- T1’s Secret Warehouse Uncovered – Whistleblower Shares T1 Hides Panels That Were NOT Shipped

- Whistleblower Reveals >$130 Million of Sales Manually Booked for Q4-25 in Late Jan-2026

- No Documentation Was Provided

- T1 Utilizes Consulting Firm, Protiviti, to Book Unsupported Financial Entries

- Protiviti = Infamous Arthur Andersen’s Former Internal Audit & Risk Team

- Arthur Andersen was Auditor & Internal Consultants to ENRON

- Protiviti Managers Encouraged Staff to “Do what the Client Asks”

- T1’s Financials are “100% Not Accurate”

- Some 45X Tax Credits Have NOT Arrived – Internally People are “Freaking Out”

- Tax Credit Insurance Co – Euclid Refusing to Pay T1 Too

- T1 Allegedly Fires Employees That Ask Questions

- Possible Fraud was Reported to KPMG

Note – The T1 Energy whistleblowers have provided this information to the SEC in advance of publication.

Note to other Whistleblowers, former T1 Energy employees, or people with more knowledge about T1 Energy’s suspicious import-export records. You can reach out to us by emailing at [email protected]. We will protect your anonymity.

Additional Disclosure – Members of the Fuzzy Panda Research Team are short securities of T1 Energy (TE). The short positions we hold in T1 Energy are the same ones we held after verifying the whistleblowers statements and documents to be real at which time Fuzzy Panda Research placed T1 Energy on our internal restricted trading list. We did not share the information outside our core team and ceased communication about T1 Energy with those parties that are normally described as the Fuzzy Panda “Affiliates” – some of which we have a financial interest in their profits. As a result, we currently have no idea if the Fuzzy Panda “Affiliates” are currently short, long, or neutral securities of T1 Energy. We apologize to them for ducking their calls, texts, and emails about T1 Energy in recent weeks. We hope you didn’t make the mistake of betting against Panda. Additionally, we have no intention of providing updates about any future positions we may have in securities of T1 Energy (TE), nor disclosing when a company has been removed from our restricted list. Please see additional disclosures at the end of report and in our terms of service.

“I feel like everyone’s cooking the books for one person…they’re just moving and shuffling stuff around” ~T1 Energy Whistleblower

“You cannot trust our books whatsoever” ~T1 Energy Whistleblower

In Part 1 we revealed the actual solar cell invoices showing T1’s management mislead investors. We showed you the receipts.

In Part 2 we revealed the secret ways Trina has “effective control” of T1 Energy.

Now in Part 3 we are going to expose how T1 has been “cooking the books.” The whistleblower revealed to us:

- A Secret Warehouse T1 uses to Hide Solar Panels Customers Don’t Want – is this creative channel stuffing?

- Internal documents showing large manual revenue entries:

- >$130 Million of Revenue Booked Weeks After the Quarter Ended

- Journal Entries with No Support

- Additional Undisclosed Bill-and-Hold Revenue Booked in Q1 (Est ~1/3 of total revenue)

- Using 3rd Party Consultants for questionable journal entries. Protiviti, the consultant, was born out of the fraud that caused Arthur Andersen & Enron’s implosion.

- Missing 45X Tax Credits – Executives are “Freaking Out”

Reminder that coming soon is Part 5 – Proof of US Tax credits going to China. We think it’s a doozy and the details are damning.

But for now, we present many of the ways that T1 Energy appears to be manipulating their books. We are short T1 Energy.

Fuzzy Panda Research is Short T1 Energy (TE)

Additional Disclosure: For once and only this once we are going to provide additional disclosure into our actual current short positioning for our T1 Energy (TE) Short. Our positions have not changed since we placed T1 Energy on our internal restricted list. Additional details of our short position are available in Part 1 – The Solar Cell Invoices.

Note – We intend to hold the below positions through the publication of all 5 Parts of the Whistleblower Series.

Please see our Terms of Service and disclaimers at the end of the report for additional disclosure.

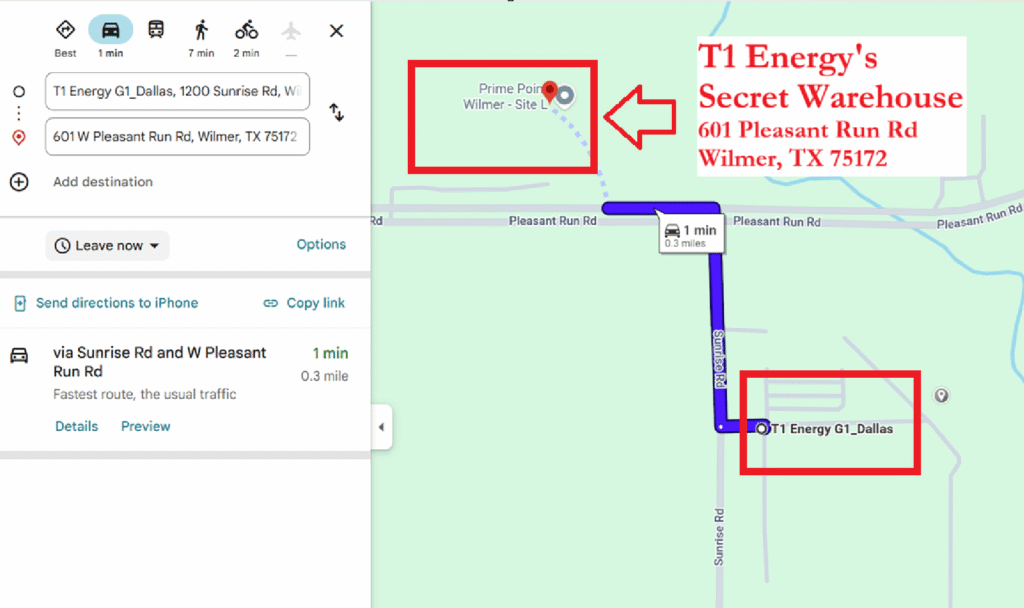

The Secret T1 Warehouse – T1’s Version of Channel Stuffing? – Solar Panels Shipped <1 Mile Away & Booked as Revenue

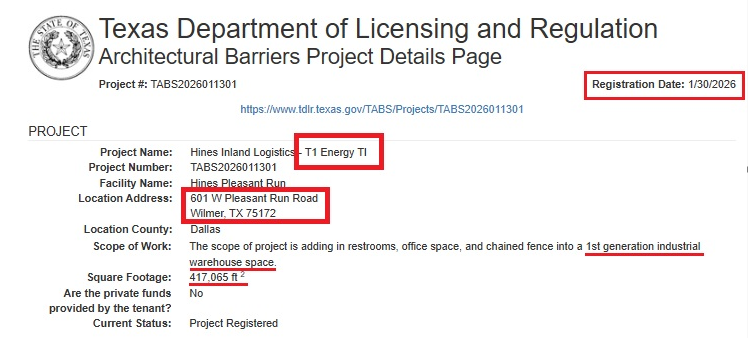

We uncovered that in Q1-2026 T1 Energy quietly leased and took over a ~420,000 sq foot secret warehouse across the street from T1’s G1 factory in Wilmer, Texas. The whistleblower told us that T1 Energy is likely using the secret warehouse to hide undelivered bill-and-hold solar panels that have been booked as revenue for T1 as well as unwanted finished goods.

We verified the location, size of the warehouse, and that T1 is leasing the whole building using records from Texas Dept of Licensing & Regulation. Google maps show that T1’s secret warehouse is only a 1 min drive away from the G1 Factory. Google street-view (from April) even shows multiple semi-trucks actively making deliveries.

Internal financial documents for T1 Energy sent to us by a whistleblower appear to reveal that in Q1-2026 there was an additional large amount of “bill-and-hold” revenue booked in Q1-2026 on top of the large bill-and-hold balance from Q4-2025. The whistleblower informed us that they believe that all T1’s excess inventory and/or undelivered panels are likely hiding at T1’s new “pleasant run location.” Based on the warehouse’s marketing deck, it appears T1 is leasing the entire space.

We have not found any disclosure or even a mention by T1 Energy management that T1 had leased a large new warehouse in Q1-2026. We were told that the reason why a material new lease was left undisclosed is that management is trying to hide something.

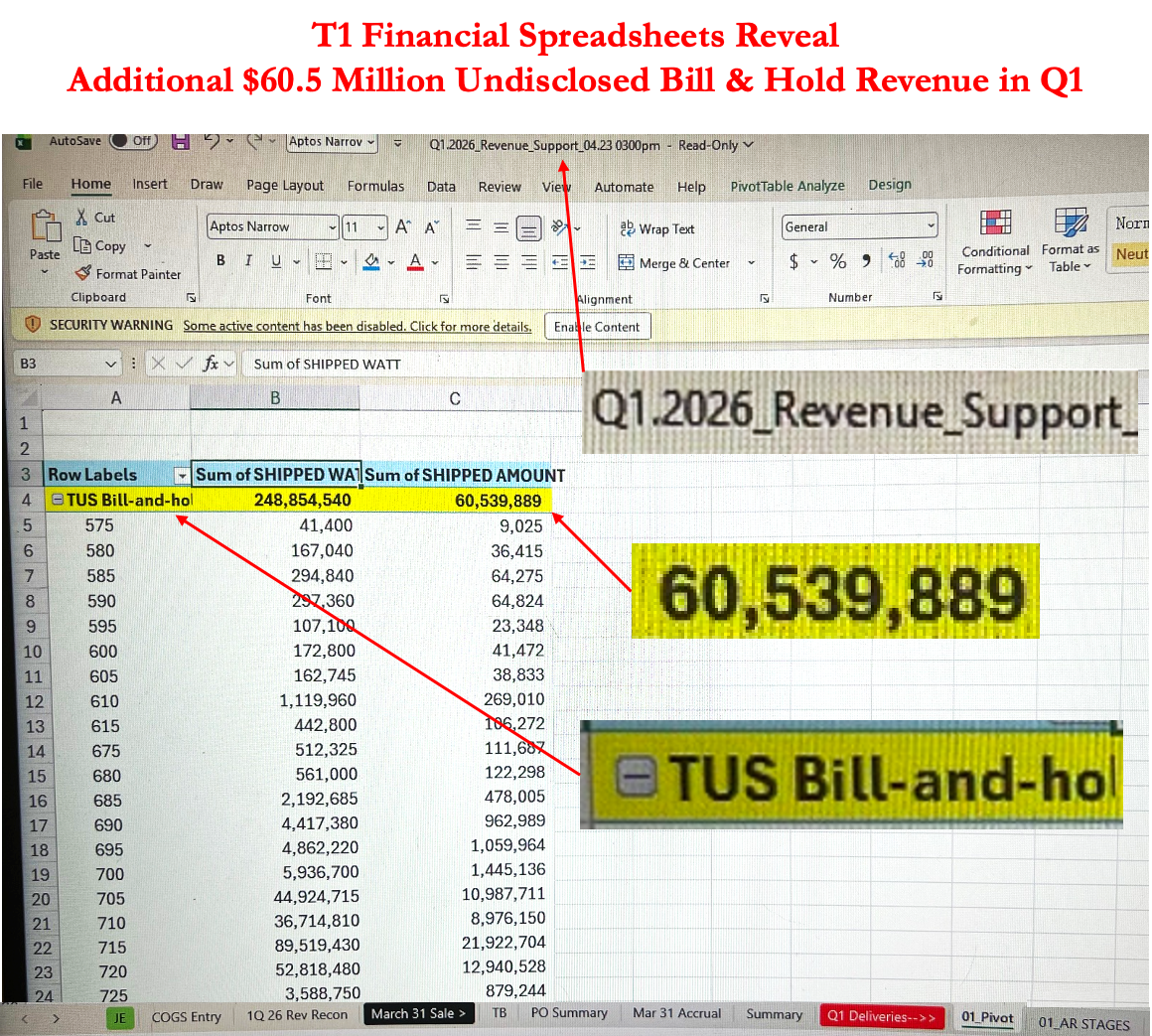

Internal T1 Financial Spreadsheets Reveal Undisclosed Bill & Hold Revenue in Q1-2026

- Was an Est $60.5 Million or 1/3 of Q1 Revenue Stashed in That Warehouse?

The Whistleblower provided us with a T1 internal spreadsheet titled “Q1 2026 Revenue Support.” T1’s financials appear to show that T1 recognized a significant amount of Bill-and-Hold in Q1-2026. Bill-and-Hold revenue is a high-risk accounting method that is frequently associated with financial manipulation. We believe it is best defined as bullshit revenue, because it enables the company to book sales for product that hasn’t been shipped or even paid for.

If the est $60.5 million number is indeed correct, then Bill-and-Hold revenue accounts for ~1/3 of T1 Energy’s Total Q1-2026 revenue.

Note – there was no disclosure by T1 Energy in Q1 filings about additional/remaining Bill-and-Hold revenue outstanding?

It’s our understanding from the whistleblower that “sum of shipped amount,” means amount “shipped to” the “TUS Bill-and-hold” account. Our financial analysis seems to confirm this $60.5 million was new bill-and-hold booked for Q1-2026 because:

- If Q4 Bill & Hold shipped → AR should decrease; AR increased in Q1

- If clearing old Bill & Hold → no need for new warehouse. T1 leased ~420k sq ft

- $60.5M Bill-and-Hold appears in a Q1 revenue support schedule — already-recognized Q4 shipments belong in a logistics tracker, not a revenue reconciliation

- Rising Right-of-Use Lease assets + secret warehouse = physical infrastructure to store modules never actually delivered to customers

Either way, the major questions are the same:

- Is the revenue T1 booked legit if T1 a) hasn’t been paid and b) the finished product is hiding in a nearby warehouse rather than being delivered to the customer?

- If T1 actually had an infinite amount of AI data-center demand…then why the hell does T1 need to stash a lot of finished solar panels in a secret warehouse while pretending, it’s all been sold and delivered?

>$130m of Revenue Added to Q4 in Late Jan-2026

Whistleblower Provided Internal Docs That Reveal Journal Entries Without Proper Documentation:

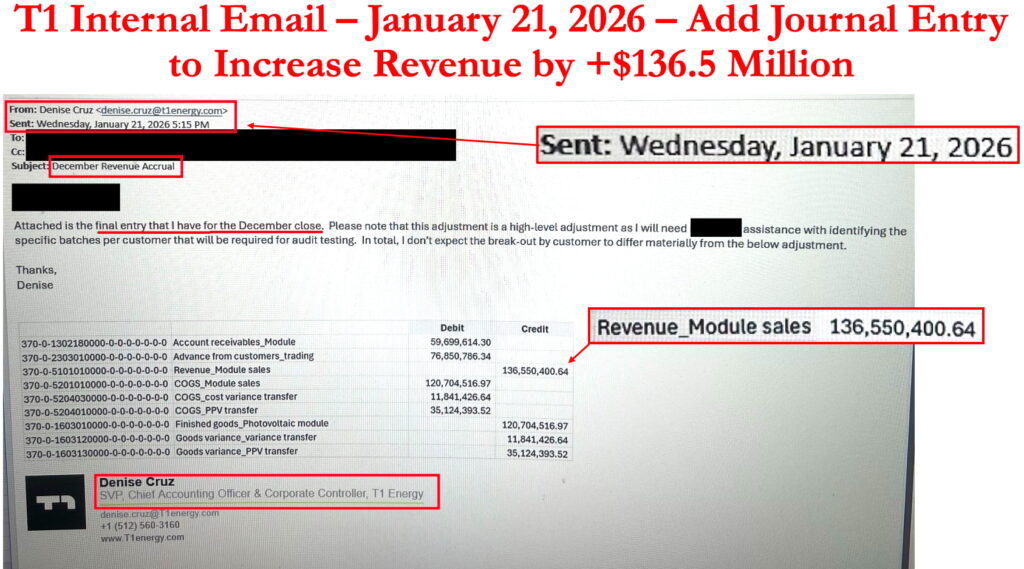

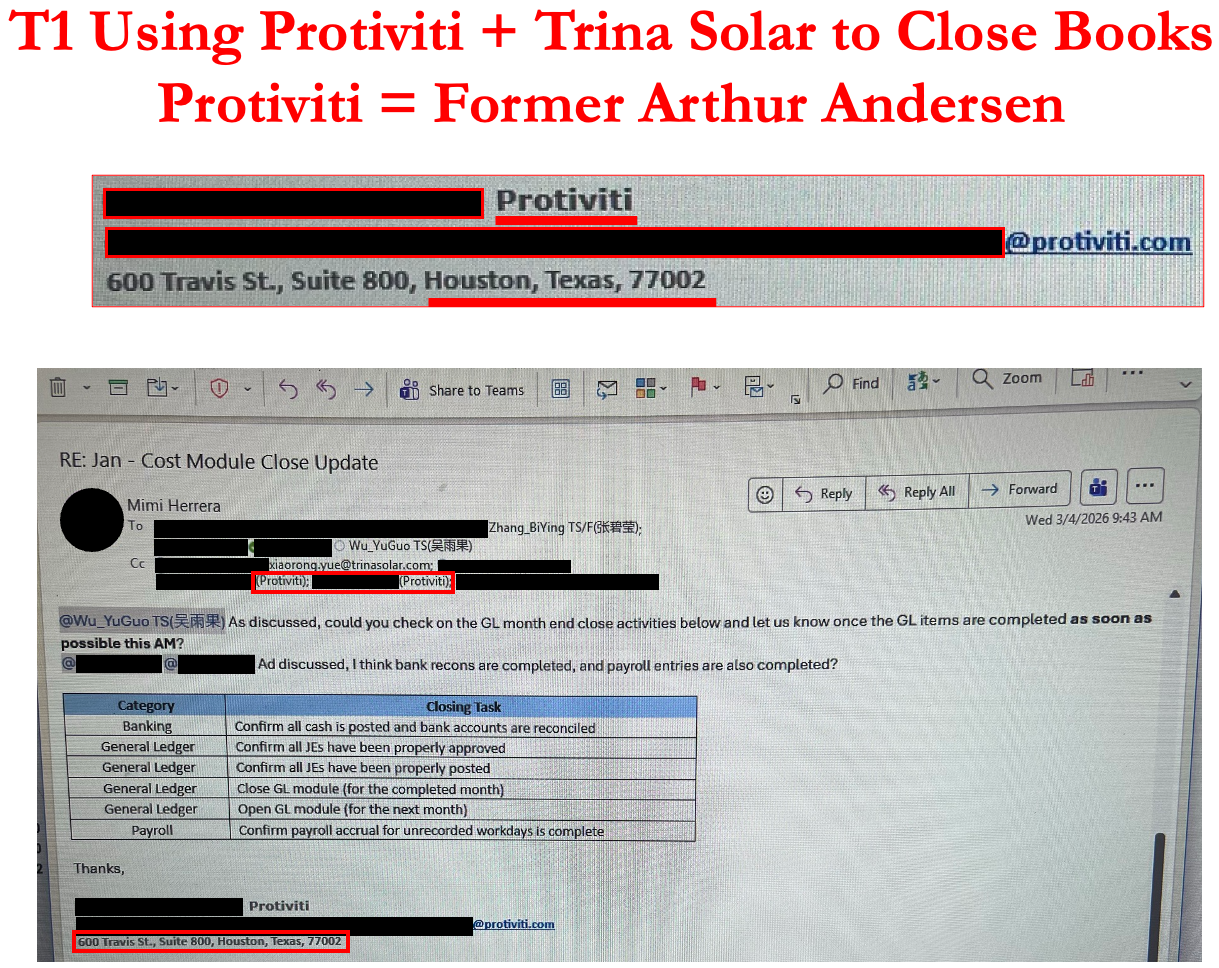

Internal Jan 21, 2026 Email: Add >$130 Million to Q4-25 Revenue

In Q4’25, T1 booked $134.4 million of bill-and-hold revenue from their related party, Trina Solar.

The whistleblower revealed emails requesting large after the fact manual adjustments to the books that were sent by the former Chief Accounting Officer, Denise Cruz, in late January. The whistleblower further explained that they could not find any proper back up documentation for these transactions. On January 21, 2026, T1’s Chief Accounting Officer (at the time) sent an email to the accounting team at G1 to book >$130 million of revenue… 3 weeks AFTER the end of the fiscal year!

The whistleblower told us that in their experience manual adjustments of this size were a huge red flag and they believed this specific entry was an initial estimate of the bill-and-hold revenue that T1 ultimately added to Q4-2025, well after Q4-2025 was done.

The whistleblower explained why this was likely a sign of financial manipulation:

- No documentation for the $136.5m sale was provided – No invoices were provided, instead just an excel spreadsheet with that same $136.5m sales number listed

- This journal entry appeared to be for a new “Bill-and-Hold revenue”

- No separation of duties. Denise (the former Chief Accounting Officer) controlled the AR activity

- Entry was done manually, by an outside consulting firm, called Protiviti – which is not the usual process for booking transactions like these

“That’s not normal to make those larger entries. It should have been accounted for throughout the month or it should’ve been done the normal accounting way” ~T1 Energy Whistleblower

The email clearly states that T1’s former CAO provided the following journal entries as estimates as she didn’t “expect the break-out by customer to differ materially from the below adjustments.” Also, the $136.5 million initial estimate from Denise was fairly close to the $134.4 million that was eventually recognized in T1’s 10-K.

The whistleblower said they are not aware of any supporting documentation for these last-minute journal entries. They also said there is a significant internal control issue that is apparent in this process. T1’s former CAO was the one that created the supposed supporting documentation, journal entries, true ups, and supposedly had no one else check them. Meanwhile the actual people entering the journal entries could NOT verify that they were legit.

“If the person doing the entries is Denise, who else is going to check? She’s doing the entries and the true up. A lot of things, there wasn’t separation of duties to be SOX compliant or GAAP” ~T1 Energy Whistleblower

T1’s Sketchy Journal Entry Processes:

- 3rd Party Consultants – Protiviti – Making Entries

- No Supporting Evidence

- Time Pressure to Rush Entries

- Trina Still has Access & Control over JE’s

“They [T1 Energy] had questionable entries…all the time.” ~T1 Energy Whistleblower

The whistleblower told us that T1 engages in an unconventional method of booking journal entries — T1 often use a 3rd party internal audit consulting firm named, Protiviti, to input journal entries directly into the books and records. They told us that this is not normal and is a significant issue for T1’s financial controls.

“How they’re doing journal entries, like pushing it down from corporate to [Protiviti] and stuff, that’s not normal. And in my opinion, not okay.” ~T1 Energy Whistleblower

The whistleblower suspected the reason why T1 Energy (and Trina Solar) engaged, Protiviti, is because the Protiviti employees were told by their managers to blindly assist T1 in entering the journal entries, even if the entries lacked proper documentation, and thus were potentially false. Apparently, Protiviti management had told members of their staff that if there was any blow-back from false journal entries that Protiviti and it’s employees would be “covered legally,” and since they were protected, the Protiviti consultants should just “do what the client asks.”

We learned that the Protiviti consultants had given up asking that T1 management provide proper back-up documentation for journal entries.

Interestingly enough, it seems that T1 is employing Protiviti consultants from Protiviti’s Houston office. More on that later.

No Support for Journal Entries:

The whistleblower told us that T1’s CFO and Chief Accounting Officer would send large journal entries worth hundreds of millions to Protiviti consultants to be entered into T1’s books & records. According to the whistleblower, these types of major journal entries to T1’s books should NOT be happening from an outside consulting firm, and they definitely should NOT be occurring without management providing the proper support.

“It’s the journal entries that get sent in emails where [T1 Mgmt] is telling [Protiviti people] to move millions of dollars with no support, and [they] have no idea why… The email is the support, or they’ll send it to someone else to book the entry that will cooperate, not ask questions…that made it sketchy” ~T1 Energy Whistleblower

“People don’t just tell you to book entries that you don’t know why or the reasoning behind it. I mean that’s just not normal. And it’s questionable when people ask you to do those. Especially when they’re $150 million entries” ~T1 Energy Whistleblower

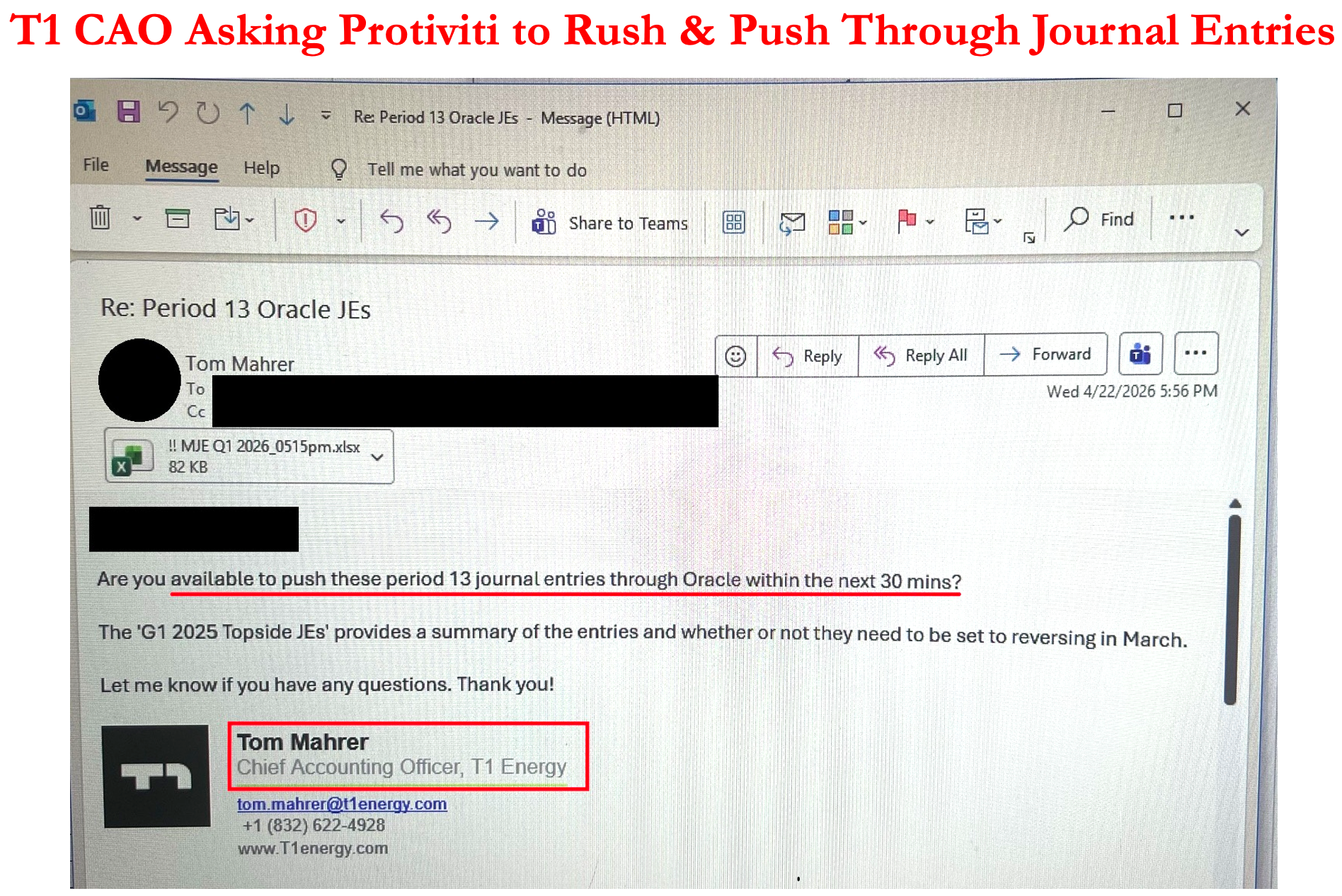

T1 Internal Emails Show Pressure to Rush & Push Through Journal Entries

Emails show that T1 Management would try to use time crunches to create pressure to push through journal entries at the last minute. The below urgent email was sent to a Protiviti consultant about “pushing through 13 journal entries” in “the next 30 min.”

Evidently these types of entries would normally be handled by full-time T1 employees like the controller of the G1 plant.

Notably the email subject is regarding changing “Period 13 JE’s” and the date is April 22, 2026. This shows T1 changing FY 2025 financial journal entries 4.5 months after the end of the year.

“Topside entries should have went to the controller of the plant...since [Protiviti] are consultants, I think they [T1] can say oh well that’s on them” ~T1 Energy Whistleblower

Trina’s Continued Control over T1’s Journal Entries & Financials

Despite T1 claiming to be independent from Trina Solar, it appears that Trina has deep control over T1’s accounting infrastructure. The financial systems, communications, and key processes remain under Trina’s operational authority

“Everything is in Chinese. Like emails, invoices, all that…our accounting system is in Chinese” ~T1 Energy Whistleblower

“Trina built our Oracle to match with their K2 (K2 is Trina software)…until you get the Chinese out of it, we will not know how everything’s being done” ~T1 Energy Whistleblower

“No one that closes the workorders does it, they’re all Trina. They don’t speak English. And it’s a Trina process” ~T1 Energy Whistleblower

Protiviti = Formed Out of Arthur Andersen’s Ashes – Enron’s Infamous Auditor

- Protiviti = Secret Consultants Who Looked the Other Way so T1 Could “Cook the Books”

- Protiviti Lineage = Born Out of the Implosion of Infamous Arthur Andersen’s Internal Audit Biz Right After Enron Implosion

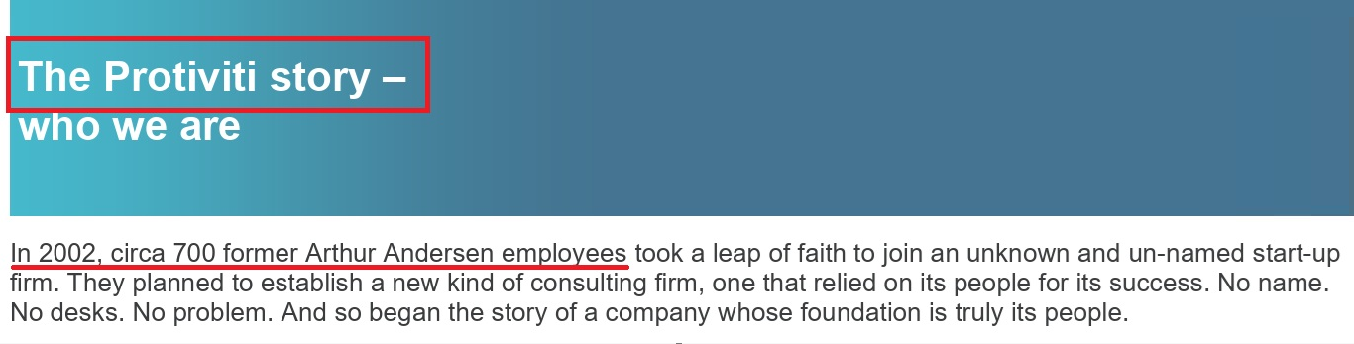

Protiviti consultants are a key component of how T1 is avoiding scrutnity, so it’s important to know Protiviti’s background. Protiviti was literally built straight out of the wreckage of the firm, Arthur Andersen, that enabled the Enron fraud, Arthur Andersen.

In May 2002, Protiviti was founded by former partners and employees from the internal audit & risk divisions of Arthur Andersen. Two months before, in March 2002, Arthur Andersen had been criminally charged by the DOJ for witness intimidation and obstruction of justice in the Enron case. So, 700 Arthur Andersen employees focused on internal audit and risk management jumped off the sinking ship and formed Protiviti. Arthur Andersen was convicted by the DOJ just a month later and the firm officially imploded for their involvement in enabling the Enron fraud.

We were shocked to uncover that the remnants of Arthur Andersen’s internal audit division still actually exist…but less shockingly the Arthur Andersen morals appear to still be alive and well. We learned that Protiviti managers keep asking their employees to look the other way when their clients (like T1 Energy) engage in suspect financial transactions.

Who is Arthur Andersen? Remember Enron?

For most of you we hope this is un-needed, but when we uncovered that Protiviti was born out of Arthur Andersen’s demise our youngest team member (aka “lil’ Panda”) said on an internal meeting “That’s amazing, but who is Arthur Andersen?” We are pretty sure Ben Axler’s heart stopped briefly over at Spruce Point. But anyways, “Lil’ Panda” both made the rest of our team feel very old + caused this brief section on one of the US’s greatest Fraud’s—Enron + Arthur Andersen, Enron’s sketchy auditors and who enabled Enron to persist for years to be penned.

The Big 4 audit firms used to be the Big 5, the 5th one was Arthur Andersen. Arthur Andersen served as both Enron’s external auditor and internal audit provider. Andersen’s negligence and complacency was key to allowing Enron to commit accounting fraud for many years. It led to the implosion of Arthur Andersen, and Enron executives serving real time in prison. Not only did Andersen act as Enron’s external Auditor who blessed Enron’s VIE/SPE structures created to hide Enron’s losses but all the while Andersen’s consulting business earned Andersen an estimated $27M/year.

Protiviti’s Involvement in Another China Hustle – China’s AgFeed

Protiviti, a Robert Half Subsidiary, was also involved in another China Hustle that imploded called AgFeed.

- Protiviti was the trusted advisor and consultant to AgFeed which was charged with Massive Accounting Fraud by the SEC for inflating revenue & asset values

- AgFeed booked ~$239 million of fictitious revenue for hogs that did not exist and created phony invoices

Protiviti’s business skates under the radar because it essentially operates in a regulatory gap that’s basically a no-man’s land. Protiviti is a consulting firm that is not PCAOB nor SEC regulated. Protiviti does some of the same work as auditors do but without legal accountability that comes with being a firm’s auditor.

T1’s Missing 45X Tax Credits – People Internally are Freaking Out – T1’s Insurance Co Isn’t Paying

The whistleblower told us that T1 Energy was expecting to receive cash from the government in mid-April for some of the 45X tax credits T1 booked but didn’t sell. But the money never arrived.

We also learned that internally T1 executives are “freaking out” and recently there have been lots of internal meetings about the tax credits not getting paid out.

“Those tax credits that they all talked about. They were supposed to receive them from the government. And they have yet to receive them. ~T1 Energy Whistleblower

“They expected [45x tax credits] to be around April 15…they’re sweating bullets because they were like we don’t know where we’re going to get money to meet payroll…[T1 Management] is really freaking out about it” ~T1 Energy Whistleblower

We learned that “Euclid insurance is not paying out [on T1’s 45x tax credits].”

The whistleblower informed us that T1 had bought insurance on the 45X tax credits from Euclid Transactional. Internally, a senior T1 Treasury employee, has been telling staff that Euclid has NOT been paying out T1’s tax credit insurance and is refusing to cover T1’s losses, and that this a major problem.

“There’s a hold up with insurance regarding the tax credits…there is an issue we are having, with insurance.” ~T1 Energy Whistleblower

Note – we are not sure the exact reason why Euclid has not been covering T1’s missing 45X tax credits but we presume it is to do with FEOC risk. But it’s possible the missing tax credits could also be related to the additional FY 2025 bill-and-hold 45X tax credits that T1 Energy has been unable to sell. Both possibilities make sense…both would mean that T1 needs to make a major accounting restatement.

Potential Accounting Fraud Flagged to KPMG

“[T1 Energy] had questionable entries all the time.” ~T1 Energy Whistleblower

Accounting Fraud Reported to KPMG – T1 Saved After a Protiviti Manager Coached the Person to Walk Back their Statement:

We learned from the whistleblower that everyone inside T1 Energy was shocked that T1 Energy passed their FY 2025 KPMG audit.

“Everyone was like we’re not going to pass this [audit]. We are not going to pass this. …then low and behold we passed…we cannot believe that we passed this audit. No one thought we were going to pass the audit at all” ~T1 Energy Whistleblower

Apparently, KPMG had sent out a survey to all internal T1 Energy financial employees and the Protiviti employees. The KPMG survey asked questions like.

- Are you aware of any inappropriate or unusual activity related to processing of journal entries? – Check Yes or No

- Are any journal entries or other adjustments recorded without adequate support or explanation? – Check Yes or No

- Were there any instances of management overriding controls, recording journal entries, or other adjustments? – Check Yes or No

The whistleblower told us that apparently one of the Protiviti consultants checked Yes to all the above questions and informed KPMG that fraud was possibly occurring at T1. People inside T1 thought the company “was cooked” – “KPMG would find out everything” and the house of cards would all fall down on top of them.

The whistleblower told us they had spoken with the Protiviti employee who reported likely fraud to KPMG. Apparently, the only way that T1 Energy was saved was that a Protiviti manager intervened and was able to coach the consultant to adjust their story. The manager convinced/coerced the consultant to change their mind and downgrade their own statements from “fraud has occurred” to “it’s possible fraud is occurring” and that it was impossible for them to truly know from their position.

T1’s Financial Professionals That Ask Questions Are Shown The Door

We learned from the whistleblower that a large number of T1 financial professionals have questioned the accounting internally. We were told that raising questions results in people getting fired and paid a large severance with NDAs to silence them.

“He’s [Dan Barcelo] surrounded by ‘yes men.’ No one will tell him no. And if you do, you get fired” ~T1 Energy Whistleblower

Chief Accounting Officer – For example, in February, T1’s former Chief Accounting Officer, Denise Cruz, was fired. Unlike most terminations for public companies, Denise’s was missing a key detail. Nowhere in the 8-K does it state the termination wasn’t due to any disagreements. The whistleblower told us Denise was paid a hefty severance package with NDAs attached. The whistleblower thought it was to get her to keep quiet about what Denise saw going on within the company.

T1’s G1 Plant Controller – Another example, in February, T1’s Plant Controller at G1, Rusty Williams, was also fired February 2026 and apparently also paid a severance package to keep quiet.

“[T1 Management] set Denise and Rusty up to be the fall guys” ~T1 Energy Whistleblower

The whistleblower told us multiple other members in the accounting department left recently and they believed that all these individuals got fired for bringing up issues with the accounting.

Protiviti Consultants “Wanting to Quit Left and Right”

The whistleblower told us that Protiviti employees that asked questions or who did not do as they were told by T1’s management, were either reassigned or fired. They said that T1 had probably gone through more than 8-10 of the Protiviti consultants in just the last year.

“I’m not lying when I say the consultants are just wanting to quit left and right. ~T1 Energy Whistleblower”

When Protiviti employees asked T1 employees for documentation T1 would just tell them:

“The email is the support, [book it] or [we will] send it to someone else to book the entry that will cooperate, not ask questions.”

Whistleblower(s) Revealed T1’s Books Are NOT Accurate – It’s Time to Make your Own Conclusion

The whistleblower has provided emails, financial statements, internal records, and a copious amount of detail about T1 Energy’s books being inaccurate. We believe management is clearly hiding the truth about the financials from investors.

“Our accounting, if you were to pull our books, are not accurate. I can 100% tell you today they’re not accurate.” ~T1 Energy Whistleblower

The whistleblower told us that they didn’t think the type of stuff they saw going on with T1’s accounting should be happening at a publicly traded company. We agree.

“T1 [Energy] is a shell…It’s a fugazi. You know, Wolf of Wall Street. Everyone [internally] knows what it is. And everyone jokes about it.” ~T1 Energy Whistleblower

We think T1 Energy has been caught red-handed. Now you know about shipments to a secret nearby warehouse, the internal details from the whistleblower about how T1 is allegedly manipulating their financials, and the missing 45X tax credits.

Make your own conclusion. We are short T1 Energy because we believe they are FEOC’ed.

Fuzzy Panda Research is Short T1 Energy (TE)

Fuzzy Panda Research Disclosures, Disclaimer and Terms of Service:

By downloading from or viewing material on this website and/or by reading this report, you agree to the following Terms of Service. You agree that any use of the research in this report or on this website is at your own risk. In no event will you hold Fuzzy Panda or any affiliated party, including officers, directors, employees, consultants, and agents of Fuzzy Panda or any companies affiliated with any of them, liable for any direct or indirect losses caused by your use of or reliance on information on this site or in this report. You further agree that you will not rely on any information in this report or on this website, to do your own research and due diligence before making any investment decision with respect to companies or securities mentioned herein, and that you will consult with your own investment professionals prior to any investment decisions. You represent that you have sufficient investment sophistication to critically assess the information, analysis and opinions in this report or on this site. You further agree that you will not communicate the contents this report or other materials on this site to any other person unless that person has agreed to be bound by these same Terms of Service. If you accessed, download, or receive this report or the contents of other materials on this site as an agent for any other person, you are binding your principal to these same Terms of Service.

As of the publication date of this report, Fuzzy Panda, and possibly any companies affiliated with it or its members, partners, employees, consultants, clients and/or investors (the “Fuzzy Panda Affiliates” – although as of the date of this report we do not know what, if any, positions the Fuzzy Panda Affiliates hold), have a short position in the stock (and/or options, swaps, and other derivatives related to the stock) and bonds of the company covered in this report (the “Covered Company”). Some of the Fuzzy Panda Affiliates possibly could even hold current positions that are contrary to Fuzzy Panda’s position as they were not aware of the contents of this report. Fuzzy Panda and potentially the Fuzzy Panda Affiliates therefore stand to realize significant gains in the event that the prices of either equity or debt securities of the Covered Company declines. There are many factors that can go into a decision to cover the short position(s) in the Covered Company’s securities and it is not possible to predict exactly when or for exactly what reasons Fuzzy Panda and the Fuzzy Panda Affiliates may cover their positions, in whole or part, or otherwise change their investment holdings. As a general matter, Fuzzy Panda and the Fuzzy Panda Affiliates intend to cover some or all of their positions at a time that the price of the Covered Company’s securities are lower than when they were sold short or otherwise invested in. Fuzzy Panda and the Fuzzy Panda Affiliates may cover some or all of their short positions immediately after the publication of this report or an indefinite period after its publication. Similarly, Fuzzy Panda and the Fuzzy Panda Affiliates may cover some or all of their short positions if the price of the Covered Company’s securities move a small amount or after moving a larger amount. Fuzzy Panda and the Fuzzy Panda Affiliates intend to continue transactions in the Covered Company’s securities for an indefinite period after the publication of this report, and they may be short, neutral, or long at any time after the publication of this report regardless of any opinions, possible stock prices or valuations, or other views stated in the report. Fuzzy Panda will not update any report or information on this website to reflect any changes in the investments of Fuzzy Panda or the Fuzzy Panda Affiliates that existed at the time of the publication of this report, or any new positions in any securities of the Covered Company.

This report and the Fuzzy Panda website is informational and describes the opinions of Fuzzy Panda. This report is not an offer to sell or a solicitation of an offer to buy any security, and Fuzzy Panda does not offer, sell or buy any security to or from any person through this report or the Fuzzy Panda website. This report is not a recommendation or advice to short or otherwise invest in or trade any security. Fuzzy Panda does not render investment advice to anyone unless it has an investment adviser-client relationship with that person evidenced by a formal written agreement. You understand and agree that Fuzzy Panda does not have any investment advisory relationship with you, or owe any fiduciary or other duties to you. Giving investment advice requires knowledge of your financial situation, investment objectives, and risk tolerance, and Fuzzy Panda has no such knowledge or information about you.

If you are in the United Kingdom, you confirm that you are accessing research and materials as or on behalf of: (a) an investment professional falling within Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “FPO”); or (b) high net worth entity falling within Article 49 of the FPO.

Fuzzy Panda’s research and reports express the opinions of Fuzzy Panda, which are based upon generally available information, field and online research, and inferences and deductions through due diligence and the analytical process. Fuzzy Panda believes that all information contained in this report has been obtained from accurate and reliable public sources, and no material nonpublic information was obtained from any person who had a duty to keep information confidential. However, Fuzzy Panda cannot be certain that the information it has relied upon in this report is accurate. The information and opinions in this report are therefore presented “as is,” without warranty of any kind, whether express or implied. Fuzzy Panda makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. This report also contains forward looking statements about what may occur in the future. The future cannot be predicted with certainty and any of the forward-looking statements about projections, beliefs, estimates, assumptions, outcomes, or any other future event may be incorrect. Among other things, any forward-looking statements may be rendered inaccurate by incorrect assumptions, incorrect methodologies, unforeseen risks and events, or other variables. Any opinions about the possible future stock price of the Covered Company or fair value of its securities is not a price target and does not mean or imply that Fuzzy Panda or the Fuzzy Panda Associates will hold any investment until such price or valuation is met. Further, all expressions of opinion, including any conclusions drawn from Fuzzy Panda’s analysis, are subject to change without notice, and Fuzzy Panda does not undertake to, and will not, update or supplement any reports or any of the information, analysis and opinion contained in them.

You agree that the expressions of information in this report are copyrighted and owned by Fuzzy Panda Research, and you therefore agree not to distribute this report, any excerpts from it, or information from the Fuzzy Panda website (whether the downloaded file, copies / images / reproductions, or the link to these files) in any manner other than by providing the following link: www.fuzzypandaresearch.com. If you have obtained Fuzzy Panda’s research in any manner other than by accessing or downloading from that link, you may not read such research without going to that link and agreeing to the Terms of Service. You further agree that any dispute between you and Fuzzy Panda and/or any of the Fuzzy Panda Affiliates arising from or related to the material on their website shall be governed by the laws of the State of California, without regard to any conflict of law provisions. You knowingly and independently agree to submit to the personal and exclusive jurisdiction of the state and federal courts located in California and waive your right to any other jurisdiction or applicable law. The failure of Fuzzy Panda to exercise or enforce any right or provision of these Terms of Service shall not constitute a waiver of such right or provision. If any provision of these Terms of Service is found by a court of competent jurisdiction to be invalid, the parties nevertheless agree that the court should endeavor to give effect to the parties’ intentions as reflected in the provision and rule that the other provisions of these Terms of Service remain in full force and effect, in particular as to this governing law and jurisdiction provision. You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to this report or the material on this website must be filed within one (1) year after such claim or cause of action arose or be forever barred.