisible as helium gas and far less useful to anyone except for its co-founders, who are already enriching themselves via related party deals with investors’ cash.

New Era Helium Energy & Digital (NUAI) is a simple story. It’s a story about a CEO, E. Will Gray II, who has 20 years of experience of running Penny Stock wipeouts and has often used paid stock promotion. But somehow Gray’s shady past hadn’t been exposed yet.

NUAI’s story actually started off with deteriorating gas wells from Gray’s previous bankruptcy at Remnant. Gray acquired the wells back out of bankruptcy and found a new story to pitch – extracting helium from the old natural gas wells. But consistent with all Gray’s past companies, he failed to execute so he pivoted and found a new story to spin to retail investors with the AI boom. We believe Gray will again fail, spectacularly. Gray’s core team and board already quit on him. NUAI lacks the talent, lacks the team, and, most important, is sitting on old, bad natural gas assets. The only thing we found that Gray has significant experience successfully executing on is using related party transactions to extract value out of penny stock shells that end up worthless.

Since E. Will Gray II is currently 50 years old, it is fitting that we are now exposing the “Fifty Shades of Gray.” We believe the NUAI story is going to end like all of Gray’s past companies … with retail investors taking a beating. Be careful believing Gray’s promises. We think investor’s safe word should be … “SELL.”

Fuzzy Panda Research is Short NUAI

Appendix A – Finding New Era’s Helium Plant: A Step-by-Step Guide

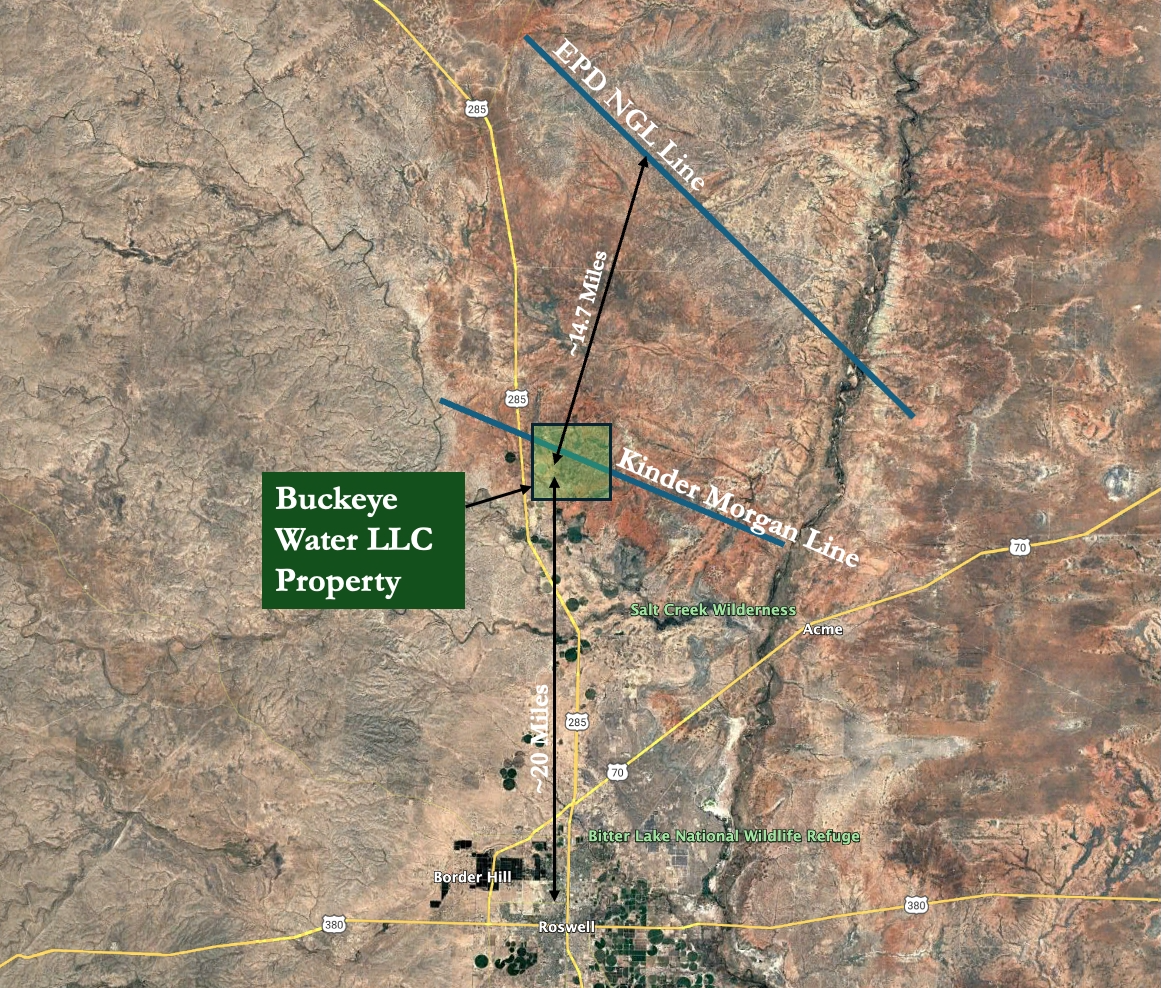

NUAI doesn’t tell investors where their Pecos Slope helium plant will be constructed. Instead, they say that it is:

- 20 miles north of Roswell, New Mexico

- Less than 0.5 miles to the El Paso Kinder Morgan line

- ~14.7 miles to the EPD NGL line

- Less than 1 mile from a major highway

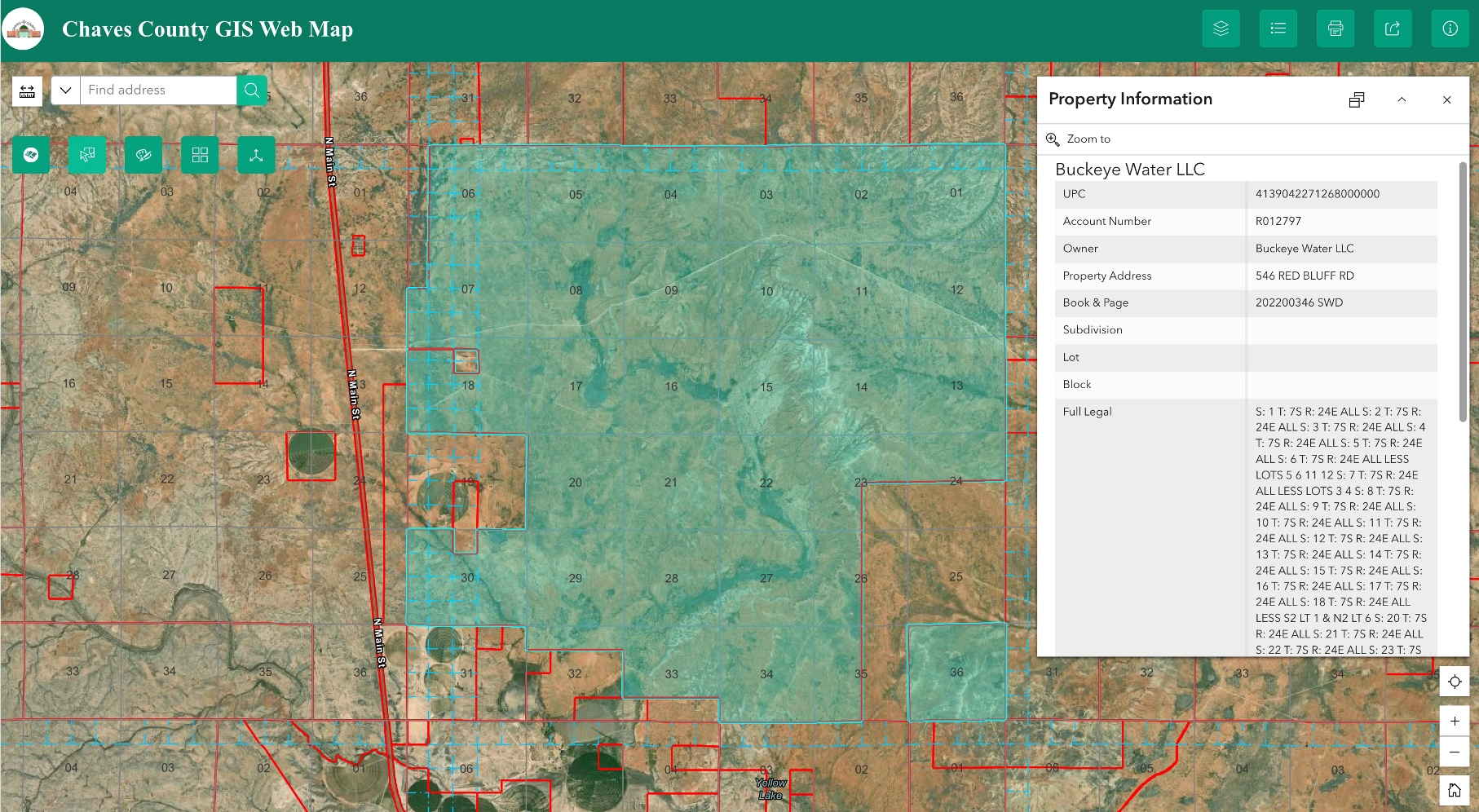

Using these clues, we believe we’ve found where their helium plant is supposed to be located. And it just so happens to appear to be on land owned by Buckeye Water LLC.

Using Google Earth, NPMS Viewer, Kinder Morgan’s website, and EPD’s website, we mapped the clues provided by NUAI to estimate where the helium plant may be located.

The green shaded box corresponds to this plot of land owned by Buckeye Water LLC, which is owned by Benjamin Pearce – the same land owner that NUAI signed the $70 million land purchase option agreement from in New Mexico for their 7GW data center campus.

Appendix B – Bad Gas Assets; How to Pull NUAI’s Well Data

To confirm NUAI has bad gas wells for yourself, follow these steps to analyze the data yourself:

- Go to New Mexico’s OCD Permitting website and search NUAI’s subsidiary “Solis Partners” in the operator field. This will load all >400 wells NUAI operates.

- Clicking into each well will provide information including previous operators, and historical production near the bottom of the page

- On the bottom of the results page, there is a button to “switch to well search expanded results.” We recommend clicking this to get more data

- Then export this to excel to begin your analysis

To see the decline curves of each well, you will need to manually click into each well and copy the historical production figures into the excel sheet. After doing this for all of NUAI’s 406 wells, you can then analyze the decline curves and get a better sense of how little these wells can produce relative to NUAI’s data center needs.

Additionally, you can also visit Go-Tech, a website run by New Mexico Tech, and download the production data for Solis Partners. This will allow you to see the declining gas production.

Appendix C – The Math Behind New Era’s Money Losing Gas Business

According to experts in the field, the heat rate for the most efficient combined cycle power plants run at ~7,000 Btu/kWh. This is in-line with an article from Energy KnowledgeBase. We were told Siemens and GE turbines typically run around 9,000-9,5000 Btu/kWh at best. And the most efficient newly designed reciprocating engines run ~7,500-7,800 Btu/kWh.

To convert from kWh to MWh, just multiply by one thousand. That means the heat rate for NUAI’s proposed data centers could vary from 7-9.5 million Btu/MWh. And 1 million Btu is ~1Mcf of natural gas. Therefore, the heat rates can vary from:

- 7 Mcf/MWh on the low end

- 9.5 Mcf/MWh on the high end

Now a Behind the Meter (BTM) power plant for data centers is expected to operate 24/7, meaning every hour it can generate 250 MW of power. Therefore, the data center would need:

- 1,750 Mcf/hour (250 MW*7 Mcf/MWh) which is 42 MMcf/day (1,750 Mcf/hour*24 hours) on the low end and,

- 2,375 Mcf/hour (250 MW*9.5 Mcf/MWh) which is 57 MMcf/day (2,375 Mcf/hour*24 hours) on the high end

New Era reported that it produced 903,985 Mcf of gas in 2024, which is ~904 MMcf/year (903,985/1,000). This is equivalent to ~2,480 Mcf/day which or ~2.5 MMcf/day.

Therefore, NUAI’s current wells only have the capabilities to supply 4-6% of the daily gas required for a 250 MW AI data center.

Appendix D – PCAOB Found Deficiencies in Auditor’s But To the Auditor’s Credit – They Still Give NUAI a Going Concern Notice & Cite Material Weaknesses

New Era’s auditor since 2023 has been Weaver and Tidwell, which the PCAOB found in 2024 had included “unsupported opinion” deficiencies in two of previous audits — meaning the firm had not obtained sufficient appropriate evidence to justify its clean audit opinions.

One of the deficient engagements involved an oil and gas issuer, where Weaver failed to properly audit the reserves-based valuation of O&G properties. The PCAOB also cited weaknesses in Weaver’s fraud-focused journal-entry testing and basic reporting.

New Era’s reliance on Weaver raises questions about much comfort investors should take from its audited financial statements, especially where the auditor’s judgement can have massive impacts, like reserves and fair-value estimates. It’s even more of an issue because New Era’s previously reported material weakness over internal cost and financial controls, which is not very surprising considering the CEO is also the CFO.

Going Concern Notice & Material Weakness in Financial Reporting = Bad News For Investors

Even after all of the additional cash raised in Q3 NUAI’s auditors’ still highlight a “going concern notice” in NUAI’s most recent 10-Q in November.

The flags that not only is NUAI running out of cash but it also has “ineffective internal controls over financial reporting.”

Auditors cite Material Weaknesses in NUAI’s Financial Reporting

Fuzzy Panda Research Disclosures, Disclaimer and Terms of Service:

By downloading from or viewing material on this website and/or by reading this report, you agree to the following Terms of Service. You agree that any use of the research in this report or on this website is at your own risk. In no event will you hold Fuzzy Panda or any affiliated party, including officers, directors, employees, consultants, and agents of Fuzzy Panda or any companies affiliated with any of them, liable for any direct or indirect losses caused by your use of or reliance on information on this site or in this report. You further agree that you will not rely on any information in this report or on this website, to do your own research and due diligence before making any investment decision with respect to companies or securities mentioned herein, and that you will consult with your own investment professionals prior to any investment decisions. You represent that you have sufficient investment sophistication to critically assess the information, analysis and opinions in this report or on this site. You further agree that you will not communicate the contents this report or other materials on this site to any other person unless that person has agreed to be bound by these same Terms of Service. If you accessed, download, or receive this report or the contents of other materials on this site as an agent for any other person, you are binding your principal to these same Terms of Service.

As of the publication date of this report, Fuzzy Panda, and possibly any companies affiliated with it or its members, partners, employees, consultants, clients and/or investors (the “Fuzzy Panda Affiliates”), have a short position in the stock (and/or options, swaps, and other derivatives related to the stock) and bonds of the company covered in this report (the “Covered Company”). Fuzzy Panda and the Fuzzy Panda Affiliates therefore stand to realize significant gains in the event that the prices of either equity or debt securities of the Covered Company declines. There are many factors that can go into a decision to cover the short position(s) in the Covered Company’s securities and it is not possible to predict exactly when or for exactly what reasons Fuzzy Panda and the Fuzzy Panda Affiliates may cover their positions, in whole or part, or otherwise change their investment holdings. As a general matter, Fuzzy Panda and the Fuzzy Panda Affiliates intend to cover some or all of their positions at a time that the price of the Covered Company’s securities are lower than when they were sold short or otherwise invested in. Fuzzy Panda and the Fuzzy Panda Affiliates may cover some or all of their short positions immediately after the publication of this report or an indefinite period after its publication. Similarly, Fuzzy Panda and the Fuzzy Panda Affiliates may cover some or all of their short positions if the price of the Covered Company’s securities move a small amount or after moving a larger amount. Fuzzy Panda and the Fuzzy Panda Affiliates intend to continue transactions in the Covered Company’s securities for an indefinite period after the publication of this report, and they may be short, neutral, or long at any time after the publication of this report regardless of any opinions, possible stock prices or valuations, or other views stated in the report. Fuzzy Panda will not update any report or information on this website to reflect any changes in the investments of Fuzzy Panda or the Fuzzy Panda Affiliates that existed at the time of the publication of this report, or any new positions in any securities of the Covered Company.

This report and the Fuzzy Panda website is informational and describes the opinions of Fuzzy Panda. This report is not an offer to sell or a solicitation of an offer to buy any security, and Fuzzy Panda does not offer, sell or buy any security to or from any person through this report or the Fuzzy Panda website. This report is not a recommendation or advice to short or otherwise invest in or trade any security. Fuzzy Panda does not render investment advice to anyone unless it has an investment adviser-client relationship with that person evidenced by a formal written agreement. You understand and agree that Fuzzy Panda does not have any investment advisory relationship with you, or owe any fiduciary or other duties to you. Giving investment advice requires knowledge of your financial situation, investment objectives, and risk tolerance, and Fuzzy Panda has no such knowledge or information about you.

If you are in the United Kingdom, you confirm that you are accessing research and materials as or on behalf of: (a) an investment professional falling within Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “FPO”); or (b) high net worth entity falling within Article 49 of the FPO.

Fuzzy Panda’s research and reports express the opinions of Fuzzy Panda, which are based upon generally available information, field and online research, and inferences and deductions through due diligence and the analytical process. Fuzzy Panda believes that all information contained in this report has been obtained from accurate and reliable public sources, and no material nonpublic information was obtained from any person who had a duty to keep information confidential. However, Fuzzy Panda cannot be certain that the information it has relied upon in this report is accurate. The information and opinions in this report are therefore presented “as is,” without warranty of any kind, whether express or implied. Fuzzy Panda makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. This report also contains forward looking statements about what may occur in the future. The future cannot be predicted with certainty and any of the forward-looking statements about projections, beliefs, estimates, assumptions, outcomes, or any other future event may be incorrect. Among other things, any forward-looking statements may be rendered inaccurate by incorrect assumptions, incorrect methodologies, unforeseen risks and events, or other variables. Any opinions about the possible future stock price of the Covered Company or fair value of its securities is not a price target and does not mean or imply that Fuzzy Panda or the Fuzzy Panda Associates will hold any investment until such price or valuation is met. Further, all expressions of opinion, including any conclusions drawn from Fuzzy Panda’s analysis, are subject to change without notice, and Fuzzy Panda does not undertake to, and will not, update or supplement any reports or any of the information, analysis and opinion contained in them.

You agree that the expressions of information in this report are copyrighted and owned by Fuzzy Panda Research, and you therefore agree not to distribute this report, any excerpts from it, or information from the Fuzzy Panda website (whether the downloaded file, copies / images / reproductions, or the link to these files) in any manner other than by providing the following link: www.fuzzypandaresearch.com. If you have obtained Fuzzy Panda’s research in any manner other than by accessing or downloading from that link, you may not read such research without going to that link and agreeing to the Terms of Service. You further agree that any dispute between you and Fuzzy Panda and/or any of the Fuzzy Panda Affiliates arising from or related to the material on their website shall be governed by the laws of the State of California, without regard to any conflict of law provisions. You knowingly and independently agree to submit to the personal and exclusive jurisdiction of the state and federal courts located in California and waive your right to any other jurisdiction or applicable law. The failure of Fuzzy Panda to exercise or enforce any right or provision of these Terms of Service shall not constitute a waiver of such right or provision. If any provision of these Terms of Service is found by a court of competent jurisdiction to be invalid, the parties nevertheless agree that the court should endeavor to give effect to the parties’ intentions as reflected in the provision and rule that the other provisions of these Terms of Service remain in full force and effect, in particular as to this governing law and jurisdiction provision. You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to this report or the material on this website must be filed within one (1) year after such claim or cause of action arose or be forever barred.

Case 3:07-cv-00931-G — Frey v. Gray Jr, Gray Sr, Well Renewal Inc, et – Defendants appear to have never filed a response to the original complaint so the court entered into a default judgement. After default judgement the Plaintiff dismissed claims against Gray Sr. & Gray Jr, so we believe the default judgement only applies to Well Renewal Inc. We encourage investors to ask Will Gray II what occurred for more details. ↑

New Era hasn’t precisely specified its helium plant site. But it has said that it is 20 miles north of Roswell, NM, is less than a mile from a major highway, is ~15 miles from the EPD NGL gas pipeline and 0.5 miles from the El Paso Kinder Morgan pipeline. We triangulated that information and believe the helium plant is on a swath of land in southeastern New Mexico owned by Pearce’s Buckeye Water LLC. ↑