Foresight Autonomous Holdings, (FRSX – US), claims to be changing the world of autonomous driving technology.

In reality, FRSX, an Israeli RTO, is nothing more than an aggressive stock promotion where insiders are siphoning cash to entities they control. FRSX was formerly controlled by a convicted felon before Kfir Silberman and Itschak Shrem took over. Shrem & Silberman are a duo of notorious penny stock promoters one of whom was arrested on suspicion of money laundering. The company is still under the influence of the duo who receive financial advisory fees and support from the current FRSX CEO.

After examining the full cast of characters at Foresight, we discovered connections to accused money launderers, convicted felons, numerous penny stock promotions, and financiers who have settled SEC charges of market manipulation.

Foresight Autonomous’ CEO also funnels cash from FRSX for himself to an entity he and his brother-in-law wholly control under the guise of R&D spending.

We are Short Foresight Autonomous (FRSX) and see material downside and expect this reverse-merger penny-stock promotion to collapse back to below $1 for the following reasons:

- FRSX’s cap table is littered with accused & convicted criminals.

- Insider Enrichment via egregious related party “service agreements” which allow FSRX’s CEO and the known penny stock promoters to siphon cash out of the company.

- Founding shareholders, members of the Board of Directors, and FRSX’s CFO have been involved in at least ten other stock promotion schemes. Insiders got paid but shareholders got fleeced.

- FRSX is a family affair. The new CTO is actually the CEO’s Brother-In-Law. The CEO’s daughter, is their legal advisor and VP of HR. His daughter has also received generous share grants including free extensions of expiring options despite being a part-time employee.

- Round-trip financing – shareholder capital is paid out to a party connected to Silberman – then a smaller amount is funneled back to FRSX through new financings (minus a % fee?).

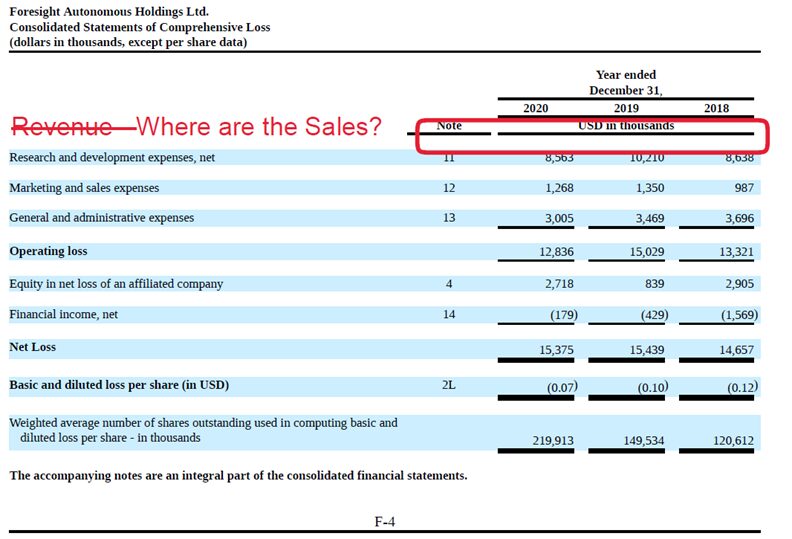

- FRSX announces what appears to be “fictitious sales” in press releases. Their lawyers and accountants corroborate that these are not real sales as the financials show $0 in GAAP revenue.

- We uncovered that FRSX’s pays for its technology “awards.”

- Failed attempts at monetizing its subsidiaries via another RTO and a failed Nasdaq IPO.

- Its technology is old and dated. We found evidence that FRSX management is essentially recycling 7-year-old marketing videos from its major shareholder and then portraying it as current breakthroughs.

- FRSX does not develop any hardware of its own. Despite the fancy marketing materials, their hardware is merely off-the-shelf.

- FRSX’s purported Elbit Systems partnership is not as advertised. Management claims that the Elbit contract is worth tens of thousands and that Elbit purchased software licenses, but this never came to fruition.

- Significant selling pressure – FRSX is currently dumping stock on the open market in a very dilutive at-the-market offering and still has $46m left to sell. (pg 49)

Disclosure: After extensive research, we have taken a short position in Foresight Autonomous Holdings. This report represents our opinion, and we encourage every reader to do their own due diligence. Please see our full disclaimer and terms at the bottom of the report

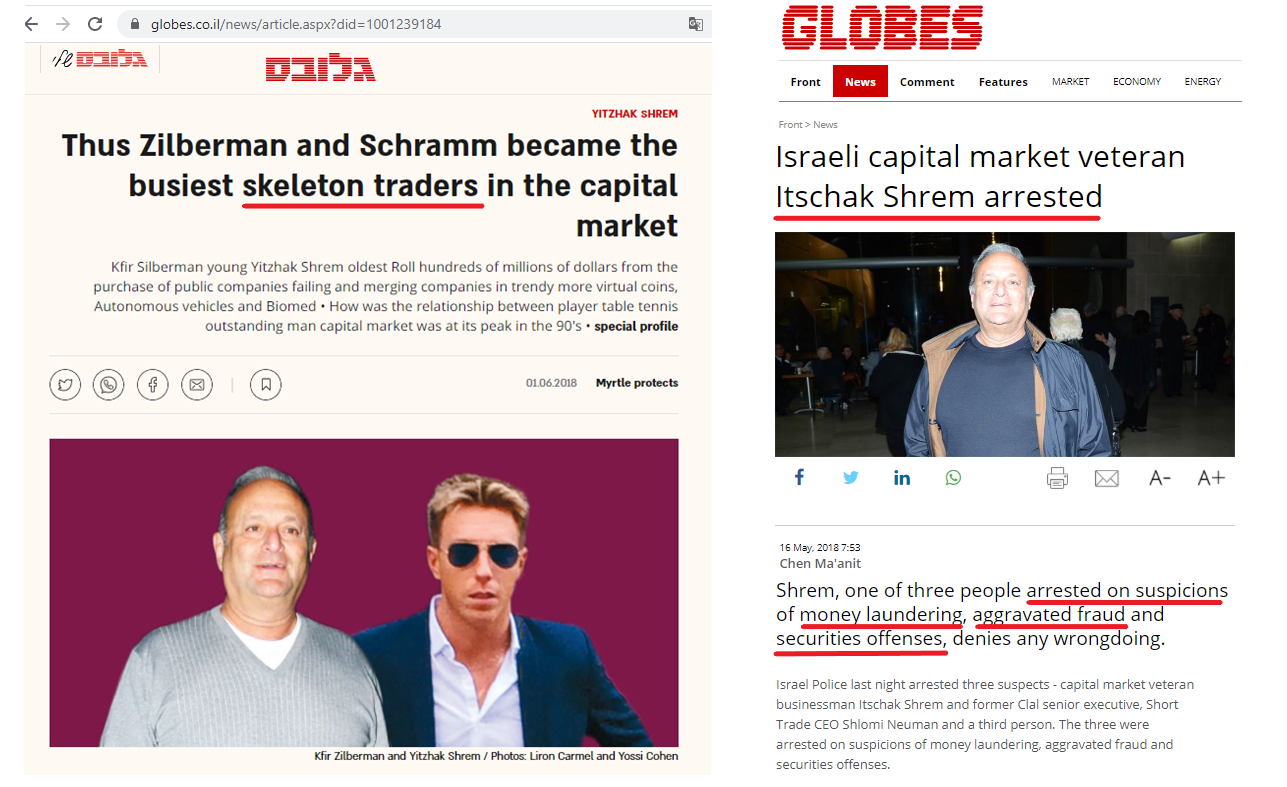

Foresight Autonomous Group’s History – Israeli Reverse Takeover; A Convicted Felon; and the “Skeleton Traders” Including an Accused Money Launderer

Foresight Autonomous (FRSX) is an Israeli RTO (reverse takeover) that was formed when Magna BSP “sold” (RTO’d) their Foresight Automotive Subsidiary into a shell company, Asia Development Ltd. The shell was controlled by the duo of Kfir Silberman & Itschak Shrem. Silberman & Shrem are best known as the “Skeleton Traders” by local media and Itschak Shrem became infamous after his 2018 arrest on suspicions of money laundering, aggravated fraud, and securities offenses. The “Skeleton Trader” nickname for the duo came from the multitude of dying shell companies Silberman & Shrem have purchased and reverse merged with trendy promotional ones. They have a consistent pattern of enriching themselves while retail shareholders pay the price.

Before Foresight was Asia Development Company and controlled by the “Skeleton Traders,” it was known as Golan Melachat Machasvat (20-f pg 19) which was controlled by Oded Dessau, who was convicted of fraud and theft from the company. Dessau served time in prison for this fraud.

Silberman & Shrem, the “Skeleton Traders,” are still deeply involved in Foresight. The Foresight CEO is even publicly quoted referring to them as both as friends and great colleagues:

“…they complement each other. I call the connection between them, a connection of Noah’s Ark. Why Noah’s Ark? Because it’s a great pair, when the young man brings a temperament with him, and the adult brings a calm, capable, connected with him. Kfir is frantic, wants to “burn” the world, and Itsack Shrem brings the experience and the connections…(later)…I will definitely work with [Silberman] again.”

~Haim Siboni, CEO of Foresight Autonomous Group (Article translated from Hebrew)

Organizational Structure – Foresight has been in the autonomous vehicle space since 2011 and in that time has generated ZERO Revenue and has ZERO Auto OEM Partners/Investors.

Foresight’s Business consists of 2 fully owned “autonomous vehicle products/divisions” and a minority position in Rail Vision. Silberman-Shrem have already tried and failed to spin off Eye-Net Mobile into a reverse merger (May 2018) and failed at completing a Nasdaq IPO for Rail Vision (Nov 2017).

- Quadsight Vision System (a 4-camera stereo-vision system for cars) – 100% owned

- Eye-Net Mobile (a cellular collision avoidance system) – 100% owned

- Rail Vision Ltd. (minority shareholder in with a 19.34% stake, 16.5% fully diluted) – (link) RailVision is another Silberman & Shrem company (link here to Israeli corporate registry)

The only thing Foresight sells is their own stock and lots of it. Then they direct the cash proceeds, through “services agreements” to 3rd party entities controlled by insiders.

Insider Enrichment 101 – Egregious Consulting Fees to Related Parties; Fundraising Fees; Round-Trip Financing

We discovered that FRSX’s CEO, Haim Siboni and Kfir Silberman are enriching themselves via payments to 3rd party entities they control—Magna B.S.P., Pure Capital (L.I.A.) and the Shrem Zilberman Group. In total FRSX has paid out over $6.7 million in cash and issued >$8.5 million worth of shares to these related parties. We uncovered:

- “Services Agreements” that send large monthly payments to these related parties.

- “Finder’s fees” for investor introductions.

- Free Stock for Nothing. Options & shares issued which get reset and extended if they are underwater.

Will FRSX’s recently raised >$50m cash be directed to related parties too? We think so. As FRSX’s history of insider enrichment shows what will likely happen next.

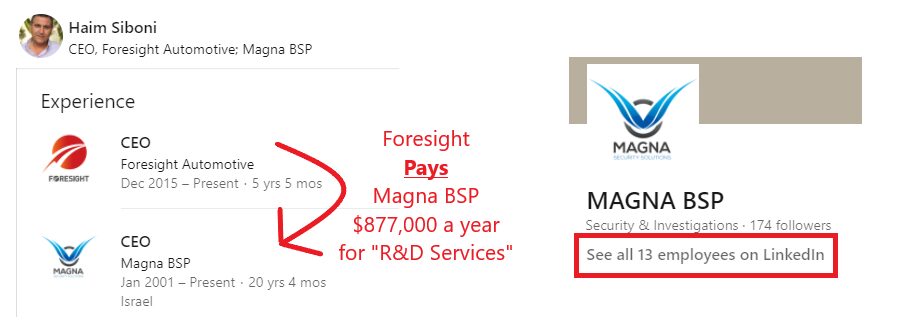

How the CEO Funnels Money Out of FRSX – Magna BSP – A Controlled Related Party

Magna B.S.P. is controlled and run by FRSX current CEO, Haim Siboni (LinkedIn) and Haim’s Brother-in-Law Levy Zruya (LinkedIn). Magna owns 11.1% of FRSX’s shares.

- Large Monthly R&D Payments – Magna receives monthly service payments that are booked as R&D expense (SEC filing – pg F-14). These payments have occurred since 2016 and are currently costing shareholders $877,000 a year for “software R&D services.” However, Magna has only 1 software programmer and 13 employees on LinkedIn. It seems highly unlikely that Magna is an essential software developer for anyone.

- $8.5 million of Free Shares – Magna BSP “employees” have received free options currently worth $8.5 Million. Due to foreign filer rules, insiders get to dump stock onto to the market without clear disclosure to the market since Form 4s are not filed.

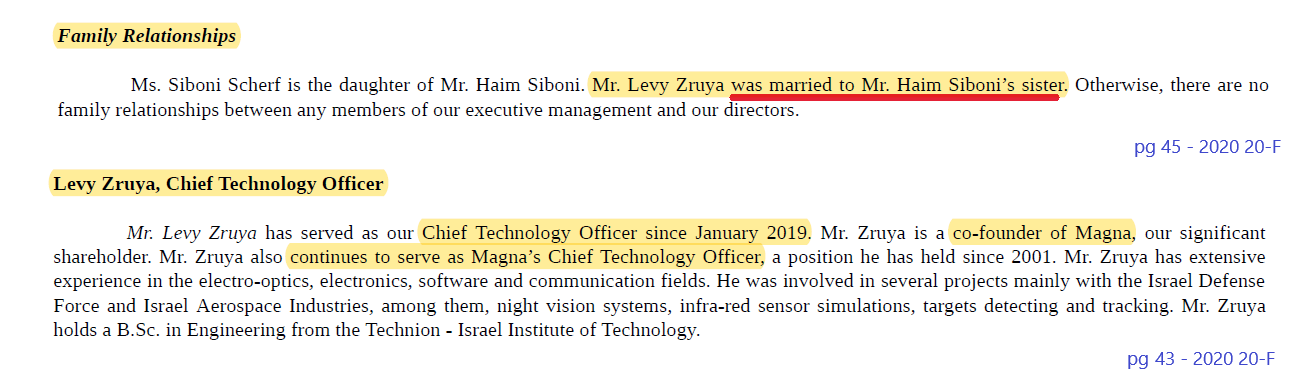

- Brother-In-Law as the New CTO – Magna’s only other executive officer and a beneficiary of these related party cash outflows happens to be Haim Siboni’s Brother-in-Law (pg 45). Levy Zruya (LinkedIn) became FRSX’s CTO in Jan 2019.

“Mr. Levy Zruya was married to Mr. Haim Siboni’s sister”

- Liabilities Shifted onto FRSX – Magna began being paid out day 1 having FRSX assume a $661,000 debt obligation to the Israel Innovation Authority. (20-f pg 18)

- Part-time CEO? – Haim Siboni is only required to spend 80% of his time working for FRSX (employment agreement pg 2)

Without FRSX capital, Magna BSP would be long extinct. Magna BSP was founded back in 2001 and had only raised ~$2m of outside funding ~40% of which came as the Israeli government grant that had its repayment shifted onto FRSX Haim Siboni, Magna’s CEO claims that Magna’s technology protects Israeli borders but that seems hard to believe. We highly doubt that a company with minimal amount of engineering support and an inability to raise capital is responsible for protecting Israeli borders.

How the “Skeleton Traders” Really Get Paid – Funding & Consulting Fees to Pure Capital and The Shrem-Zilberman Group

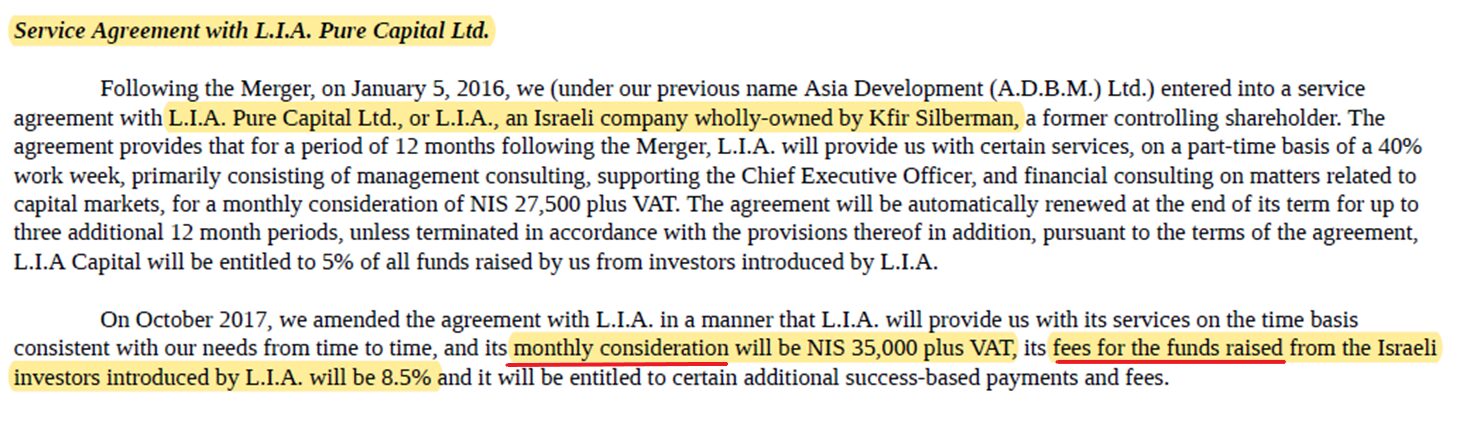

Pure Capital (aka L.I.A) is wholly controlled entity by Kfir Silberman, one of the “Skeleton Traders.” Silberman began getting payouts from FRSX shareholders the moment it went public via a FRSX repaying loan of Silberman’s for $833,320 when the RTO closed (pg 56). The payments haven’t stopped since.

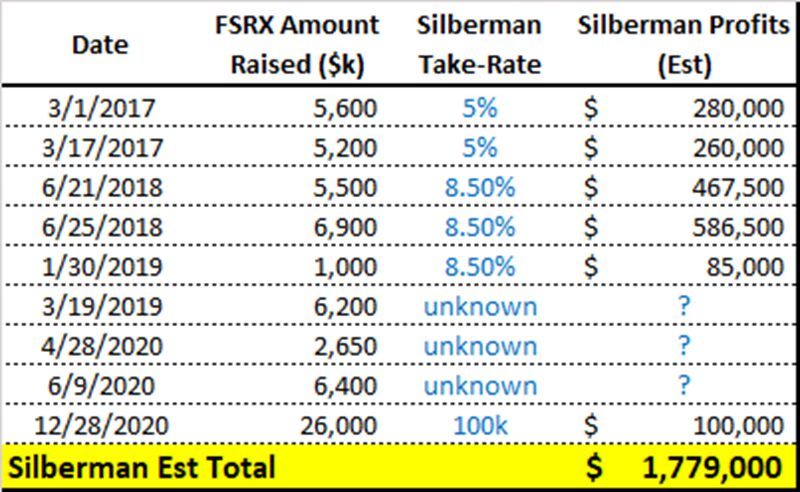

- “Fundraising Fees” – An estimated $1,800,000 of FRSX shareholder money was redirected to Silberman via Pure Capital which was paid as “fees for funds raised.” Disclosures show that Silberman had agreements to receive as much as 8.5% of all funds raised from Israeli Investors (increased from 5% in 2016).

- Monthly Payments –Silberman (via Pure Capital) also receives 35,000 NIS a month so ~$125,000 a year since 2017 (2019 20-f pg 57). This was also increased in 2016 from NIS 27,500 at the time of the merger. See Appendix for full excerpt of agreement.

- Silberman Still Deeply Involved – In the Dec 2020 offering (pg S-13), FRSX’s disclosure states “I.A. Pure Equity Ltd., an entity owned by Kfir Silberman, acted as our financial advisor for the offering and was paid $100,000 for its services.”

Shrem Zilberman Group – An investment company controlled by Itschak Shrem & Kfir Silberman’s.

- Led fundraising rounds for Foresight (March 2017)

- Led fundraising rounds for Foresight’s RailVision Subsidiary (April 2017). Itschak Shrem is also a board member at RailVision.

Round-Trip Financing to An Entity Connected with Silberman – Paying Out $1.25m to Only Get $1m Back

- RH Electronics – Received a development services contract for $1.25m and after that they invested $1 million into FRSX equity. Note – we are unsure whose pocket the missing $250,000 ended up in.

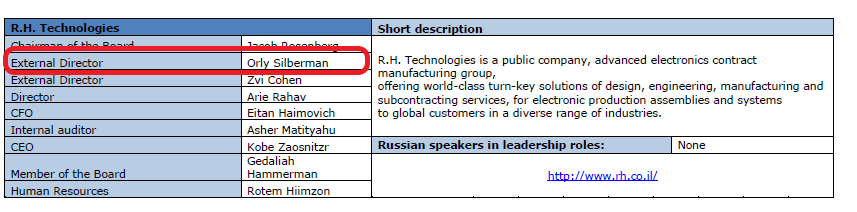

- We uncovered documents showing Silberman has a hand in controlling RH Electronics via a likely relative, Orly Silberman, who is a director of RH Electronics (RH Board on pg 69)

- Note – Israeli company record searches list 2 RH Electronics entities RH Assets Electronics Ltd – 512967043 and RH Technologies – 512970534 and both are controlled by the same individuals.

- We uncovered documents showing Silberman has a hand in controlling RH Electronics via a likely relative, Orly Silberman, who is a director of RH Electronics (RH Board on pg 69)

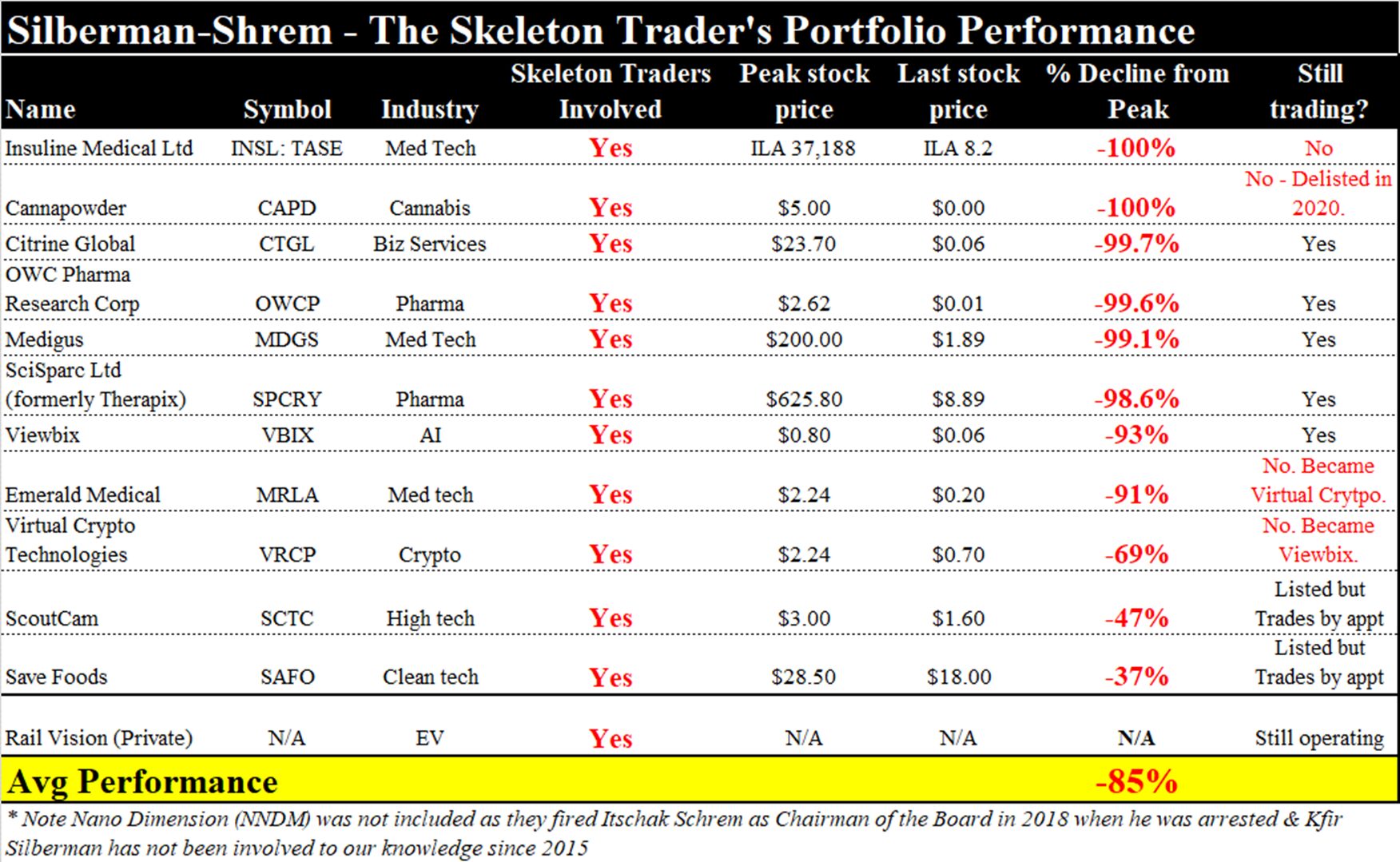

A Skeleton Trader’s Past Performance: Average Decline of > 85%

We discovered over 10 penny stocks that Silberman-Shrem and their team of proxies have been involved in throughout the years and on average investors lose >85% from peak valuations. We doubt this time will be different for FRSX shareholders.

Based on their history of controlling public shells and using them as a personal piggy bank it is not surprising that Silberman-Shrem had already tried and failed to reverse merger or IPO Eye Net (May 2018) and Rail Vision (Nov 2017).

Keeping It In The Family – Who’s Letting Them Get Away with It?

An essential step of funneling funds out of a public company via “service agreements” and R&D contracts is to have loyal friends in place who were hand-picked.

The CEO’s Daughter!

Yes, there are more family members beyond the CTO/Brother-In-Law! We discovered that another senior executive is actually the CEO’s daughter. Sivan Siboni Scherf, the in-house legal advisor & VP of HR(Profile), is Haim Siboni’s daughter. Despite only being 34 years old and working “part-time” (pg F-59) Miss Siboni is one of eight named FRSX senior executives along with her uncle the new CTO.

We also discovered that in 2020 the company extended the exercise dates for options set to expire worthless for the CEO’s daughter (worth ~$800,000) the CEO (currently worth ~$25,000,000), and Magna BSP (worth ~$5,000,000) for free. Additionally, Mrs. Siboni recently received an additional 700,000 options (currently worth $3,300,000). Pretty great gift for a part-time employee.

It’s good to be part of the Siboni Family at Foresight Autonomous.

FRSX’s CFO – Eli Yoresh the current FRSX’s CFO is also only a part-time employee (pg 59) but a full-time Silberman loyalist and one of the “Skeleton Traders” most trusted associates. Previously, Yorseh was CFO of the Silberman controlled reverse-merger shell for years before it became FRSX. Yoresh has also been involved in many of Silberman’s prior stock promotions as either a C-suite employee or a board member. We discovered Yoresh involved in Silberman backed companies across a wide variety of industries—cannabis, crypto, medical, clean tech, and an AI company.

A public company that was defending itself against both Itschak Shrem and Eli Yoresh being installed as board members by Silberman (Pure Capital) put it best in their proxy:

“Two of Pure Capital’s leading candidates (Shrem & Yoresh) have a negative track record of eroded value in companies they have been involved with.”

~Bos Better (BOSC) Proxy

Board of Directors that was Hand-Picked by those Enriching Themselves – 50% from Silberman-Shrem and 50% from Magna BSP

Unsurprisingly, 100% of the FRSX directors are connected to one of the groups that are enriching themselves at FRSX’s shareholders expenses. Four are connected to the Silberman-Shrem (the “Skeleton Traders”) and four are connected to Magna BSP.

Directors Appointed & Connected to Silberman-Shrem

- Zeev Levenberg – A Silberman appointed Director who joined the Board back in 2011 when it was the shell company controlled by Silberman

- Verad Raz Avayo – Connected to Silberman by serving as a Director for at least four other Silberman companies (Save Foods, Apollo Power, Safe-T Group and Tamda Ltd).

- Daniel Avidan – Connected to Silberman via multiple companies. Daniel was the Former CEO of Sapir Corp where Silberman’s likely relative Orly Silberman is a director and the Former CFO Ablon Group Ltd which is connected to Silberman via its CEO.

- Eli Yorseh – CFO & Director – Appointed by Silberman with numerous board seats at his companies and was CFO of predecessor company, Asia Development Ltd.

Directors Connected to Magna BSP

Foresight Automotive’s other 4 directors (Michael Gally, Shaul Gilad, and Ehud Aharoni, and Haim Siboni) were chosen by Magna BSP which is controlled by Haim Siboni.

“As part of the foregoing merger agreement, Magna was provided with the one-time right to nominate the following four directors: Mr. Haim Siboni, Mr. Michael Gally, Mr. Shaul Gilad, and Mr. Ehud Aharoni.” (2019 20-f pg 56)

We are certain that a CEO who has installed his brother-in-law and daughter in senior executive roles selected fiercely loyal directors for his 4.

Faking It Without Making It – ZERO Revenue but Press Releasing “Sales” for Prototype Give-aways Anyways?

Foresight has press released, over the last 5 years, 12 QuadSight “sales”. Management quantifies these purchases as tens of thousands of dollars during investor conferences. Their financials, however, tell a very different picture. Foresight has generated NO REVENUE despite a deluge of press releases claiming “sales,” “purchases,” and even announcing “expected revenue.”

Could Foresight just be sending out misleading press releases & presentations to hype their stock? Every data point we came across would suggest this is precisely the playbook.

“Sale” + “Purchase” = No Revenue – May 2020 German Sale

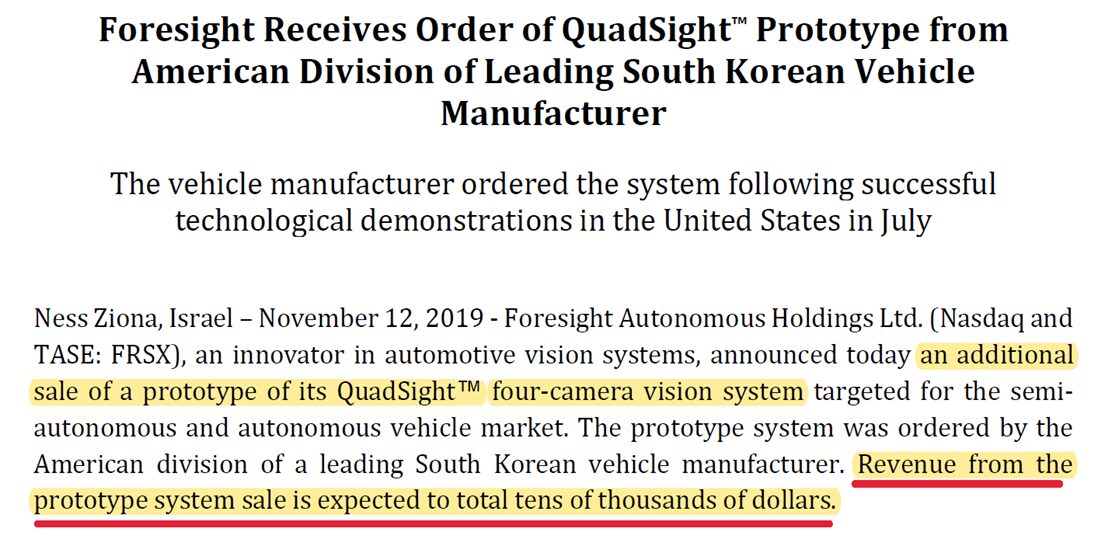

“Sale” with “Expected Revenue” = No Revenue – Nov 2019 – Korean Manufacturer

“Sale” with “Expected Revenue” = No Revenue – Nov 2019 – Korean Manufacturer

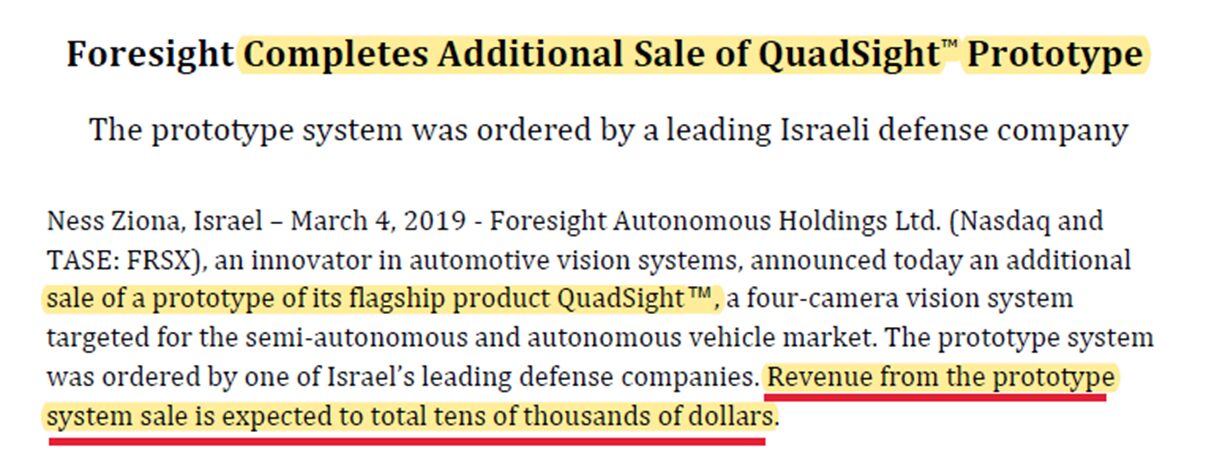

More “Sales” with “Expected Revenue” = No Revenue! – March 2019 Israeli Defense Co

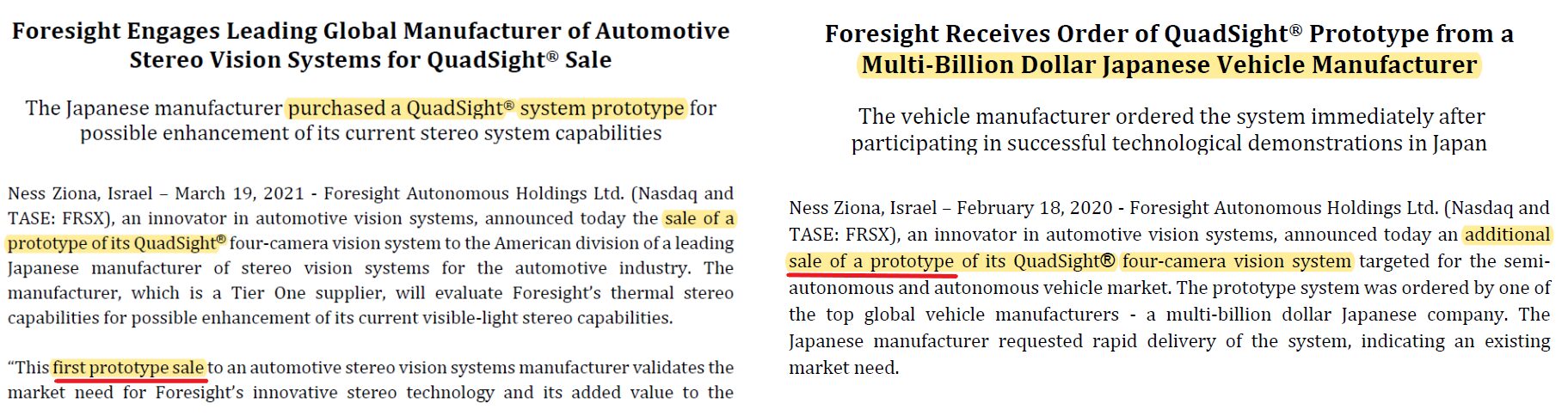

More “Sales” with “Expected Revenue” = No Revenue! – March 2019 Israeli Defense Co Will FSRX’s recent announcement of a March 2021 Japanese “Sale” be any different than last year’s Japanese Order/Sale from Feb 2020 which booked…No Revenue? We doubt it.

Will FSRX’s recent announcement of a March 2021 Japanese “Sale” be any different than last year’s Japanese Order/Sale from Feb 2020 which booked…No Revenue? We doubt it.

According to press releases Quad-Sight has been “sold” or tested by OEMs & auto distributors across the globe. It seems as though every OEM in the world has done due diligence, and none have paid FRSX either $1 of revenue for product or decided to make a strategic investment into the company. If this was truly a competitive technology, or a unique offering, OEMs would have at least made a toehold investment in FRSX.

- China – 2016 & 2017 – 3 Chinese OEMs (including JAC); Chinese EV maker – 2018

- Europe – Oct 2016 – French Industry Leader then June 2018 – European vehicle manufacturer;

- Japan – June 2019; Feb 2020 – Tier one Supplier & OEM

- America – July 2019 – Supplier & OEM

- As well as South Korea and Israel

If they can’t actually sell the tech maybe they can at least win an award.

Award Winning Technology PAYING for Technology Awards

We noticed that Foresight proudly displays multiple technology awards, including some awards we had never heard of before. With no sales and no auto OEM’s willing to vouch ForeSight’s technology, they needed to create social proof to deceive retail investors into thinking their technology is cutting edge.

Through our diligence we discovered Foresight has been PAYING for technology awards via the suspect industry of “Pay to Play” technology awards.

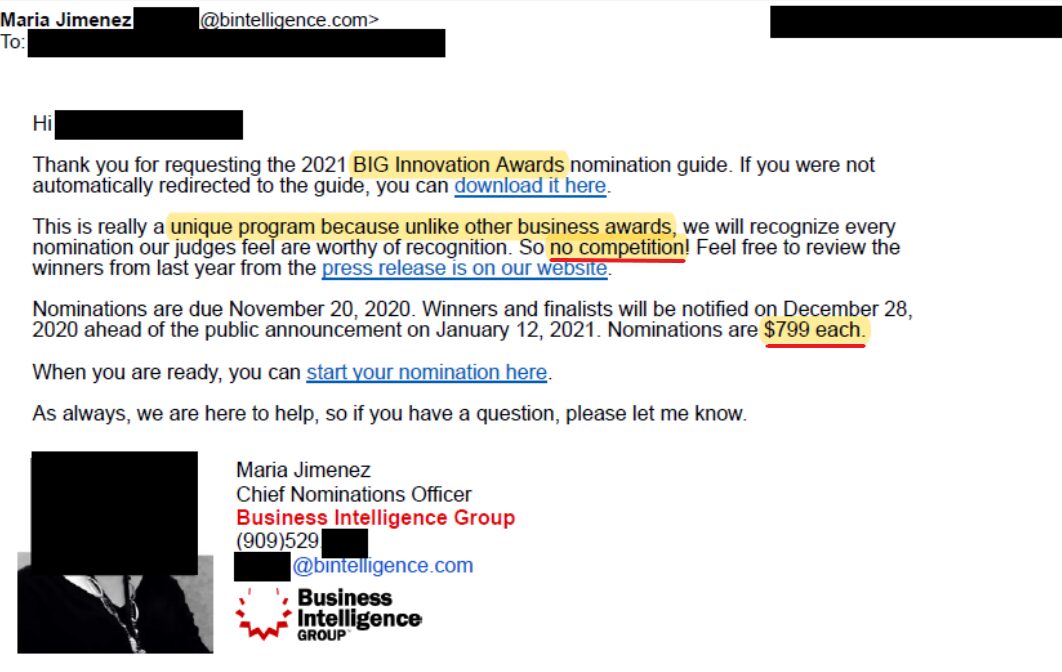

Example 1 – Buying a “Big Innovation Award” for $799

Foresight proudly display QuadSight winning a “Big Innovation Award” in press releases and investor presentations.

We reached out to Business Intelligence to learn more about the “Big Innovation Award,” they informed us it was a unique award program because it features:

- No Competition – “Unlike other business awards” there is “no competition.”

- No Scrutiny of Our Submission – Neither Business Intelligence nor the judges will “independently verify information contained in award entries” (link)

- A Majority of Nominees Win – “We provide a lot of categories, and different company sizes to provide the best chances to win to the most companies as possible”

- Nominations cost only $799

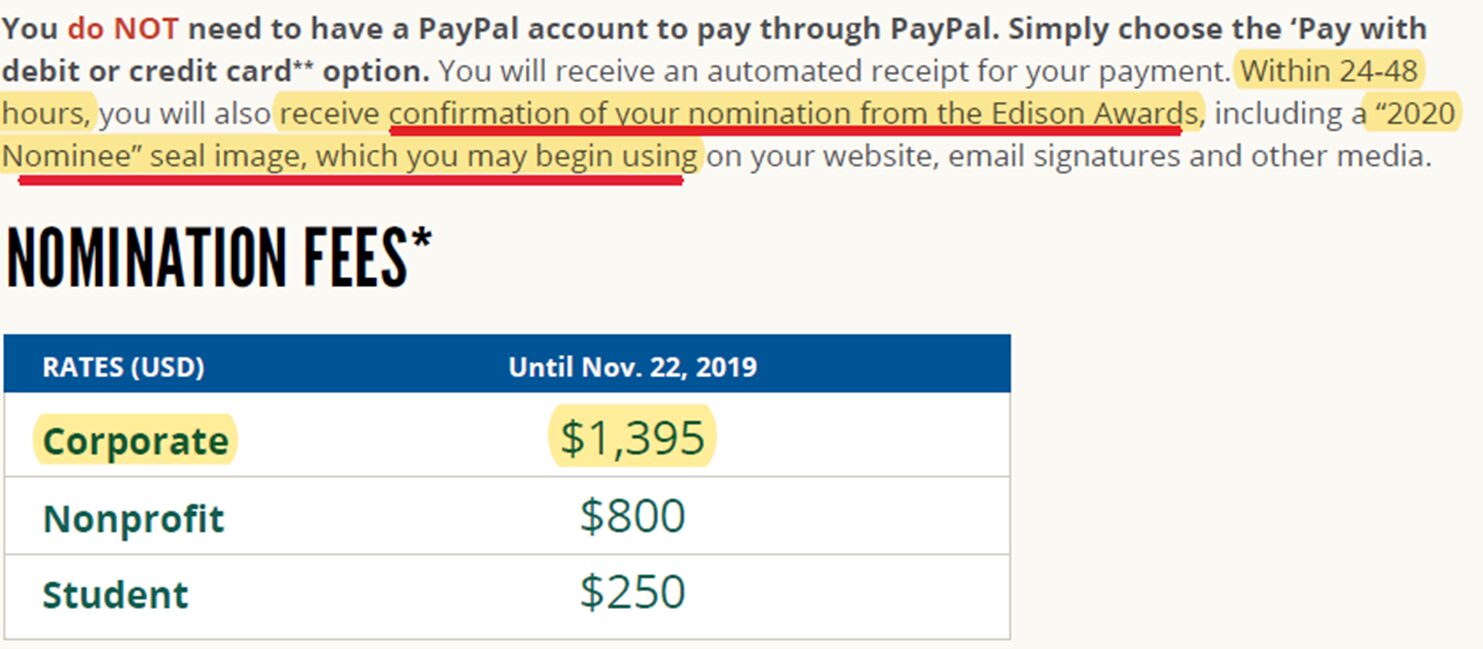

Example 2 – Purchasing an “Edison Award” for $1395

Example 2 – Purchasing an “Edison Award” for $1395

Foresight also brags about winning “Gold at the 2019 Edison Awards” – April 2019

According to the Edison Committee’s own nomination guide Edison is willing to create an entirely new category to improve a nominee’s chance of winning. FSRX’s own very narrowly defined category featured only one other competitor which also purchased “won” an award and just went public via a SPAC – 2019 Award List.

The cost of the Edison Award is $1,395 and companies also immediately receive an “Edison Award Nominee” seal image within 24-48 hours of payment so they can being using it in their media.

More Participation Awards:

In November 2018 for $850 FRSX received the CES “Honoree” Award aka a “Participation Award.” The Verge previously notes it’s given that there were 27 other Honorees in the same Vehicle Intelligence category and 1 real “Best of Innovation Award.” CES judges don’t test the product and rely on photos and descriptions the company submits. products are submitted.

Quadsight Vision – Old Tech That Hasn’t Advanced Far:

Why does a company resort to Fake Awards and Misleading Press Releases? Because their technology is inferior when compared to competitors. It isn’t surprising that FRSX has failed to demonstrate meaningful progress with its tech, despite spending a significant amount of R&D money. Management is highly incentivized to spend cash when related parties are receiving the funds, like Magna BSP is here.

Below we compare two images, one from FRSX’s YouTube channel and another from Magna BSP’s channel 7 years ago.

“QuadSight” tech from May 2020 is still remarkably similar to Magna’s system in Dec 2013.

Magna’s Dec 2013 Video

Magna’s Dec 2013 Video

Over this time, FRSX has spent ~$35m on “R&D” but we see next to no advancement in the technology to support that level of spend. Probably since a significant amount of that R&D spend has actually been related party payments to their controlled 3rd parties.

Over this time, FRSX has spent ~$35m on “R&D” but we see next to no advancement in the technology to support that level of spend. Probably since a significant amount of that R&D spend has actually been related party payments to their controlled 3rd parties.

Moreover, FRSX’s management continues to promote their technology as “mature” given the many years of development at Magna BSP. Like everything else at FRSX, this claim is overblown

In reality back in 2018, Foresight’s CEO admitted they were still running a prototype on a computer:

“In March-April in a year there will be a beta model, and in August (2018) there will be a product on the shelf. We are currently running the prototype on a computer (Foresight’s product is actually software – HM), and this process takes time.”

~Haim Siboni, CEO (2018 Article here)

Foresight’s QuadSight system also uses off the shelf hardware rather than utilizing specialized cameras or chips that are propriety innovations by Foresight. For example, FRSX’s cameras are just FLIR thermal cameras.

Competitors on the other hand have invested significantly in developing their own hardware. Tesla says that unique hardware designs, like their own silicon chips, are essential to the Tesla Autopilot Program.

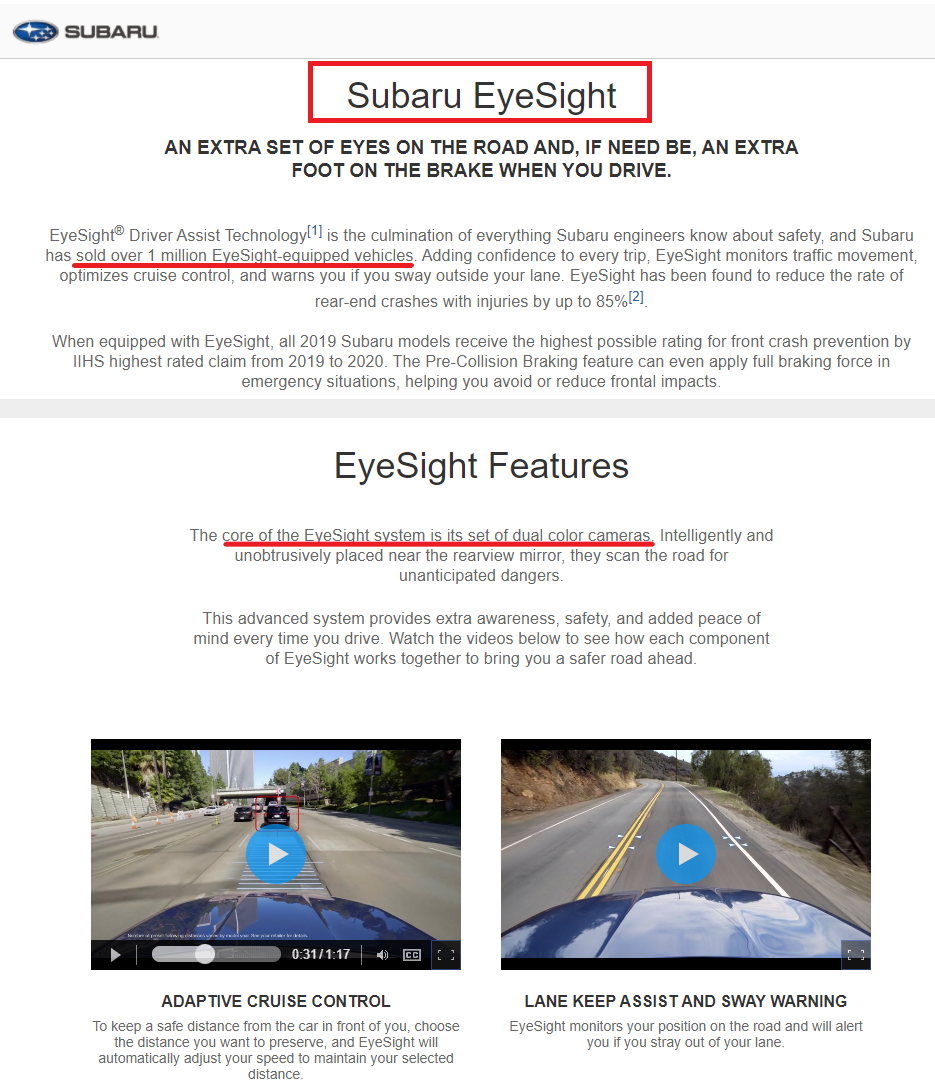

Competition is Significantly Ahead – Subaru – A Japanese OEM That Has Been Using StereoVision since 2019

ForeSight’s QuadSight technology is based on stereovision – stereovision is a system of multiple color cameras which when overlayed can perceive objects, change in depth, motion, etc and is the overlay of multiple cameras.

Recent hype at Foresight has been around a Quadsight prototype sale to a Japanese OEM (link).

Unfortunately for FSRX investors one major Japanese OEM is already using their own advanced stereovision system called EyeSight. Subaru’s EyeSight system is not a prototype product though; it’s already deployed and is on the road in over 1 million Subaru vehicles since 2019.

Other notable competition in the stereovision space that is much further along that FSRX includes:

- Tesla currently uses stereo vision but only as a part of their autopilot solution.

- Veoneer is also well ahead of FRSX. Veoneer also has $1.37bn in sales in 2021.

- Dahua technology in China is using stereovision, and had 98% accuracy in mid-2019 (Link).

The Tale of Two Failed Reverse Mergers:

The Skeleton Traders (Silberman & Shrem) already attempted, and failed, to complete a reverse merger for Foresight’s other two divisions.

- Eye-Net tried and failed to RTO with via Tamda Ltd (TASE: TMDA) in 2018. (FRSX Press Release)

- Rail Vision failed to pull off a Nasdaq IPO back in 2017 (Article)

1) Eye-Net Mobile – An App That Needs to Be More Successful than TikTok & Waze to Work. Even Then It Often Fails.

It’s no wonder Eye-Net was a “business” that Silberman-Shrem failed to reverse merge into the public markets. In order for Eye-Net Mobile to succeed their mobile app which is NOT AVAILABLE on Apple App Store or Google Play needs to be:

- More ubiquitous an app than TikTok & Facebook combined

- Convince users to keep it always on like Waze.

Eye-Net Mobile’s patent shows that it only works in the following scenario:

- Eye-Net Mobile must be downloaded on 100% of mobile phones and 100% of infotainment systems.

- 100% of the population in the area must have it always on.

- All the mobile phones somehow do not run out of battery from constant GPS usage (it sends/receives GPS locations 10 times per second).

- Eye-Net’s servers & network capacity must note be overrun by extreme amount of GPS data.

The likelihood of having all four of the above that are required for Eye-Net Mobile to work is slim to none. Yet Eye-Net Mobile actually tested this we’ve “acquired the world” and are “always on” in a 2 way collision scenario. FRSX’s own results are an uninspiring 4.5% FAILURE RATE!

100% global mobile adoption + 100% usage + 0 Battery or Server Failures = 4.5% Failure Rate

Data & Server issues – Waze App, which is likely the most successful and largest adopted GPS app delays updating other Wazers information by 2-5 min (Waze.com FAQs). Waze cite server capacity and network data capacity as the largest issue if they updated every Wazer’s location every 2 seconds. Eye-Net requires updating locations 20x more often.

Eye Net’s is currently only available on the Wunder Mobility Marketplace. Wunder Mobility is a start-up primarily focused on Vehicle Sharing & Ride Hailing.

2) Rail Vision’s Impending Crash – Knorr-Bremse Can’t See the Horse Standing on the Tracks

Foresight currently has a minority stake (19.34% or 16.5% diluted) in Rail Vision. This stake is worth ~$9.6m based on Knorr-Bremse valuing Rail Vision at $50m (PR). We believe that Knorr is unaware that they are actually investing in a business that is still controlled by Silberman-Shrem loyalists.

Rail Vision’s Board of Directors currently include 4 out of 7 members as being loyal to the Skeleton Traders:

- Sam Donnerstein – Exec Chairman – is also a director on Scoutcam’s (OTC: SCTM) board. Scoutcam is controlled by Silberman with his brother as CEO and father on the Board.

- Eli Yoresh – Director – CFO of FRSX from pre-merger; board member at many other Silberman-Shrem companies.

- Elen Katz – Rail Vision Founder who brought Shrem-Zilberman Group into Rail Vision

- Itschak Shrem (himself) – Director

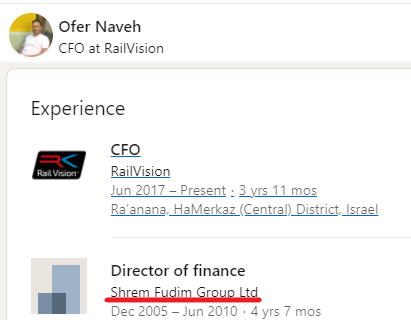

Also, Rail Vision’s CFO was previously the “Director of Finance” at a Itschak Shrem investment company (Shrem Fudim Group Ltd) according to his LinkedIn.

We reviewed RailVision’s videos of their technology which is supposed to capture all obstacles on the tracks at both night & day and we found multiple incidents of the technology failing, most notably it did not identify some fairly obvious issues like twice it missed an actual HORSE ON THE TRACKS! (Rail Vision Technology Demonstration Video – 00:19)

We reviewed RailVision’s videos of their technology which is supposed to capture all obstacles on the tracks at both night & day and we found multiple incidents of the technology failing, most notably it did not identify some fairly obvious issues like twice it missed an actual HORSE ON THE TRACKS! (Rail Vision Technology Demonstration Video – 00:19)

In this same video demonstration, the technology fails to identify a 2nd horse at night (01:28).

Other Financiers – SEC Violators, More Arrested Criminals & Behind the Scenes Suspect Players

SEC Accused Foresight’s Financiers with Stock Manipulation:

- Ionic Ventures, was recently a major FRSX’s shareholder (9.98% owner) but they are hardly shareholders you’d want to be in bed with. Both of Ionic Venture’s founders, Brendan O’Neil, and Keith Coulston were partners at Ironbridge Global when the SEC accused Ironridge Global’s of violating securities laws & manipulating microcap prices. Ironridge consented to the SEC’s order without admitting guilt and paid $4.4 million in disgorged profits.

- In December 2020 FRSX’s stock went up ~500% for no fundamental reason amongst lots of stock promoter activity. Ionic Ventures sold 100% of their shares.

Other Arrested Foresight Financiers – The Dayan Family

- Dayan Family are highlighted by FSRX as notable shareholders in past fundraising deals led by the “Shrem Zilberman Group.” Amir & Yitzhak Dayan were recently arrested in December 2020 on suspicion of tax evasion and concealing assets & income. (article)

Shrem’s Previous Partner – Criminal Convicted of Money Laundering & Bribery

- Itschak Shrem previous investment company was Shrem Podim Kellner. His partner, Avigdor Kellner, was convicted of money laundering and bribery in the infamous Holyland Case. (article)

More Behind the Scenes Consultants – Amir Uziel and Lavi Karsney constantly show behind the scenes in Silberman-Shrem companies. We have found service agreements with these Amir & Lavi’s firms at 5 different “Skeleton Trader” controlled penny stocks.

More Behind the Scenes Consultants – Amir Uziel and Lavi Karsney constantly show behind the scenes in Silberman-Shrem companies. We have found service agreements with these Amir & Lavi’s firms at 5 different “Skeleton Trader” controlled penny stocks.

The 2018 Globes story, even notes that Silberman & Shrem are “joined by two accountants, Amir Uziel and Lavi Krasny, who specialize in the American capital market.”

Why would Foresight a company with no revenue need “services agreements” with 2 different accountants consulting firms?

What type of services are they arranging?

Stock Promotions!

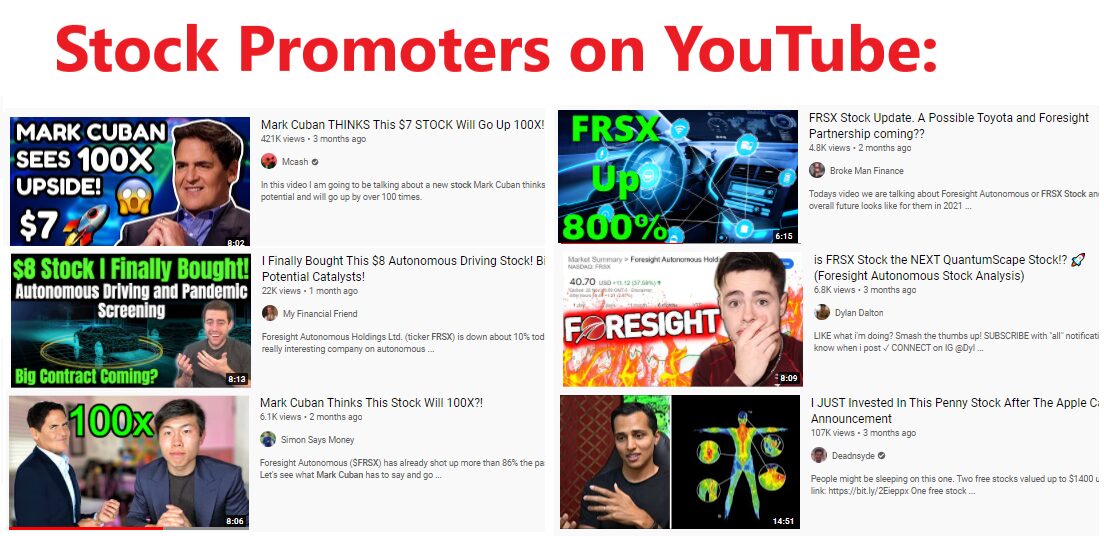

Foresight currently has a significant amount of on-going stock promotions. We were able to find and document Over 200 YouTube stock promotion videos on Foresight Autonomous. Some of these YouTube stock promoters are the very same ones that we discovered were promoting Workhorse Group. WKHS is down >50% since we published our report on Workhorse.

The stock promoters pitch FALSE narratives like:

- Mark Cuban is an Investor and thinks the stock will go up 100x (Ex 1, Ex 2)

- Foresight is partnering with Toyota!

- Foresight is teaming up with Apple or Tesla!

Foresight is no stranger to stock promotions – Sylvacap.com readily admits in their disclaimer that Foresight has been PAYING for STOCK PROMOTION

Foresight is no stranger to stock promotions – Sylvacap.com readily admits in their disclaimer that Foresight has been PAYING for STOCK PROMOTION

“Sylva has been compensated by all companies referred to in the articles, videos and podcasts we publish on our website, www.sylvacap.com. Sylva is compensated by and offers public companies digital marketing services for a term of up to one year and the compensation varies by company.”

Foresight Automotive has also been featured on Proactiveinvestors.com, another well-known stock promoter.

Negative Selling Pressure – $46m More of On-Going At The Market Offerings; Massive Shelf Registration

FRSX recently filed a $180,000,000 shelf registration with $60,000,000 currently approved for “At-the-Market” offerings.

Investors that are wondering why FRSX’s stock price is collapsing should also pay extra attention to part of their offering that was $60 million of “At the Market Offering” (ATM definition).

Foresight requested the SEC to accelerate the effective date of this offering and ever since the $60m ATM went effective the stock has collapsed. FRSX’s stock declined about -40% since the offering went effective on Feb 2nd.

As of March 21, 2021 (20-F pg 40) only $14 Million of the $60 million had been completed by AGP. That means that AGP still needs to unload $46 million of shares so a potential ~11 million shares into the market. This equates to multiple days of additional selling pressure at the current trading volume.

FRSX’s other bankers have been Chardan Capital, Aegis Capital, and is even in litigation with Roth Capital who is accusing FRSX of not paying Roth their agreed upon fees.

Conclusion – Beware The Risks of Investing In The Skeleton Traders.

Foresight Autonomous is a new notch in the infamous Skeleton Traders belt. FRSX has all the ingredients of a stock market cesspool: connections to accused market manipulators; fraudsters; stock promoters; egregious related party dealings; nepotism; obsolete technology; and fake sales.

Foresight Autonomous is unlikely to ever produce any revenue with its old undifferentiated technology and only exists to prey on unwitting retail shareholders while enriching insiders.

This stock promotion is still up >500% and will continue crashing at the hands of a dilutive at-the market offering and a massive options overhang from previously locked-up insiders.

Fuzzy Panda Research is short FRSX.

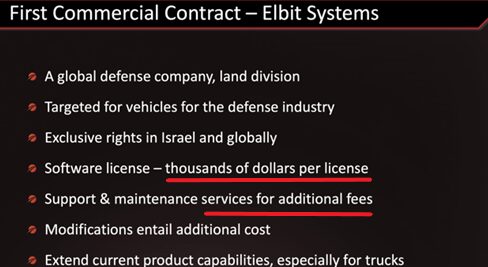

Appendix A – Where’s the Revenue this Time – The Story of the Elbit Systems Contract

In 2019, FRSX signed a sales agreement with Elbit and it was described as FRSX’s first commercial agreement. FRSX’s IR deck below highlights “thousands of dollars per license” and support & maintenance services as incremental revenue.

Like other “sales”, no revenue was actually recognized in FRSX’s financial statements.

We believe this Elbit relationship is curious because:

- Elbit is a significant investor in Brightway Vision (link here), which appears to have more advanced and competing tech with Foresight Autonomous

- If Elbit really needed the FRSX technology why wouldn’t they be a shareholder?

- Elbit also owns and develops Stereo Vision technology; do they really need FRSX’s tech?

- This article, link here, states they received hardware orders, which again came with no real revenue associated with it. This seems to contradict FRSX’s disclosure that they sold a software license to Elbit.

So how is FRSX able to use Elbit’s name publicly?

Both FRSX’s VP, Business Development, and its former Strategic Advisor, had spent many years at Elbit, per their Linkedin profiles (link here and here). We wonder if a warm contact at Elbit is allowing the use of their name for FRSX’s promotional purposes? It wouldn’t surprise us.

Appendix B – Other Empty Promotional Plans & Meaningless Partnerships:

Throughout Foresight’s history they have announced promotional new business lines that we think are nothing more than empty press releases.

- Cyber Security JV – in 2017 they PR’ed a cyber security JV with another company controlled by Silberman-Shrem (unlisted options with Shrem-Silberman and Cyber Company). Foresight has since removed this press releases from their website but we still found it (link to PR).

- Covid Play – in 2020 they even attempted to become a covid related play announcing a covid-19 symptom detection solution. (Oct 2020 Press Release, Dec 2020 Press Release)

- Other examples of worthless partnerships – Foresight announced a Brazilian distribution agreement with WebSia which is a 17 person Brazilian company founded in Dec 2003 focused on reselling technology licenses. WebSia appears to have 0 relationships to the automotive industry.

Disclaimer & Terms of Service:

By downloading from or viewing material on this website and/or by reading this report, you agree to the following Terms of Service. You agree that use of the research on this website or report is at your own risk. In no event will you hold Fuzzy Panda or any affiliated party, including officers, directors, employees and agents of Fuzzy Panda or any companies affiliated with them, liable for any direct or indirect losses caused by any your use of information on this site. You further agree to do your own research and due diligence before making any investment decision with respect to securities covered herein. You represent that you have sufficient investment sophistication to critically assess the information, analysis and opinion on this site or in this report. You further agree that you will not communicate the contents of reports and other materials on this site to any other person unless that person has agreed to be bound by these same terms of service. If you download or receive the contents of reports or other materials on this site as an agent for any other person, you are binding your principal to these same Terms of Service.

You should assume that as of the publication date of their reports and research, Fuzzy Panda and possibly any companies affiliated with them and their members, partners, employees, consultants, clients and/or investors (the “Fuzzy Panda Affiliates”) have a short position in all stocks (and/or options, swaps, and other derivatives related to the stock) and bonds of companies covered in such reports and research. They therefore stand to realize significant gains in the event that the prices of either equity or debt securities of the subject companies decline. Fuzzy Panda and the Fuzzy Panda Affiliates intend to continue transactions in the securities of issuers covered on this site for an indefinite period after their first report on a subject company, and they may be short, neutral, or long at any time hereafter regardless of initial position and the views stated in Fuzzy Panda’ research. Fuzzy Panda will not update any report or information on this website to reflect such positions or changes in such positions.

This is not an offer to sell or a solicitation of an offer to buy any security, nor shall Fuzzy Panda offer, sell or buy any security to or from any person through this site or reports on this site. Fuzzy Panda and the Fuzzy Panda Affiliates do not render investment advice to anyone unless they have an investment adviser-client relationship with that person evidenced in writing. You understand and agree that Fuzzy Panda does not have any investment advisory relationship with you or fiduciary duties to you. Giving investment advice requires knowledge of your financial situation, investment objectives, and risk tolerance, and Fuzzy Panda has no such knowledge about you.

If you are in the United Kingdom, you confirm that you are accessing research and materials as or on behalf of: (a) an investment professional falling within Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “FPO”); or (b) high net worth entity falling within Article 49 of the FPO.

Fuzzy Panda’s research and reports express their opinions, which are based upon generally available information, field and online research, and inferences and deductions through due diligence and the analytical process. To the best of their ability and belief, all information contained in their reports is accurate and reliable, and has been obtained from public sources believed to be accurate and reliable, and they have not obtained information from persons who are insiders or connected persons of the stock covered or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind, whether express or implied. Fuzzy Panda makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. Further, any report on this site contains a very large measure of analysis and opinion. All expressions of opinion and conclusions are subject to change without notice, and Fuzzy Panda does not undertake to update or supplement any reports or any of the information, analysis and opinion contained in them.

You agree that the expressions of information in this report are copyrighted and owned by Fuzzy Panda Research, and you therefore agree not to distribute this report or any excerpts from it (whether the downloaded file, copies / images / reproductions, or the link to these files) in any manner other than by providing the following link: www.fuzzypandaresearch.com. If you have obtained Fuzzy Panda’s research in any manner other than by downloading from that link, you may not read such research without going to that link and agreeing to the Terms of Service. You further agree that any dispute between you and Fuzzy Panda and their affiliates arising from or related to the material on their website shall be governed by the laws of the State of California, without regard to any conflict of law provisions. You knowingly and independently agree to submit to the personal and exclusive jurisdiction of the state and federal courts located in California and waive your right to any other jurisdiction or applicable law. The failure of Fuzzy Panda to exercise or enforce any right or provision of these Terms of Service shall not constitute a waiver of this right or provision. If any provision of these Terms of Service is found by a court of competent jurisdiction to be invalid, the parties nevertheless agree that the court should endeavor to give effect to the parties’ intentions as reflected in the provision and rule that the other provisions of these Terms of Service remain in full force and effect, in particular as to this governing law and jurisdiction provision. You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to this report or the material on this website must be filed within one (1) year after such claim or cause of action arose or be forever barred.